Today we published our latest Economic Commentary.

Today’s Commentary includes a forward look to tomorrow’s Scottish Budget.

In this blog, we summarise some of the key points from our latest outlook.

- As we outlined in our last Commentary, growth in the Scottish economy has picked up in recent times, consistent with the view we set out this time last year.

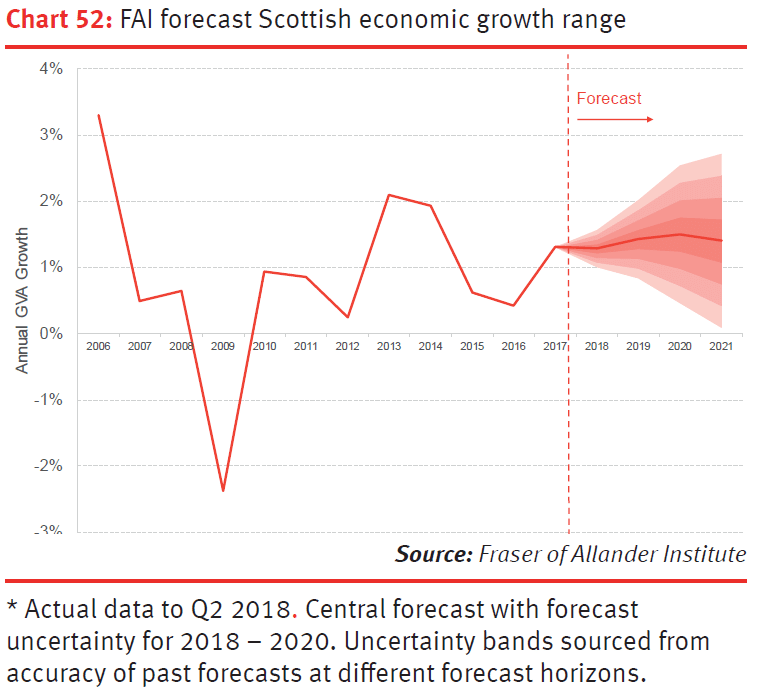

- On balance, we are cautiously optimistic that 2018 will mark a continued improvement in the Scottish economy, although growth is likely to remain below trend.

