Last week, we obtained the first major official economic data on the performance of the UK economy since June’s EU referendum.

The figures surprised most economists. The consensus forecast was for growth of around 0.3%, or less than half that in the 2nd quarter of 2016 (+0.7%), but the figure came in at 0.5%.

With so much speculation about the impact of Brexit in recent months, what do the figures tell us about the health of the UK economy, its likely direction in the months ahead, and the implications for Scotland?

Q3 GDP Figures

Last week’s UK GDP figures for the 3-month period Jul-Sep showed growth of 0.5% (around 2% on an annualised basis).

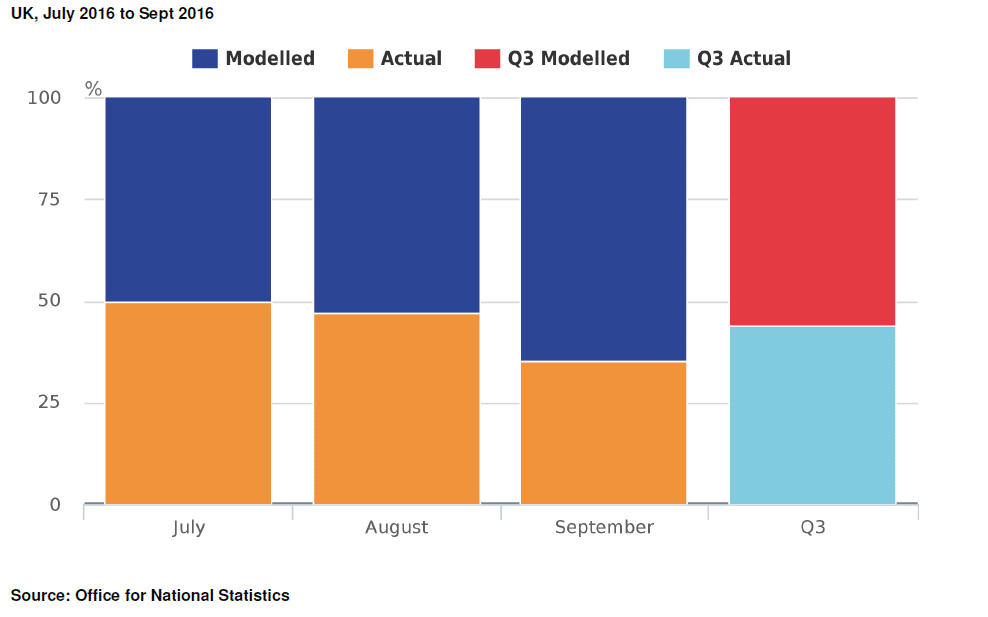

The first point to note is the usual caution around these early estimates. They are the ONS’ ‘flash estimates’ and are based upon approximately 40% actual data with the rest modelled based upon past trends and the judgement of statisticians. They are therefore more susceptible to revision in the future.

It is also clear that underneath the headline figures, some of the sector data was disappointing.

Services grew by 0.8% – driven, in part, by a spike of activity within the entertainment sector following the release of major UK films over the summer – and a healthy rise in hotel and restaurant activity, perhaps driven by a boost in tourism supported by a falling pound. However, construction fell by 1.4% with private house building stalling, whilst production fell 0.4%.

