Last week’s quarterly growth figures of 0.8% for the first 3 months of 2017 were the best results for Scotland since 2014 – and much improved on the average quarterly growth of +0.14% during the last couple of years.

In this blog we unpick the sectoral results to see what they can tell us about the balance of growth and outlook.

We also address some recent comments about our own analysis.

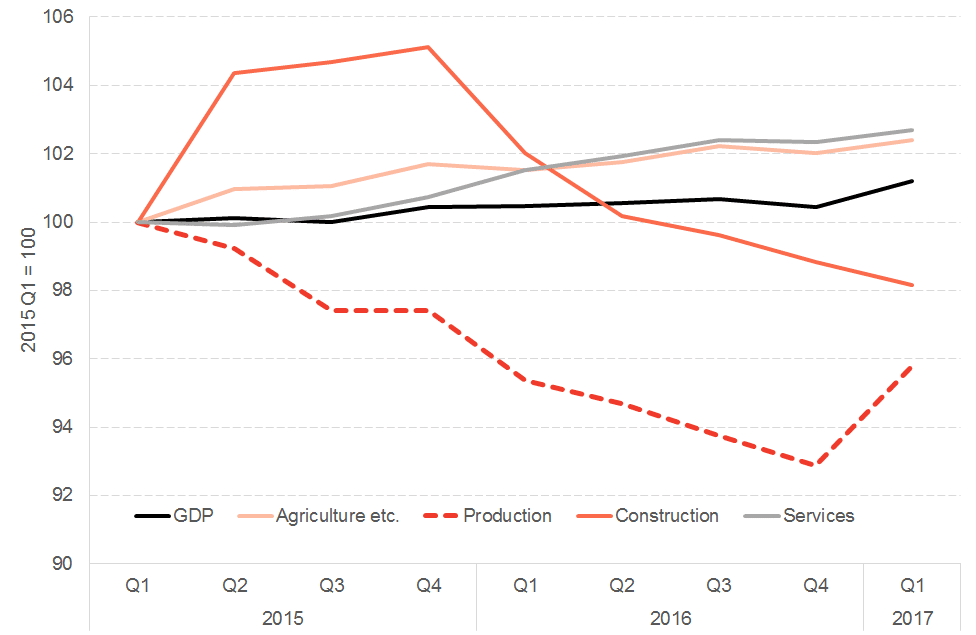

Sectoral Trends – since 2015

The first – albeit rather obvious – point to note is that when an economy is said to have grown by a certain amount, not all sectors will have expanded at the same pace. Some will do better than others.

This chart provides a summary of what’s been happening over the last two years.

Figure 1: Sectoral performance since 2015: Q1 2015 = 100

Up to the end of 2016, production had fallen sharply – down around 7%. Whilst oil and gas has clearly been the major factor, other sectors such as food and drink, computers and electronics, transport and textiles have all been weak. Electricity production has also fallen with the growth in renewables not (yet) fully replacing recent reductions in other forms of generation.

Average quarterly growth in services has also been coming in below trend.

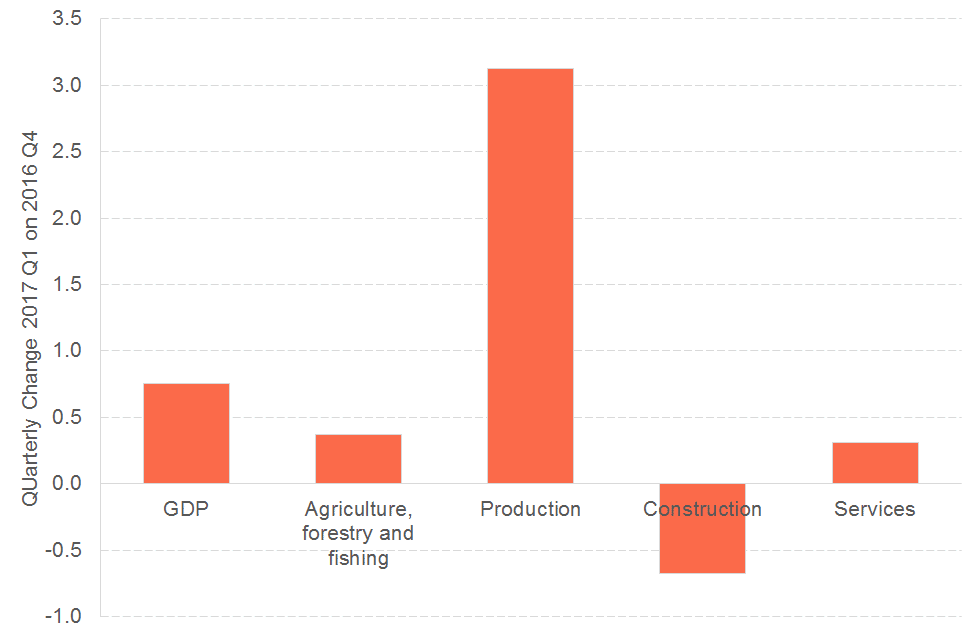

Performance in Q1 2017

For services and construction, which together make up over 80% of the economy, the results were positive but unspectacular.