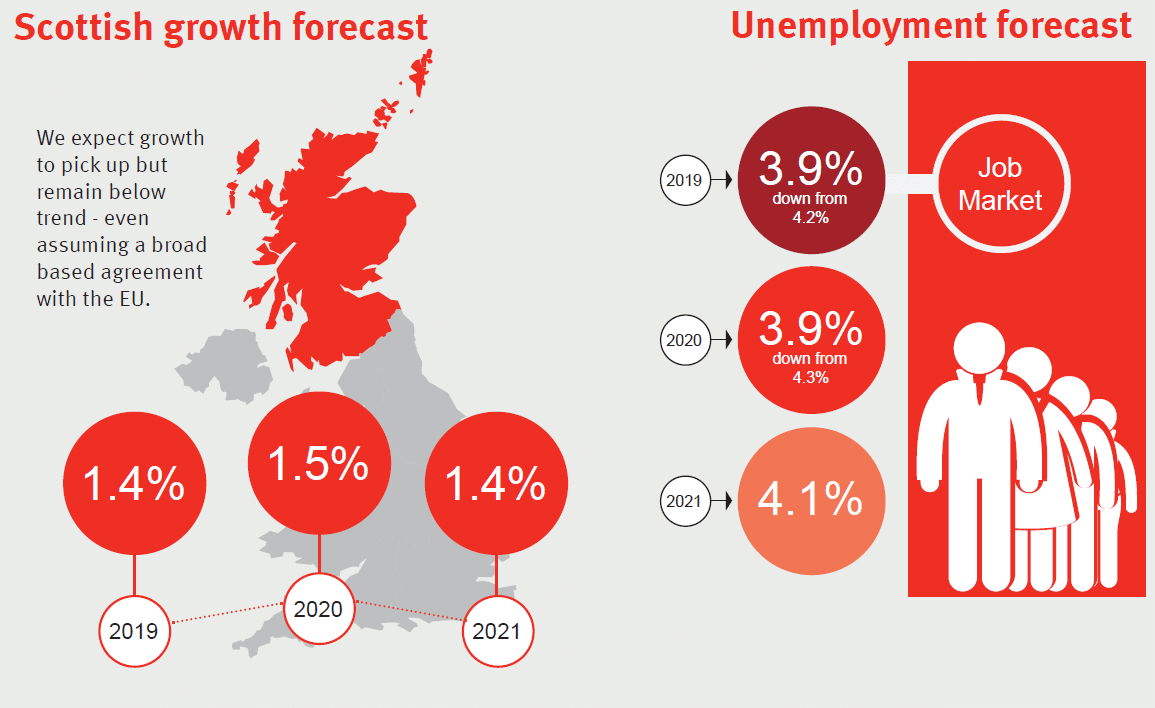

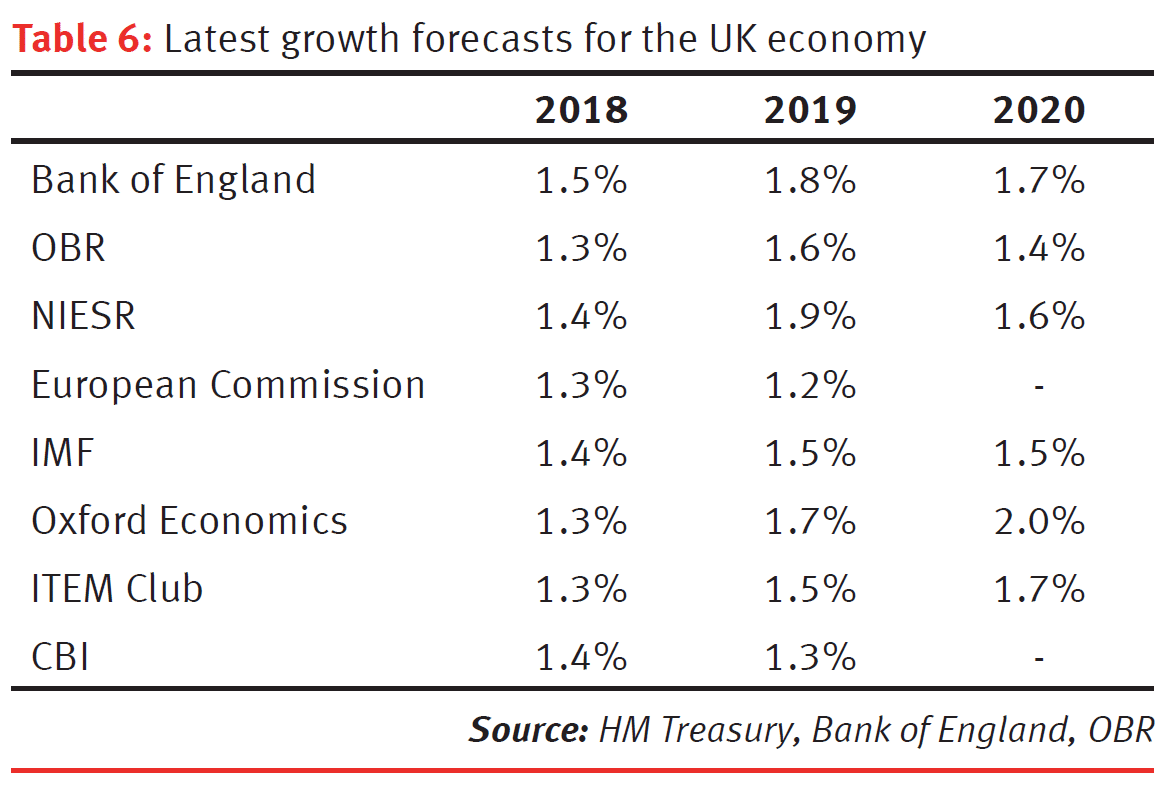

Our latest forecast is for growth of 1.4% in 2019, 1.5% in 2020 and 1.4% in 2021.

There is an important caveat with these forecasts.

They are based upon a broad-based agreement between the UK and the EU being reached before March 2019.