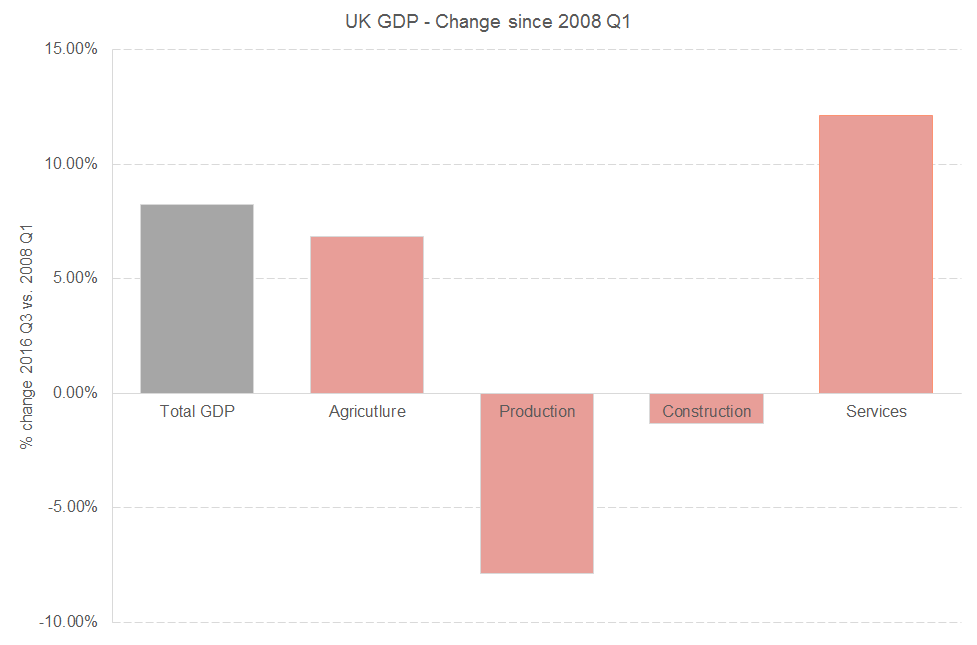

Overall, compared to its pre-financial crisis level – i.e. 2008 Q1 – the economy is around 8.2% larger with services having grown 12.1%. However, production is down some 7.9% – with manufacturing down 5.6% – and construction down 1.3% on 2008 levels.

So there remains little evidence that the UK is re-balancing, indeed the evidence suggests it has become even more unbalanced. There is also little sign that manufacturing – vital to the long-term success of the UK outside the EU – has benefited yet from the sharp fall in Sterling.

All this being said, a figure of +0.5% is a long-way away from the consensus forecast or the level of growth predicted by the majority of business surveys. On this first estimate, growth has come in at the rate predicted by the OBR back in March in their Economic & Fiscal Outlook published alongside George Osborne’s last Budget.

Indeed, even with all the caveats around 1st estimates, if you’d asked most economists – and policymakers – in July if they would take growth of 0.5% they would have jumped at the opportunity. In the immediate aftermath of the referendum, the combination of shock at the result and subsequent political vacuum at Westminster, created a real risk of a period of immediate financial and economic instability.

We hope that some of this performance is reflected in the Scottish figures for Q3 which will be published in January. Two or three issues will be worth watching for.

Firstly, the extent to which conditions in the North East and Scotland’s oil and gas supply chain have bottomed out will continue to dominate in the short-term. We know that one of the key reasons for Scotland’s diverging economic performance from the UK has been our greater exposure to the low oil price. Early signs are not too positive, with the Royal Bank of Scotland Business Monitor suggesting that conditions remain challenging in the North East.

Secondly, how well the strong performance in services in the UK is replicated in Scotland will be crucial. Scotland should benefit from a pick-up in tourism activity, but it will require much more sustained growth than we have seen recently in services more generally to match the UK’s strong performance.

Thirdly, we know that the Scottish construction sector has been returning – i.e. falling – to more normal levels of activity following unprecedented growth in 2014 and 2015. It is highly possible that this may continue for another quarter or so.

Our next Fraser Economic Commentary – now to be on a quarterly basis and published in December – will discuss these issues in greater detail.

The Outlook

So is everything fine? Did virtually every economist get it wrong? Well, in short, no.

As we highlighted in our short note in advance of tomorrow’s Economy, Jobs and Fair Work Committee roundtable, the major economic challenges with Brexit aren’t going to be the immediate economic or financial consequences of the referendum.

As Professor Brad Mackay of St Andrew’s University outlined at a Brexit Breakfast seminar last week at the Scottish Parliament – and here – most businesses when faced with economic and political uncertainty tend to adopt a ‘wait and see’ policy. Businesses may delay expansion and investment plans but immediate activities (or past investments) are more resilient.

