The prospects for ‘no deal’ to be agreed between the UK and the EU have increased in recent weeks.

A lot has been written about the potential long-term economic implications from Brexit. All else remaining equal, the larger the economic barriers between Scotland and its main international trading partner, the greater the potential hit to the country’s growth potential.

But very little has been written about what the implications might be in the short-run from ‘no deal’….beyond “bad” or “very bad”.

In this blog we try to unpick some of the key issues surrounding what a ‘no-deal’ might mean for the economy and just why it is so difficult to forecast.

Performance since the referendum

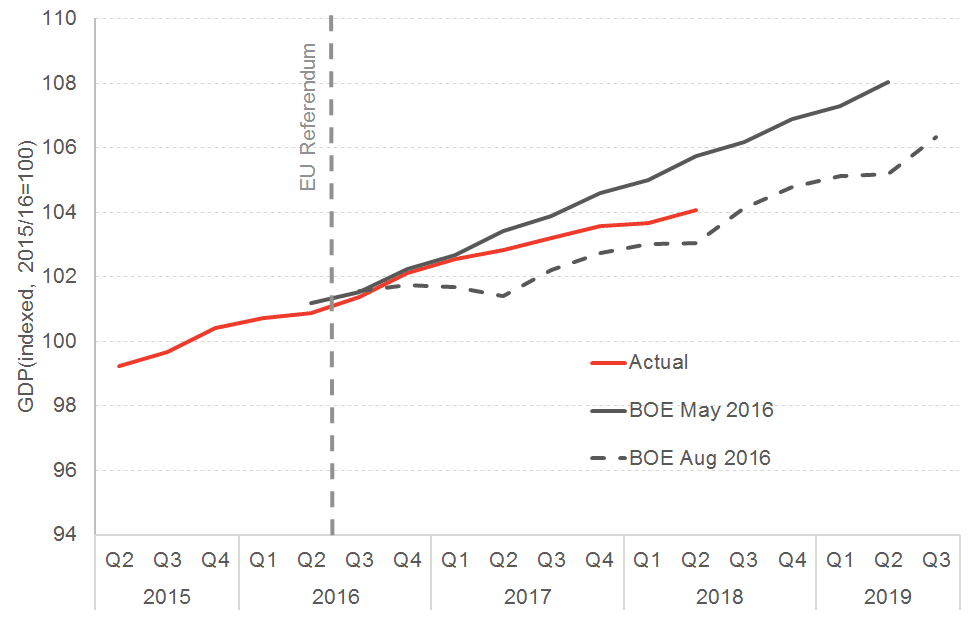

Many will recall the UK Government’s claim that the economy would fall into a recession after the ‘leave’ vote in 2016.

In the end, the economy did not enter recession. But as time has progressed, it is clear that growth has slowed – see chart.

Some have argued that UK economy is around 1 to 2 per cent smaller than it would otherwise have been because of the result of the EU referendum result has been in the region of 1 to 2 per cent. But such calculations come with wide confidence intervals.

Here in Scotland, growth through 2016 and 2017 was well below trend. But this was driven by the downturn in oil and gas rather than anything EU related. In 2018, growth has picked up with growth faster in the first 6 months of the year than in the UK as a whole.

A ‘no-deal’ scenario

So what might happen in the event of ‘no deal’?

Much of the debate since 2016 has been over a ‘hard’ vs. ‘soft’ Brexit. A ‘no-deal’ Brexit adds an additional element to this – no transition period.

A transition period (up to the end of 2020 on current plans) is seen by many businesses as being crucial in allowing them time to adjust.

Without a deal, the UK and EU would immediately revert to trading under rules governed by World Trade Organisation (WTO) agreements.

Tariffs would be placed upon products entering the EU, and vice versa. For many products, the EU average tariff is relatively low (albeit this could still be the difference between being competitive and uncompetitive). For others, particularly agriculture, the tariffs are much higher.

Non-tariff barriers – the rules and regulations that help deliver the ‘single-market’ and in many cases allow firms in 3rd countries to trade at all with the EU – are likely to be a much more serious impediment for many (e.g. pharmaceuticals, energy and financial services).

At the same time, a no-deal would also see the UK leave the EU Customs Union, requiring an economic border and ‘rules of origin’ checks.

Our work estimates that – over the long-run – a WTO outcome would act as a drag on Scotland’s long-term growth potential.

We estimate that over the long-run, Scotland’s economy under a ‘Canada-type’ model would be around 5% smaller than it would otherwise have been, rising to 7.5% under a hard Brexit.