Should this not happen, then our forecasts are likely to change significantly. Whilst we do not share the extremely negative outlook of some, we can say with some confidence that ‘no deal’ would be a substantial (negative) economic shock.

Our latest forecast puts us slightly more optimistic than the government’s own official forecaster the Scottish Fiscal Commission, who will update their forecasts tomorrow alongside the Scottish Budget.

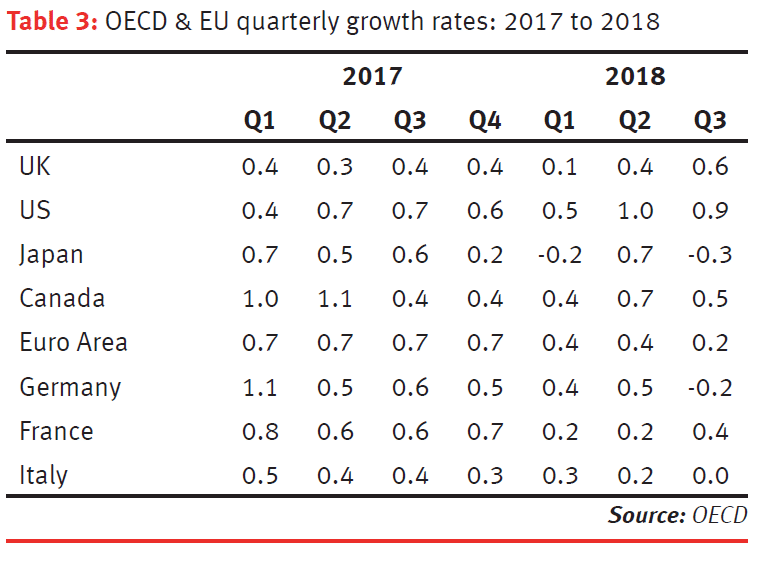

- The global economy remains relatively robust, as it has been for some time. However, there is some evidence of slowing in some of Scotland’s key trading partners in Europe.

The global economy has been in robust health for over two years now.

World GDP is estimated to have risen by 3.7 % in 2017, up from 3.2 % in 2016. The IMF forecast that it will remain at this – above trend – level in 2018.

However, as we highlighted in our last commentary, most economists believe that growth has peaked (at least in advanced economies). Indeed, there is growing evidence of a slowdown in many of Scotland’s key trading partners. Table 3. In particular, output in the Euro Area rose by just 0.2% – a four year low – over the summer.

Significantly, the German economy contracted for the first time since 2015, driven in part by ongoing challenges in car manufacturing, but also wider fragility in investment and household spending.

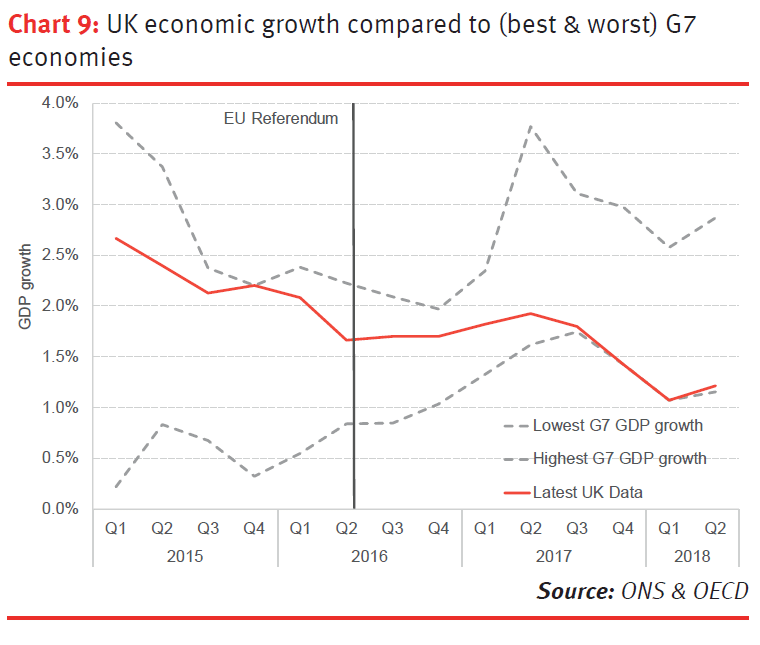

- Following a period of relatively strong growth of the period from 2014 through 2016, the UK economy has slowed significantly in the last 2 years compared to its main competitors

In late October, the OBR revised down their forecasts for GDP growth in 2018 to just 1.3%. Since then, figures have shown that growth picked-up over the summer (+0.6%), boosted in part by good weather, the World Cup and recovery in sectors which had experienced a challenging start to 2018.