So we should be too surprised to not see large scale immediate changes, although the prospects will increase as months pass. Most businesses will await clarity over the likely outcome of any negotiated settlement and any future change in UK industrial strategy (as demonstrated by the debate over the assurances provided to Nissan).

The effects of inflation will also take time to come through. Inflation rose in September to 1%, the highest rate since November 2014. The Bank of England expect inflation to peak at around 2.4% in 2018. Over time, this will erode incomes and hit consumption. Some consumer confidence surveys are beginning to pick-up evidence of a decline in confidence as higher inflation begins to bite.

Most economists – as evident in the Chancellor’s cautious welcoming of last week’s GDP figures – predict that whatever the data tells us about the immediate aftermath of the referendum outcome, the more serious macroeconomic challenges will begin to come through in 2017 and beyond – see chart. The average of latest forecasts for 2017 – marked by an ‘x’ – remains much lower than the forecasts for both 2016 (the red and green boxes) and the estimates published pre-referendum (the blue box). For a full explanation of the chart see here.

So what next?

Irrespective of what happens in the short-term, the real challenge from Brexit is to the UK’s long-term productivity and ability to access international markets.

Over the longer term, trade opens up businesses to new opportunities for exporting and investment; labour mobility boosts labour supply helping to increase productivity and address demographic challenges in countries – such as Scotland – with an ageing population; competition helps efficiency, product specialisation and growth; and financial integration deepens and broaden capital markets.

Any impact from Brexit on these key drivers of growth will be gradual and will stem from the potential disruption of trade and investment accumulated in the run-up to and after actual Brexit.

As we move ever close to the UK’s exit from the EU therefore, it is vital that discussions begin to focus on the practicalities of what Brexit might mean for businesses, sectors and individuals. The decision to leave the EU cannot be changed. But what can be influenced is the scale of any impact, which, in turn, depends crucially upon the terms of the exit deal and what both the Scottish and UK Governments do to address the challenges that will then follow.

In our submission to the Economy Committee, we highlight a number of areas that we believe policymakers should now focus upon –

- Understanding the trade-offs from the specific terms of the negotiated exit from the EU;

- Identifying the sectors and areas of the economy – e.g. elements of international investment, the labour market etc. – most likely to be impacted by Brexit;

- The policy opportunities that may open up – both at the Scottish and UK level – from no longer being bound by EU commitments and obligations; and,

- Reassessing existing policy priorities and commitments, and crucially the delivery of the government’s Economic Strategy, in a world where Scotland is no longer part of the EU.

None of this will be easy. And even with strong policy responses and a good outcome in the negotiations, the economy will still face headwinds.

But whilst it is understandable that the debate thus far has focussed on the scale of the impact of Brexit, the political fall-out from the referendum campaign, and the potential constitutional implications both in Scotland and the UK, it is critically important that our policymakers now move quickly to find solutions and develop strategies to respond to the challenges (and new possibilities) that Brexit presents.

And here lies an opportunity, albeit one created out of difficulty rather than success. Many of the challenges that Scotland will face in a world where the economic environment will – as a result of Brexit – be more growth-inhibiting rather than growth-supporting – have been around for decades.

We know that we must improve our export performance, boost levels of innovation in our economy (both in R&D and also in work environments), re-balance the industrial structure of our economy, focus on long-term value added rather than short-term profit, provide greater opportunities for all of Scotland to benefit from growth, and build an economy that tackles poverty and poor quality work.

Brexit won’t make any of this easier, far from it. But with the right ambition and focus within policy circles there is an opportunity to use the challenge thrown down by Brexit to take a fresh look and, perhaps a more frank assessment, at how best to address these challenges (and to take advantage of new opportunities that will emerge) in the years ahead.

Authors

The Fraser of Allander Institute (FAI) is a leading economy research institute based in the Department of Economics at the University of Strathclyde, Glasgow.