These estimates were obtained from what is known as a general equilibrium model of the Scottish economy. Such models examine the impacts of major macroeconomic shocks over the long-term.

However, they tell us little about the short-term impact of a ‘no deal’ scenario.

Much will depend upon how ‘chaotic’ a no-deal would be.

The academic unit, the UK in a Changing Europe has documented the various potential impacts in their report “Cost of No Deal: Revisited”.

In the worst-case scenario, they document the potential for aircraft to be grounded; certain products blocked from entering the EU until necessary certificates can be obtained; and border crossings on both sides of the Channel gridlocked as new customs arrangements are put in place.

The UK Government has also set out the potential implications for a range of sectors in a series of technical guidance notes.

What might happen to the economy

One thing that we can be certain of is that the potential hit to sectors and individual firms will vary significantly.

Those that rely upon EU markets, either directly for sales or as part of their upstream or downstream supply chain, will be impacted the greatest.

But what about the Scottish economy overall?

Up to March 2019, there are likely to be two different forces at work.

Firstly, there is a series of factors that may slow the economy even further.

As after the referendum, Sterling could fall further, pushing up inflation and reducing real wages. Financial markets are likely to be volatile. Some have suggested that the UK’s Credit Rating may be downgraded. All of this could lead to a further fall in business and consumer confidence, reducing investment and spending.

Secondly however, there are some countervailing forces that could actually boost growth in the short-run. In particular, if a no deal outcome looks likely, businesses and government may start to prepare for the worst – e.g. stockpiling and contingency planning – and this will help boost growth in the near-term.

What effect dominates is uncertain, but one thing that can be guaranteed is that economic activity is likely to be choppy.

But post-March 2019, the immediate outlook is likely to be much more negative.

Firstly, any boost from stockpiling and contingency prior to March 2019 will gradually be eroded.

Secondly, uncertainty over how long a ‘no deal’ outcome could last might further dampen investment and consumer spending.

Thirdly, and of course most significantly, the actual barriers that a ‘no deal’ outcome would create – in terms of tariffs, customs controls and regulations – would come into immediate effect. The disruption to some export markets and supply chains – for some – could be highly significant.

Whilst it’s important to remember that – at a macroeconomic level – most businesses are one-step removed from international markets, much of what the UK imports are raw materials and semi-manufactured goods that help support business activity across the domestic economy. It’s these ripple effects that will have the greatest macroeconomic impact.

Much will depend upon how the government and Bank of England respond.

The Chancellor has promised a more pro-active Spring Budget in 2019 should action be required to support the economy through any difficult adjustment.

It is also possible that the UK and EU authorities would try to mitigate some of the most disruptive consequences of a disorderly Brexit.

So will the economy enter recession?

The challenge with forecasting what a ‘no deal’ might mean for the economy is the lack of any precedent which can be relied upon to give an idea of the scale of the shock.

So whilst we can be confident that a breakdown of the UK’s economic relationship with the EU will be significant, it’s difficult to attach an exact number to it.

Economies can be resilient to short-term disruptions.

With this in mind, and perhaps burnt by past experiences, few economists have made short-term forecasts for the UK economy post-March 2019 under a ‘no-deal’ scenario.

The OBR, Bank of England and most independent forecasters have stuck to a baseline view that the UK and the EU will secure some form of comprehensive deal.

The OBR did cite the move to the three-day week as an example of a large scale economic shock – which took 3% of GDP in one quarter – whilst also being clear that they were not predicting something similar this time around.

The Bank of England, whilst avoiding specific forecasts thus far, has also outlined its concerns over the potential short-term economic impact. An update is expected next week.

Oxford Economics forecast that, even with support from monetary and fiscal policy, GDP would be around 2% lower than their baseline forecast by 2020 – so positive growth, but very much slower than it would otherwise have been. A similar result is found by the National Institute for Economic and Social Research (NIESR) who predict annual growth close to 0%.

On these forecasts, a technical recession – i.e. two or more consecutive quarters of falling output – whilst by no means a certainty, cannot be ruled out.

So what can we conclude?

A ‘no-deal’ outcome is clearly the worst possible outcome for Scotland. Whether or not this means accepting the deal that is on offer, or seeking an alternative outcome, will be played out in the political corridors of both Holyrood and Westminster in the coming days.

Authors

The Fraser of Allander Institute (FAI) is a leading economy research institute based in the Department of Economics at the University of Strathclyde, Glasgow.