This recovery was particularly pronounced in construction, where output grew by over 2%.

It is over a longer time horizon that a clearer picture of the true health of an economy can be assessed.

This shows that even with these recent positive figures, UK growth remains below trend with annual growth of 1.5%.

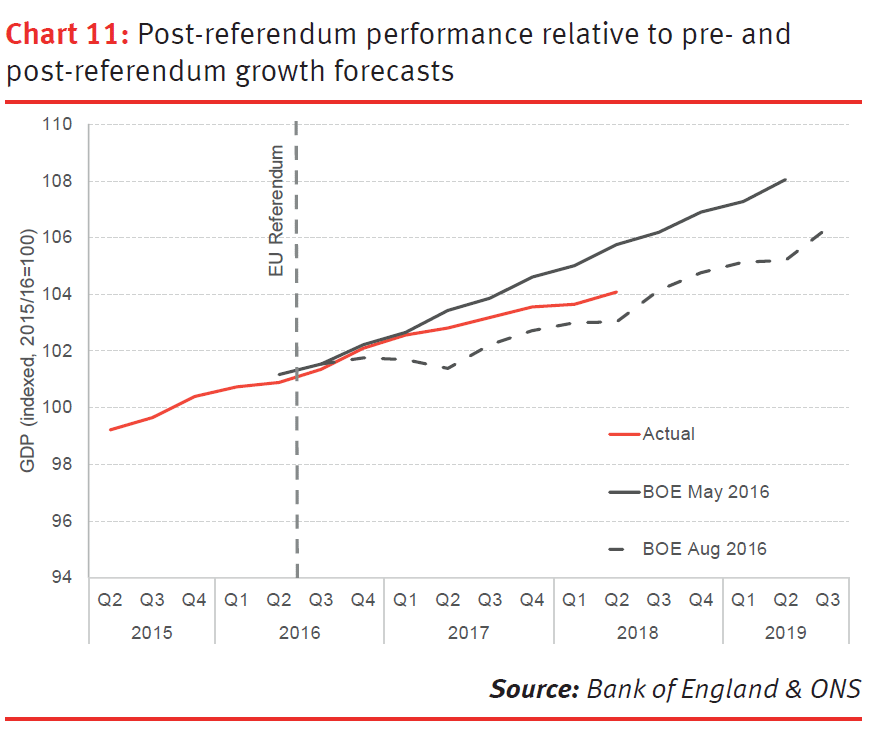

- This slowdown in growth in the UK has led to convergence towards forecasts made after the EU Referendum

It is therefore hard not to conclude that the ongoing Brexit uncertainty has had an impact. The fall in the pound has squeezed household incomes. Business investment has arguably taken the biggest hit and has contracted now for three consecutive quarters.

Of course, predicting where the economy ‘would have been’ had a referendum not been called is fraught with difficulty.

What we can at least conclude is that those who predicted a sharp recession immediately after June 2016 were wrong, but so too were those who suggested that leaving the EU would have no negative impact.

