Chancellor Rachel Reeves has today delivered her second Budget, which had a significantly different flavour to last year’s. If the theme of the Autumn of 2024 was large increases in spending punctuated by smaller increases in taxes, this year it’s revenue-raisers that have taken centre stage. The Chancellor’s lack of wriggle room to increase borrowing meant a much more sombre background to this Budget given the worsening economic forecasts.

While we were initially led to believe that a broad-based increase in income tax rates might be coming, the Chancellor has opted instead for a piecemeal approach – the so-called ‘smorgasbord’. Thresholds for personal taxes (including the personal allowance, which applies in Scotland) have been frozen yet again, which brings more people into higher rates of tax. But there have also been many other smaller tax rises. These include higher taxes on property, savings and dividends income; restrictions on salary sacrifice, a new tax on electric cars; a new high-value surcharge on properties in England; and higher taxes on gambling.

This is a much riskier way of raising revenue than raising income tax. Not only are these tax increases backloaded – meaning borrowing is actually higher in the short-term – but each tax affects small numbers of people. Those affected are hit much harder and have both an incentive to organise campaigns and to change their behaviour to reduce their tax bill. There is a significant chance that these measures won’t raise as much revenue as expected, as highlighted by the OBR’s uncertainty ratings; if that happens, the Chancellor might well be back in this position next year.

Rachel Reeves increased her fiscal headroom – the difference between her plans and breaking the fiscal rules – to around £22 billion. This is a step in the right direction – although not quite enough to cope with the general uncertainty of economic forecasts recognised by the OBR. But this increase has also been achieved on the back of what are almost guaranteed to be fiscal fictions: increasing fuel duty again after 14 straight years of freezes, cutting day-to-day spending in a few years’ time and finding unspecified efficiencies. The UK Government will also assume the full risk of the special educational needs and disabilities system in England from local authorities, without setting aside any specific funding for it. This flatters the picture in terms of borrowing – a more realistic headroom might be as low as £15 billion, which is still a very thin margin.

If those spending cuts did come to pass, there would be a cut to the forecast block grant for the Scottish Government relative to previous plans in the years beyond the Spending Review period – making the projected £2.5 billion resource funding gap by the end of the decade larger still. However, in the short-run, the abolition of the two-child limit will mean the Scottish Government will no longer need to spend the £155 million it had set aside for mitigation, and will be free to allocate it to other priorities.

In terms of Barnett consequentials, the Treasury is reporting relatively small additions to funding: £0.5 billion in resource funding over four years and £0.3 billion over five years on capital. The profile, however is quite lumpy: there is a boost in the short-term, eroding away quickly and a small cut in day-to-day spending in 2028-29. This, of course, reflects overall UK Government decisions on areas which have devolved powers rather than being a specific decision about funding in Scotland, as it’s simply the operation of a mechanical formula.

Table: Barnett consequentials to the Scottish Government from the Budget

| Consequentials (£m) | 25-26 | 26-27 | 27-28 | 28-29 | 29-30 | Total |

| Resource Block Grant | 45 | 307 | 185 | -26 | Outside SR period | 510 |

| Capital Block Grant (including FTs) | 0 | 23 | 200 | 4 | 83 | 309 |

Source: HM Treasury

There is another measure which will affect Scottish Income Tax, which relates to a new category of property income which will be taxed at a different rate by the UK Government (it is currently taxed the same rate as earnings from work). Income from property is part of Scottish Income Tax; details are in short supply as to what it will mean going forward, but it might affect the block grant adjustment and leave Scottish Government with a choice to make as to whether they follow suit with a higher rate for property income.

The Chancellor also announced that the OBR would now only formally assess compliance with the fiscal rules at the Budget, rather than at every forecast. This is in line with the IMF proposal, but it’s a move that – as we discussed recently – is unlikely to have any practical consequences. The OBR will still publish the relevant figures, and the headroom will be very easy to calculate by everyone. This will do nothing to change fiscal volatility – only a move towards one forecast a year would.

Abolition of the two-child limit

The only measure in the Budget that is directed at reducing child poverty – although it’s a big one – is to remove the two-child limit to Universal Credit. The limit will be removed in full from April 2026, following speculation that the Chancellor may delay its removal or adopt a half-measure. It is still not clear when the UK Government’s full child poverty strategy will be published.

