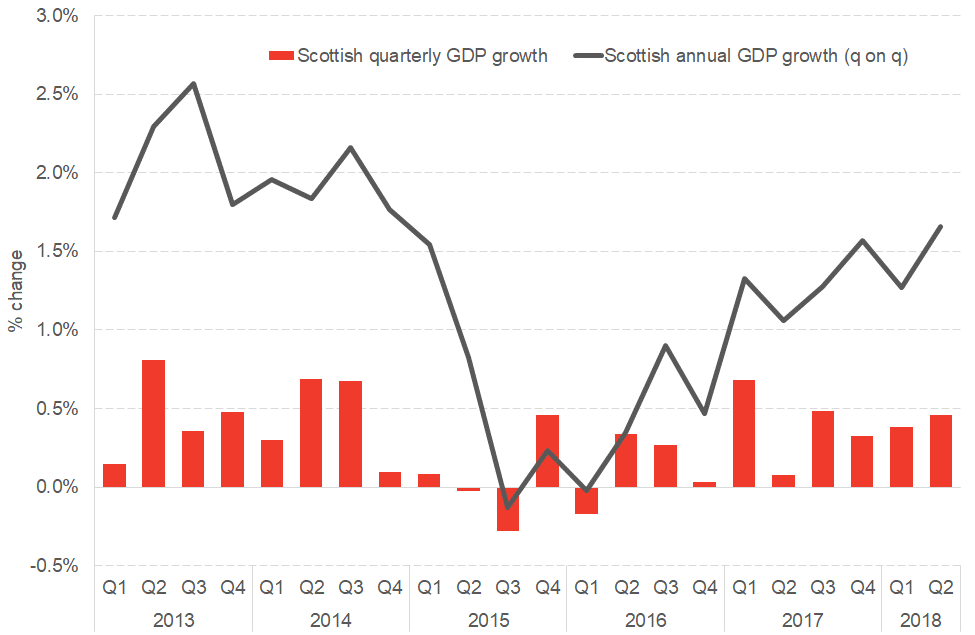

Yesterday’s Scottish GDP growth figures – for the period up to June 2018 – showed a further pick-up in economic growth in Scotland. The Scottish economy expanded by 0.5% over the 3-months to June. This followed revised growth of 0.4% in the first 3-months of the year.

In this blog we provide a quick summary of the key trends. We’ll have a more in-depth discussion in our Economic Commentary – in partnership with Deloitte – to be published on Wednesday 26th September.

Upturn in growth

This week’s figures – consistent with the latest survey indicators and our prediction from June – represent further evidence of the first sustained period of expansion since the downturn in oil and gas in early 2015.

Indeed, growth over the year to June 2018 was the fastest since late 2014/early 2015.

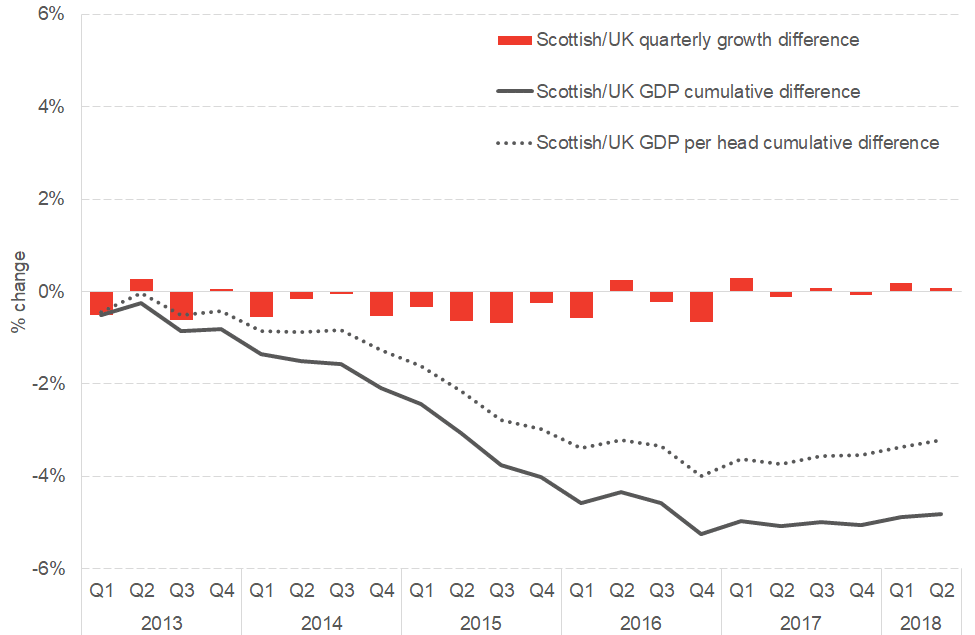

The Scottish economy has outpaced the UK for the last two quarters. And over the year, on a quarter-to-quarter basis, Scottish growth grew more quickly by around 0.4 percentage points.