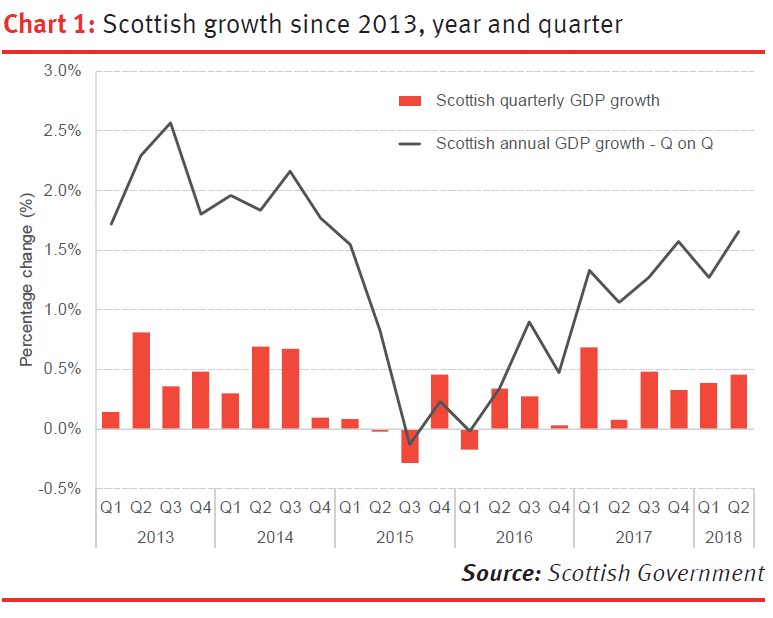

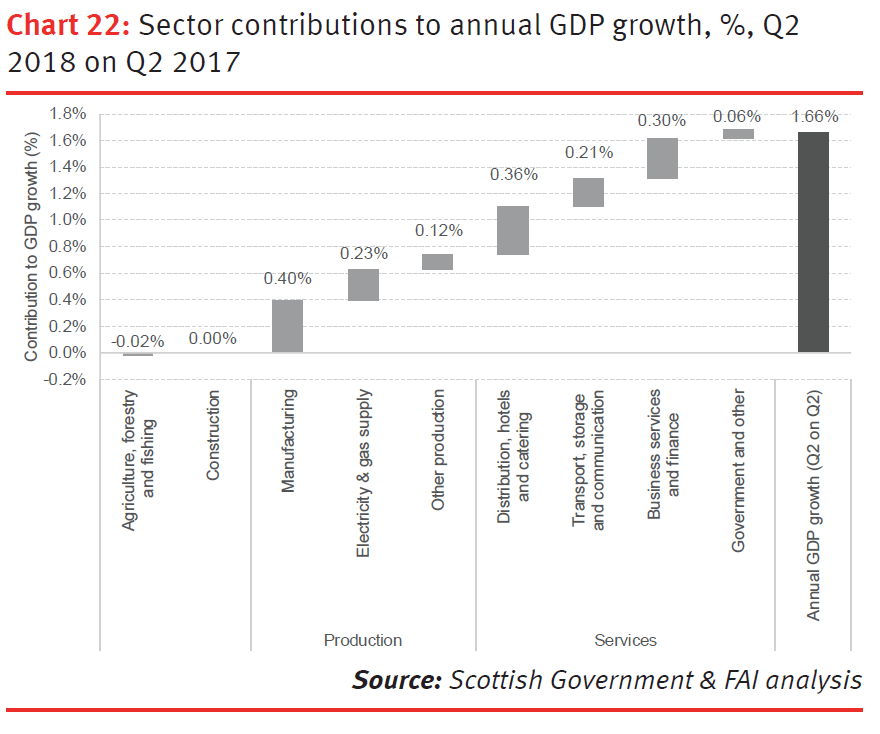

- Growth in Scotland over the last year has been relatively broad based and faster than the UK as a whole.

Over Q2, there was growth of 0.3% in production activities, 1.9% in construction and 0.5% in services.

Some of this reflects a degree of cyclical catch-up with the UK having grown much more quickly than Scotland since 2014.

It also reflects the fact that the outlook for oil and gas – and its all-important supply chain – remains more positive than it has been in almost three years.

The oil and gas sector had just come through a difficult period, with confidence returning.

Whilst the current low oil price will come as a blow to many, the mood in the sector remains confident with most contractors and operators better prepared for a lower break-even price.