We estimate that the abolition of the two-child limit will reduce child poverty in Scotland by around 1 percentage point in 2026-27, representing around 10,000 children, although the Scottish Government had been planning to mitigate the limit. Based on April 2025 statistics, the Treasury estimates that 95,000 children in Scotland live in households that will benefit from its removal, although the number is closer to 98,000 if we include those who are subject to the Benefit Cap, a different policy which is mitigated in Scotland. The numbers affected by the two-child limit would have increased each year until the policy had been fully rolled out.

Based on forecasts from the Scottish Fiscal Commission, the abolition of the two-child limit will free up £155m that the Scottish Government was planning to spend on two-child limit mitigation in 2026-27, rising to £204m by 2030-31 (although these numbers do not take into account economic and policy changes since June). Universal Credit applies across Great Britain, including Scotland, so removing the two-child limit does not affect the Scottish Budget through the Fiscal Framework.

However, removing the limit does generate some knock-on costs for Scottish Government as it means more households are entitled to Universal Credit (and therefore for some Scottish benefits like the Scottish Child Payment) and moves more existing Universal Credit claimants onto the Benefit Cap (which is mitigated in Scotland through Discretionary Housing Payments). We estimate that these costs will reduce the net savings to around £121m.

Productivity growth and how the OBR looks relative to other forecasters

The OBR have revised down the trend rate of productivity in the medium term from 1.3% to 1%. This is a downgrade of the UK economy’s capacity to grow in each year until 2030.

Productivity has been downgraded to account for UK’s poorer long run productivity performance in comparison to other major advanced economies. This has been observed since the financial crisis and also accounts for more recent shocks from the pandemic and energy shocks. The anticipated bounce back of productivity growth from these recent shocks has not materialised in official labour and output data. The lower productivity growth rate also reflects more recent events, including changes to global trade and tariffs reducing productivity, and developments in AI which are expected to boost productivity. Planning reforms announced in March 2025 are expected to boost productivity slightly.

The productivity downgrade has a direct effect on GDP forecasts. Real GDP is forecast to grow 0.3 percentage points slower, with growth of 1.5% on average between 2026 and 2030. However, real wage growth and inflation over the next two years are forecast to be around 0.75pp and 0.5 pp higher, so overall growth in nominal GDP to 2030 is only 1pp lower than previously forecast. In isolation, the downgrade in productivity growth is also expected to decrease tax revenue by £16bn.

The OBR’s real GDP forecasts for the UK are still higher the average of external forecasts form 2026 onwards but below those of the Bank of England from 2027 onwards.

SFC estimates for Scotland from May 2025, and previous OBR forecast form March 2025 have been included for reference. If the SFC continues to align to just below OBR forecasts, we could expect lower productivity rates, and lower real GDP levels in the SFC next forecasts.

Real GDP Forecast comparisons

| 2025 | 2026 | 2027 | 2028 | 2029 | |

| OBR | 1.5 | 1.4 | 1.5 | 1.5 | 1.5 |

| Bank of England | 1.5 | 1.2 | 1.6 | 1.8 | |

| External forecaster average | 1.5 | 1.2 | 1.4 | 1.4 | 1.4 |

| SFC (May 2025) | 1.2 | 1.8 | 1.7 | 1.6 | 1.6 |

| OBR (March 2025) | 1.0 | 1.9 | 1.8 | 1.7 | 1.8 |

Source: OBR, SFC

No changes to the ‘windfall tax’

The Energy Profits Levy will remain in place until 2030, despite strong pressure from the oil and gas industry to end it sooner. This comes at a time when tax revenues from the sector are already falling, mostly due to prices being significantly lower than at the 2022 peak.

There is a possibility it could end earlier, but only if oil and gas prices drop below specific levels for two quarters in a row. While oil prices are expected to fall far enough, gas prices are not, making an early end to the tax unlikely. It will be replaced by a new, permanent system called the Oil and Gas Profits Mechanism when the EPL runs out.

This new measure will only come into effect when prices are very high. It will automatically switch on if oil rises above $90 a barrel or gas above 90p per therm, with a tax rate of 35%. The gas price threshold is particularly steep, meaning the mechanism is unlikely to be triggered except during extremely volatile market conditions.