- Services grew 0.31% – below average growth of greater than 0.4%. Financial services expanded, whilst health and education also grew relatively strongly (offering some interesting interpretations about how public sector output is bearing up in the face of tight budgets).

- Construction fell 0.7%.

In contrast, production grew – for the first time since Q1 2015.

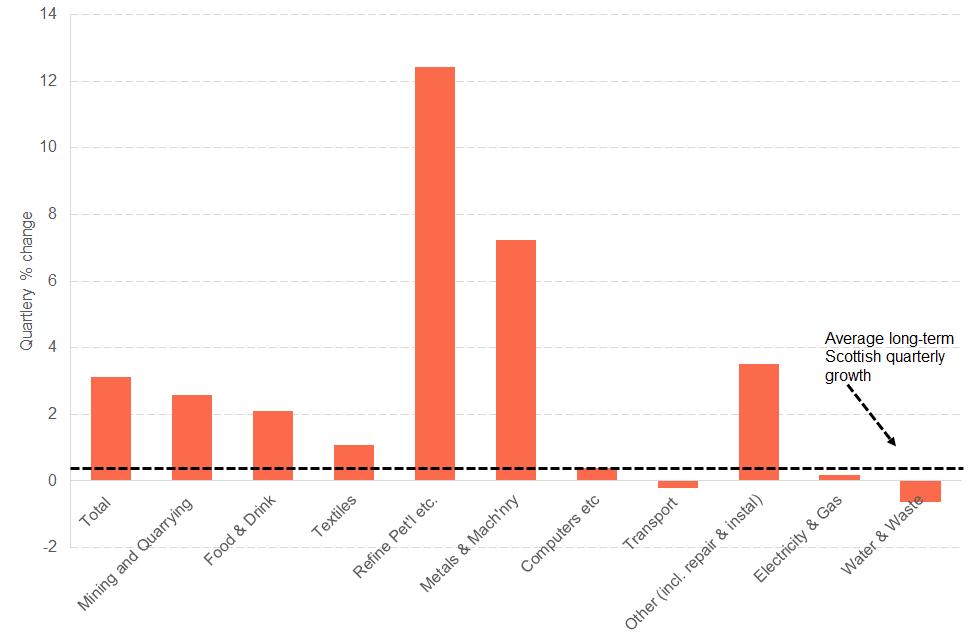

Figure 2: Growth by sector: Q1 2017

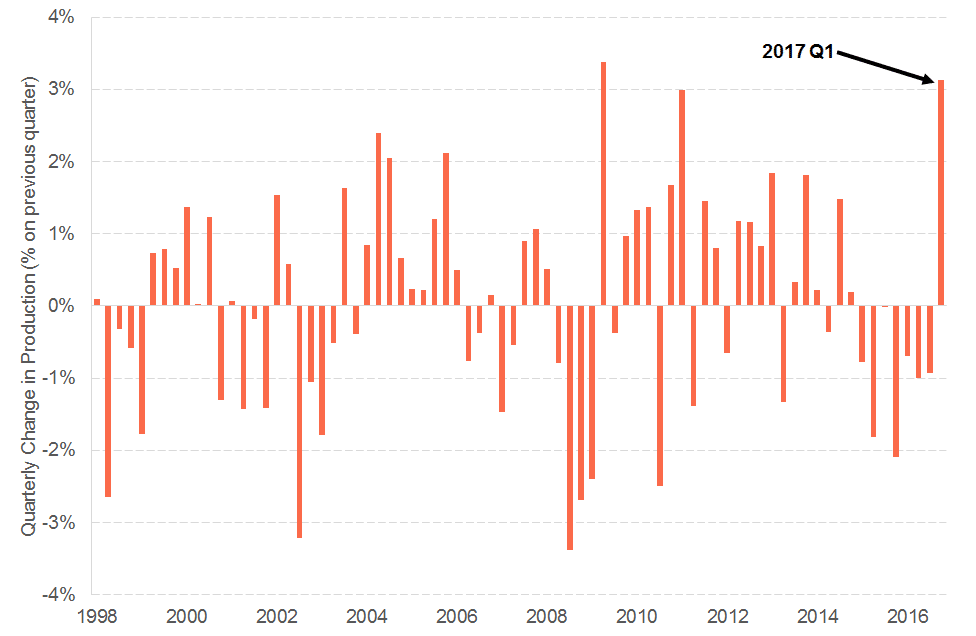

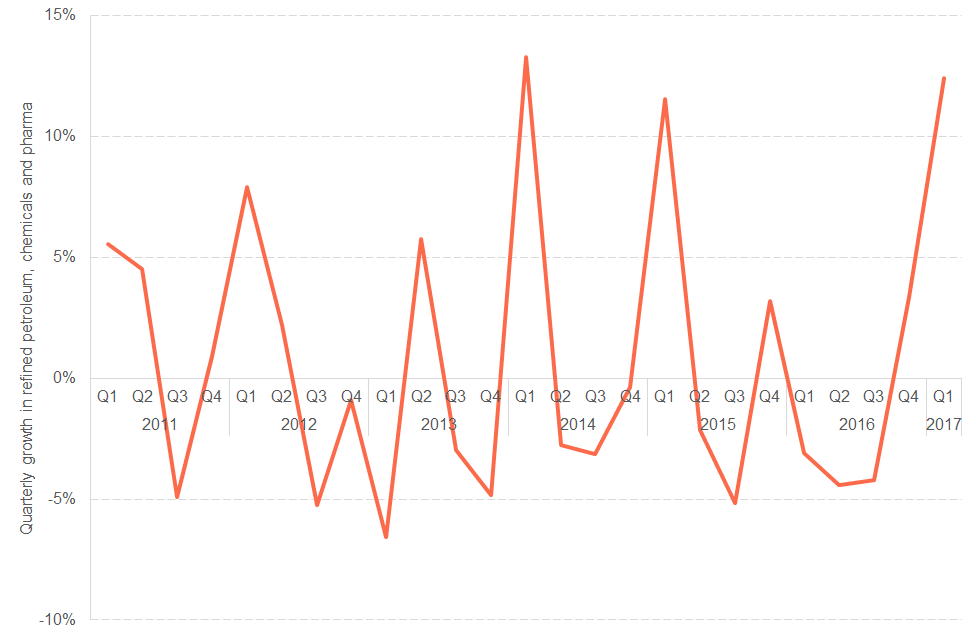