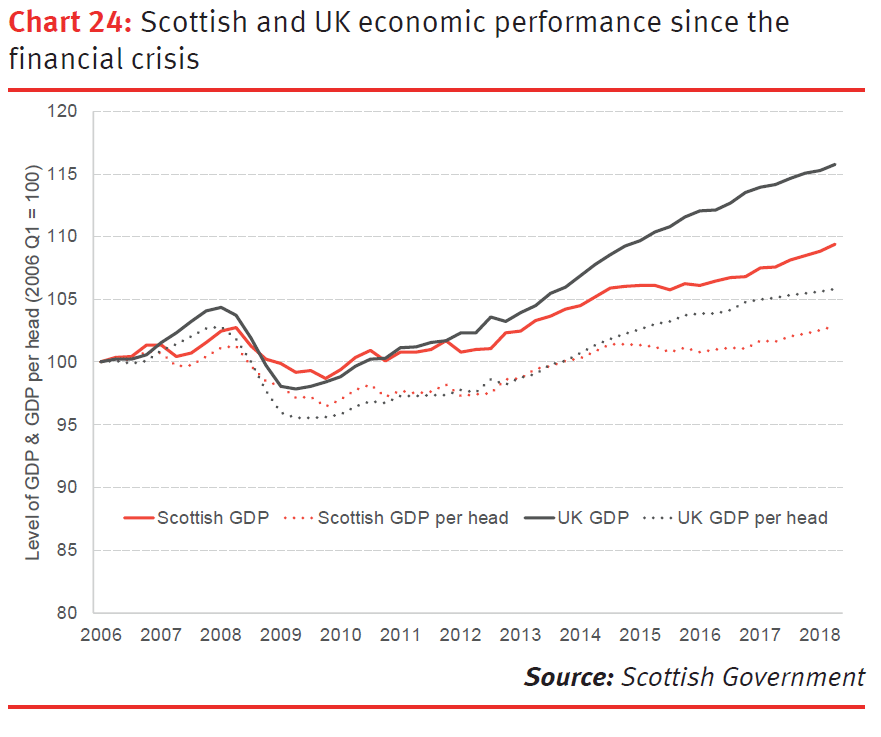

- Looking back over the last ten years since the global financial crisis, the economic story in Scotland is one of a shallower recession, but then sustained weaker recovery compared to the UK as a whole

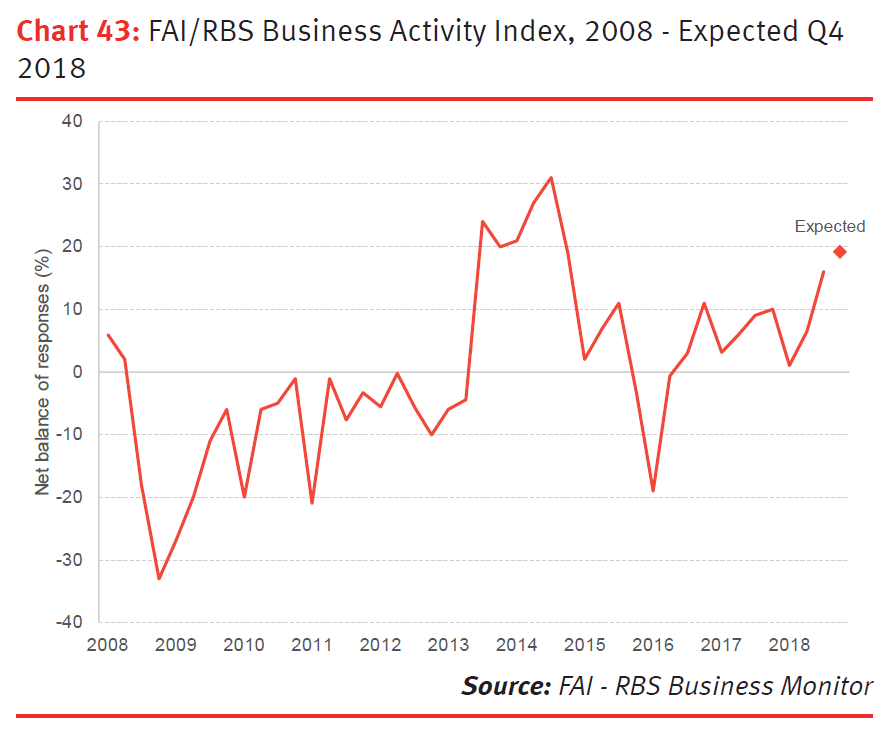

- Indicators of day-to-day activity in the Scottish economy continue to hold up relatively well.