Annual and quarterly economic growth in Scotland since 2013

Source: Scottish Government

As the Scottish Government were pleased to point out, the latest figures show growth in the first six months of 2018 has “been greater than the 0.7% growth forecast made by Scottish Fiscal Commission for 2018 as a whole”. The fact that they were mentioning this suggests that the SFC’s forecasts have raised eyebrows in the government – although as we pointed out here, some of the explanation for this relates to the way in which the Scottish Government had been measuring construction activity. The SFC have not yet produced a forecast on the basis of this new data – it will be interesting to see how their forecasts evolve in the next iteration.

That being said, annual growth of 1.7% (quarter-to-quarter) and 1.4% (4Q-on-4Q), still lags Scotland’s long-term historical growth rates.

And some of the upturn undoubtedly reflects a degree of cyclical catch-up; with the UK having grown more strongly over the four years to late 2016.

Scottish vs. UK growth since 2013

Source: Scottish Government

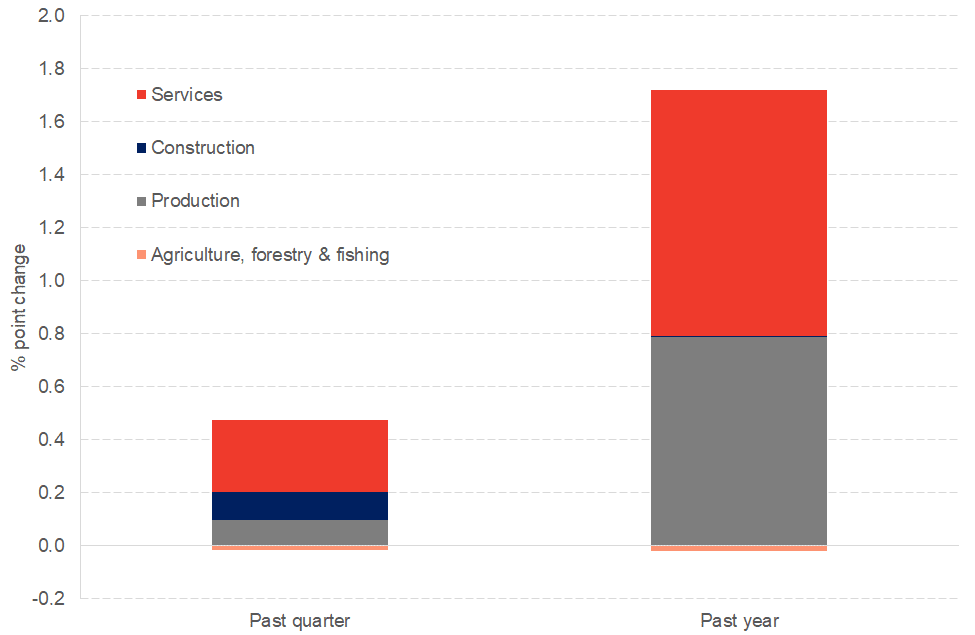

What has been driving the growth?

The upturn in the Scottish economy has been increasingly broad-based. Over Q2, there was growth of 0.6% in production activities, 1.8% in construction and 0.4% in services.

With services by far the largest element of our economy –over 75% of activity – it is no surprise that Scotland’s overall rate of growth has been shaped by growth in this sector.

Drivers of growth – contribution to growth by sector (Q2 and past year)