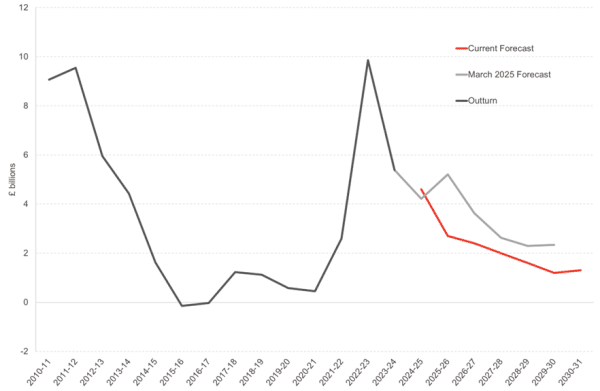

The OBR also reported that the overall tax revenue from North Sea oil and gas is expected to be lower than previously forecast, mainly due to company mergers and falling prices.

It now expects to raise £2.7bn from the sector during 2025-26, a 41% drop compared with this year and £2.5bn lower than it expected in March. By 2030-31, revenues are expected to fall further to £0.3 billion as production continues to decline and the windfall tax comes to an end, as shown in the chart below.

Chart: Oil and Gas Revenues, Outturn & Forecast, 2010-11 – 2030-31

Source: OBR

A ‘mansion’ tax introduced in England

The chancellor has announced a ‘High Value Council Tax Surcharge’ (HVCTS) on all properties in England worth over £2 million. The tax will be applied as a recurring annual charge, levied on property owners in addition to council taxes. This is forecast to raise £0.4 billion every year from 2028-29, when it is to be introduced.

Properties will be liable based on valuations in 2026 prices and placed in one for four tax bands. Liabilities will increase from £2,500 for a property valued between £2m – £2.5m, to £7,500 for a property valued at £5m or more. Liabilities are to be uprated annually in line with inflation.

The OBR assume that over time this tax will be fully passed through into house prices of liable properties and will also result in price bunching just below each band boundary. This will reduce tax revenue raised, as there will be fewer properties in scope and more properties moving into lower bands.

The HVCTS sounds like council tax, but while it will be collected through that mechanism, it will actually be a separate tax. Council tax revenues are retained locally, but the HVCTS will flow to central government.

The UK Government plans to introduce and appeal and deferral scheme for those unable to pay the tax immediately and has announced a consultation to determine the design of these systems. This leaves open the possibility that the tax will raise less than initially anticipated, and it might also come with a lumpier cash profile. But one thing that is unclear is whether these valuations will have any impact on council tax, and how the government might justify valuing part of the council tax roll but not the rest. One to watch out for in coming months.

Soft Drinks Levy expanded

As was announced on Tuesday, people with a sweet tooth may soon pay more for bottled milkshakes and some fizzy drinks, as the government confirmed a tougher sugar tax.

The levy, which aims to help tackle obesity, currently applies to drinks containing 5g of sugar per 100ml. Following a public consultation, this threshold will be lowered to 4.5g per 100ml, bringing more products into the scope of the tax. The current exemption for milk-based drinks will also be removed.

However, this doesn’t automatically mean higher prices for milkshakes or milky coffees. Manufacturers could decide to absorb the extra cost or reduce the sugar content, something many already did when the tax first came in.

The consultation estimated that the expanded Soft Drinks Industry Levy (SDIL), due to take effect from 1 January 2028, would raise £40–45 million a year in extra revenue. The OBR estimates expect the figure to be slightly higher, around £50 million a year by the end of the forecast period.

This isn’t a major boost to overall tax revenues. If the purpose of the tax is to encourage people to consume less sugar, the amount of money it generates shouldn’t really the main measure of success – but there is a real trade-off in terms of adding to fiscal consolidation and changing behaviour.

Does the announcement apply in Scotland?

One of the questions we always try to answer is whether the announcements that the Chancellor makes applies to Scotland. The table below tries to answer that – it’s not always clear, however, so we have flagged where we aren’t sure!

| Announcement | Will it apply in Scotland? | Notes |

| Taxes | ||

| Freezing personal tax and employer National Insurance contributions thresholds | In part | The Scottish Government has powers to set thresholds for income tax on non-savings and non-dividend income, with the exception of the Personal Allowance (the level of earnings at which an individual first becomes liable for income tax).