This backs up the assessment we made in June that, despite Brexit uncertainty, underlying economic conditions have strengthened in the last 6 months. We retain that cautious optimism, albeit dependent on a broad based Brexit process.

For example, The FAI/RBS Business Activity index shows sentiment amongst businesses remains relatively strong.

Unsurprisingly, concerns remain around investment, reflecting the wider economic and political uncertainty.

One interpretation of these data is that the current period of heightened uncertainty is leading businesses to meet any increase in demand by taking on more workers, rather than investing in new plant and machinery.

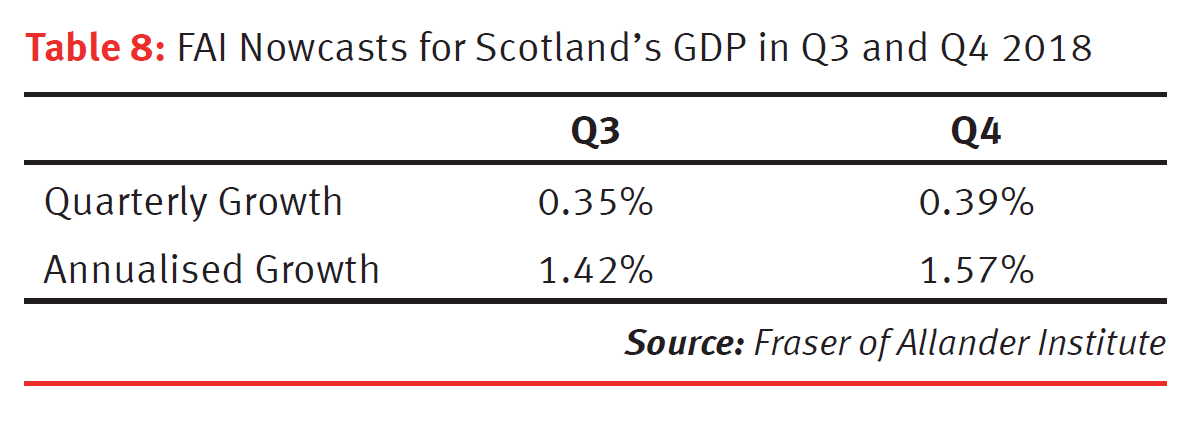

- Our latest nowcasts are consistent with the view that growth will continue at its current rate (and may even surprise on the upside), provided that a broad based agreement on Brexit can be secured.

Overall, our base forecasts are similar to our previous commentary. In short, we believe that the Scottish economy will grow this year, will quicken slightly over the forecast horizon, but growth will remain below trend.

Overall, our base forecasts are similar to our previous commentary. In short, we believe that the Scottish economy will grow this year, will quicken slightly over the forecast horizon, but growth will remain below trend.

Our latest forecasts for Scotland put us broadly in line behind the consensus forecasts for the UK.

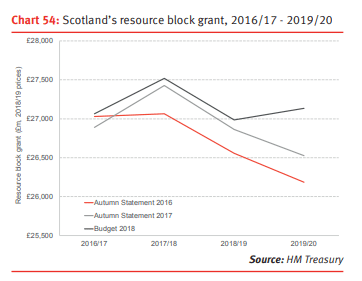

- One of the frustrating things with the Brexit debate is that it has crowded out important discussions we should be having around domestic issues. Indeed we’ve heard very little debate about tomorrow’s Scottish budget. But the decisions Mr Mackay will set out will have important implications for the relative competitiveness of our economy and the future of public spending in Scotland.

As we set out in a blog yesterday, the Cabinet Secretary has received a windfall of around £720 million additional Barnett consequentials to spend this year.

On top of this, should he choose not to follow the Chancellor’s lead and raise the higher rate threshold on income tax, then he’ll raise around a further £200m, Of course, this poses a dilemma for him in that he’ll have to defend a higher income tax burden in Scotland (for some taxpayers) compared to what exists in rUK.

In addition, it will be interesting to see how the other bands in the new Scottish 5 band system evolve, perhaps to give small tax cuts to lower earners.

Authors

The Fraser of Allander Institute (FAI) is a leading economy research institute based in the Department of Economics at the University of Strathclyde, Glasgow.