-768x432.jpg)

It’s been quite a week. Even before the Budget yesterday, we had a bumper week of economic data to digest. Our initial analysis of the Budget announcements was published yesterday evening. We have more analysis on the to-do list.

One area that we need a bit more clarity on is the local government spending line. There is often more to it than first appears, and differences of opinion on how the number is being presented. We’ll let you know once we have dug in to that. We will also soon put out an explainer on income tax as there are a fair few numbers floating around.

Watch out on Twitter for any updates (@strath_fai).

Labour Market

On Tuesday, labour market data for the three-month period August – October 2022 was released. Compared to the previous three-month period economic inactivity fell meaning that there has been an improvement in the proportion of people who are active in the labour market (in work or actively seeking work).

The number in employment also rose and is at its highest level since early 2019. 75.9% of working age people in Scotland are in work. This is broadly in line with the UK figures of 75.6%.

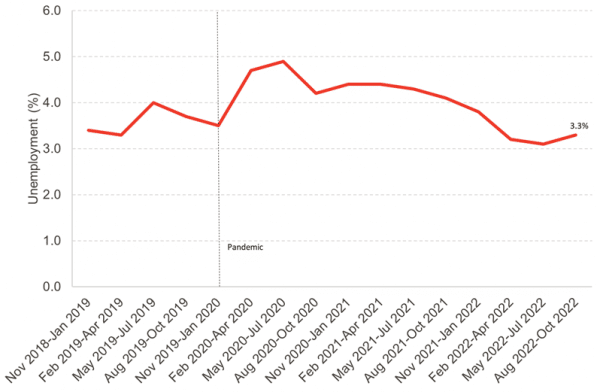

Unemployment (people actively seeking work) also rose. This is a departure from the recent trend, as shown in the chart. This isn’t necessarily all driven by people losing their jobs – the drop in economic inactivity may well be part of the reason why the unemployment rate has risen. The fact that some people may have moved from not seeking work to actively seeking work is a good thing. However, there are of course concerns over job losses. GDP fell marginally (-0.2%) in the third quarter of 2022 (June – September) in Scotland and there are fears that economic contraction will make labour market conditions more difficult.

Chart 1: Unemployment rate in Scotland

Our colleague @stuartgmcintyre was busy tweeting about all this on Tuesday and is worth a follow for timely labour market analysis.

Inflation

Wednesday saw the publication of inflation forecasts for November 2022 and showed a small fall in prices compared to recent data. Consumer prices grew by 10.7% in November compared to a year earlier. In October 2022, that figure was 11.1%. Inflation is still extremely high, but as the Bank of England Governor, Andrew Bailey, said yesterday, this reduction may be the first glimmer of light.

The ONS briefing pointed to price easing in motor fuels and second-hand cars being a key driver of lower inflation, and a partially offsetting increase in prices charged in restaurants and hotels, particularly in the price charged for alcohol. Bad news potentially for those footing the drinks bill at Christmas work outings!

The ONS also produced its latest insights on the impact of the cost of living on people’s spending. According to their data collected between 22 November and 4 December, 66% of adults in Great Britain reported they are spending less on non-essentials and 63% are also using less fuel (e.g. gas, electricity) in their homes. This of course bad news for the wider economy, and a key driver of why GDP is expected to decline again in Q4 2022, which will mean we are in a ‘technical’ recession.

Interest rate

High inflation means difficult decisions to be made on interest rates. Given most of the pressure on inflation is coming from external drivers rather than an overheating economy (if only!) the strength of the impact on inflation from interest rates rises is, in the immediate term, fairly limited.

However, the Bank of England’s remit is to target inflation in the medium term, two years ahead, and part of the rationale for the further interest rate rise is to signal that they are acting to bring inflation under control to help anchor interest rate expectations (i.e., to prevent people assuming inflation will stay high indefinitely in case the factor that into pricing and remuneration strategies, which in itself will drive up inflation).

There is a delicate balancing act between anchoring inflation expectations and trying to limit unnecessary collateral damage to the economy in the short term, principally from higher borrowing costs.

This dilemma is perhaps reflected in the fact that it was not unanimous decision of the Monetary Policy Committee to raise income taxes by 0.5 percentage points. Two members voted for no change, and one wanted the raise to be higher.

Time for a break

This will be our last weekly update before Christmas, and we won’t be back until the week commencing the 9th January. We will return, recharged, for 2024!

Our best wishes for the festive season and we hope you all manage to get a good break.

Authors

Emma Congreve is Principal Knowledge Exchange Fellow and Deputy Director at the Fraser of Allander Institute. Emma's work at the Institute is focussed on policy analysis, covering a wide range of areas of social and economic policy. Emma is an experienced economist and has previously held roles as a senior economist at the Joseph Rowntree Foundation and as an economic adviser within the Scottish Government.