Source: Scottish Government

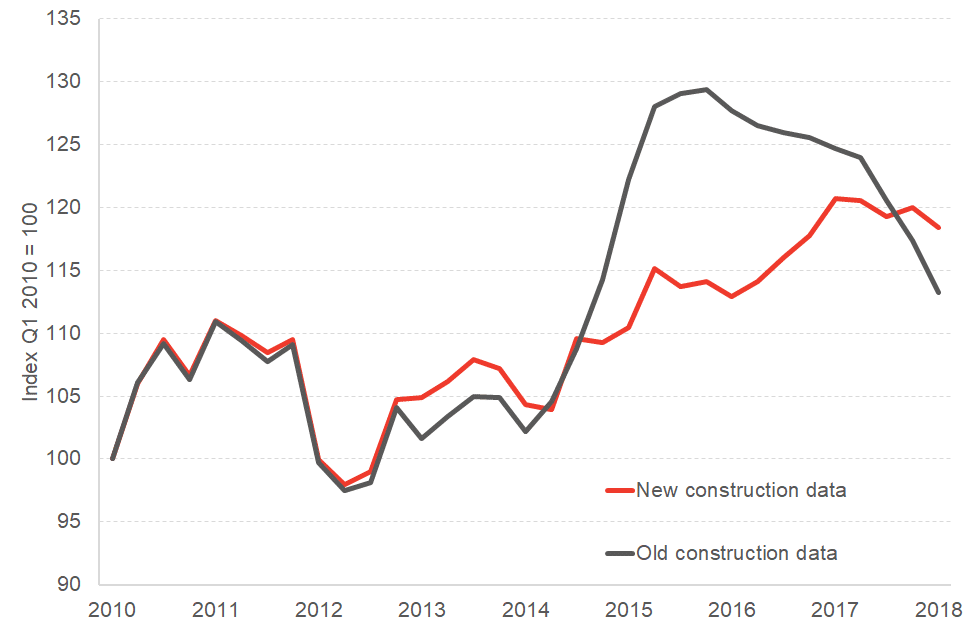

Construction grew by around 1.8% over the quarter, bouncing back a little following a challenging start – likely brought on by the bad weather – to 2018. As the chart highlights, the new time profile for construction looks very different to what was reported back in June.

Revised construction methodology – significantly boosted growth in 2016 and 2017 (but fell back in 2014 and 2015)

Source: Scottish Government

Some of the improvement in the headline Scottish numbers undoubtedly reflects a more positive outlook for oil and gas than last year as a result of increased onshore activity (remember that the data released yesterday do not include estimates of fluctuations in offshore activities themselves).

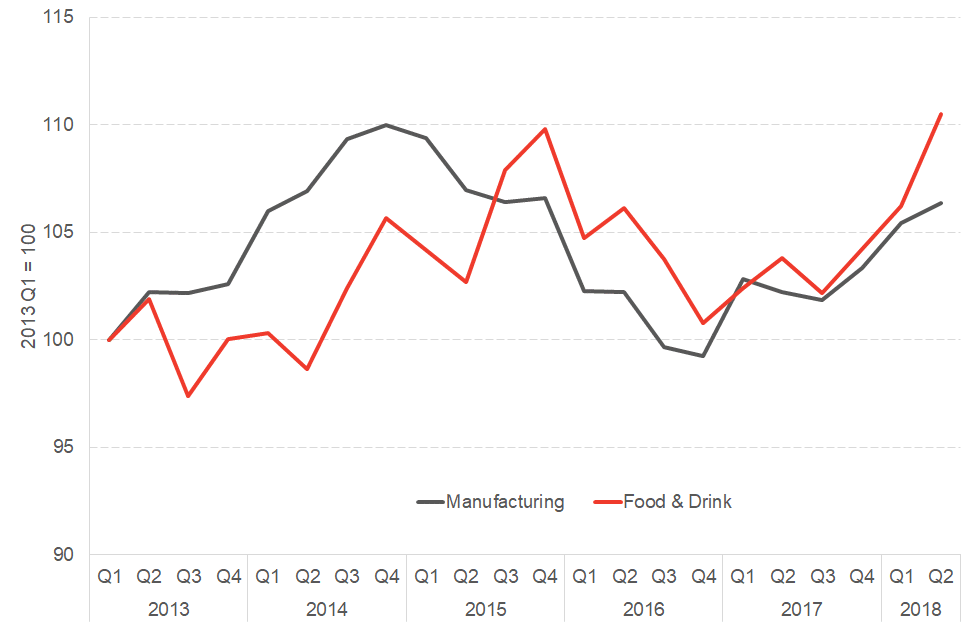

But there is also increasing evidence of a wider recovery. For example, manufacturing grew by 0.9% over the quarter and by 3.2% over the year on 4Q-on-4Q basis.

A key driver of this has been the strong growth in Scotland’s food and drink sector. The sector has grown 3.0% over the year on a 4Q-on-4Q basis to reach its highest ever level.

Manufacturing and Food & Drink latest economic performance

Source: Scottish Government

In services, retail & wholesale and the accommodation and food sector grew strongly over the year. Indeed around a quarter of the total growth in Scottish GDP this quarter has stemmed from growth in the retail and wholesale sector.

Whilst positive, it is clear from wider indicators that both sectors – and individual companies within these sectors – continue to find trading conditions challenging.

Summary

Yesterday’s GDP figures are clearly welcome and show the Scottish economy continuing to make up some lost ground following an exceptionally challenging 3 or 4 years.

That being said, growth remains below trend and wider indicators within the economy – such as household incomes and real earnings – continue to underperform.

It is interesting that whilst there is undoubtedly Brexit heightened uncertainty, many businesses appear to be ‘looking-through’ such concerns and are getting on with day-to-day activities. But this situation is clearly a fragile one. The apparent lack of contingency planning amongst many firms is a significant concern.

In next week’s commentary we’ll discuss all of this in greater detail and provide an update to our outlook for the Scottish economy for the next few years.

Authors

The Fraser of Allander Institute (FAI) is a leading economy research institute based in the Department of Economics at the University of Strathclyde, Glasgow.