National Insurance is reserved so this will apply automatically in Scotland. This actually reduces tax rates relative to the counterfactual as NICs drop to 2% after the £50,270 threshold |

| Taxing salary-sacrificed pensions contributions | Yes | These changes apply to National Insurance, which is a reserved policy. |

| Increasing the tax rates on dividends and savings income | Yes | Tax on savings and dividend income is reserved, however, so these changes will apply to people in Scotland |

| Increasing the tax rates on property income | No | Scottish Income Tax includes applies to income from property so changes to tax on income from this source won’t automatically apply in Scotland. There is likely to be some impact on the Block Grant Adjustment, so the Scottish Government will need to decide whether to reflect these changes in line with UKG |

| Reducing the writing down allowance main rate in corporation tax | Yes | Corporation tax is reserved so these changes will apply in Scotland |

| A new mileage-based charge on battery electric and plug-in hybrid cars from 2028 | Yes | This is reserved policy so will apply in Scotland |

| Changes to taxation of gambling | Yes | This is reserved policy so will apply in Scotland |

| Reduced capital gains tax relief on disposals to employee ownership trusts | Yes | This is reserved policy so will apply in Scotland |

| A council tax surcharge on properties worth over £2m (mansion tax) | No | Despite the name, it is not actually council tax, but a separate tax that will flow to central government. Will only apply in England |

| Business rates changes for retail, hospitality and leisure funded through higher rates on larger properties and other changes | No | Non-domestic rates are devolved so this won’t apply in Scotland. There may be Barnett consequentials |

| Alcohol duty | Yes | This is a reserved policy so will apply in Scotland |

| Benefits | ||

| Working age benefit uprating | In part | This will apply to reserved benefits in Scotland (e.g. Universal Credit). The Scottish Government is yet to announce uprating for devolved Scottish benefits |

| Universal Credit: Removing the two-child limit | Yes | Universal Credit is reserved so this will apply in Scotland. The Scottish Government had already stated plans to mitigate the two-child limit from March 2026 and there will be some spillover costs |

| Universal Credit: Extend the £2,500 surplus earnings threshold for one year from April 2026 | Yes | Universal Credit is reserved so this will apply in Scotland |

| Motability Scheme: Reforming tax reliefs | Yes | The Motability Scheme operates UK‑wide (including Scotland), and the tax treatment is set by UK‑level tax policy |

| Other | ||

| National Living Wage and National Minimum Wage increases | Yes | This is reserved policy so will apply in Scotland |

| Youth Guarantee: Jobs Guarantee scheme funding | Probably | Employability is always a grey area, but as far as we can work out, these changes would lead to consequentials which the Scottish Government can choose how to spend it |

| International Student Levy | No | Further detail within a consultation published today indicates that this won’t automatically apply in Scotland |

| Soft Drinks Industry Levy (SDIL) | Yes | This is reserved policy so will apply in Scotland |

Authors

João is Deputy Director and Senior Knowledge Exchange Fellow at the Fraser of Allander Institute. Previously, he was a Senior Fiscal Analyst at the Office for Budget Responsibility, where he led on analysis of long-term sustainability of the UK's public finances and on the effect of economic developments and fiscal policy on the UK's medium-term outlook.

Mairi is the Director of the Fraser of Allander Institute. Previously, she was the Deputy Chief Executive of the Scottish Fiscal Commission and the Head of National Accounts at the Scottish Government and has over a decade of experience working in different areas of statistics and analysis.

Emma Congreve is Principal Knowledge Exchange Fellow and Deputy Director at the Fraser of Allander Institute. Emma's work at the Institute is focussed on policy analysis, covering a wide range of areas of social and economic policy. Emma is an experienced economist and has previously held roles as a senior economist at the Joseph Rowntree Foundation and as an economic adviser within the Scottish Government.

Ciara is a Knowledge Exchange Fellow at the Fraser of Allander Institute. Her main area of focus is macroeconomic and fiscal analysis. She has recently completed a secondment to the Scottish Fiscal Commission, where she worked as an Economic and Fiscal Analyst in the economy team forecasting macroeconomic conditions.

Spencer is a Senior Knowledge Exchange Fellow at the Fraser of Allander Institute.

Brodie is a Knowledge Exchange Associate at the Fraser of Allander Institute.

Josh is a Knowledge Exchange Assistant at the Fraser of Allander Institute, at the University of Strathclyde.