To put Q1’s growth in context, since 1998, on only one other occasion has the production sector grown more quickly in a given quarter. Production statistics – as Figure 3 shows – can be volatile with significant growth one quarter followed by a contraction the next (and vice versa).

Figure 3: Quarterly growth in production output

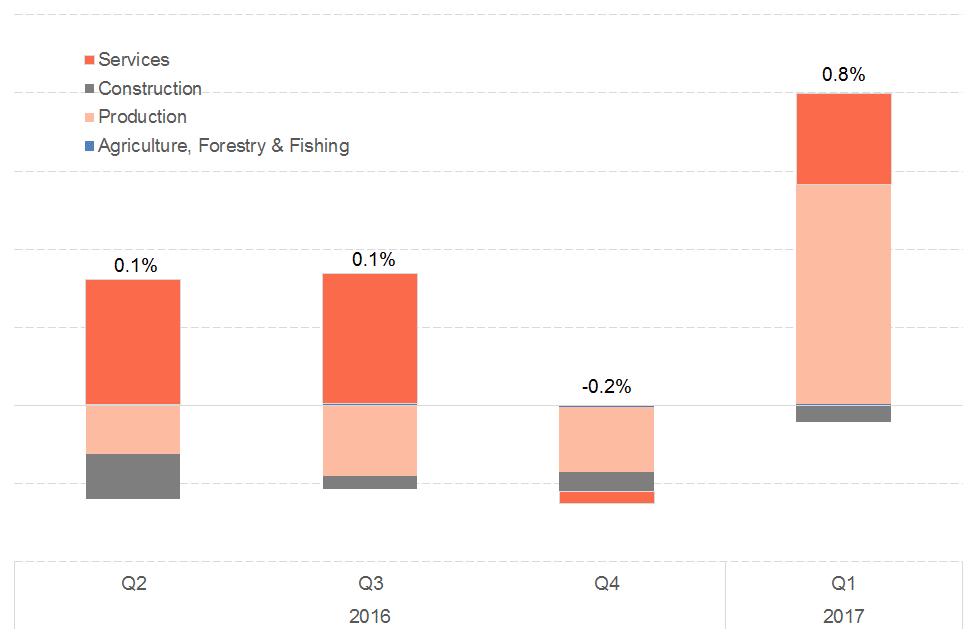

Figure 4 provides a breakdown of the sector split of growth – i.e. how much each sector contributed to the overall growth rate in the economy. That is, of the +0.8% total growth in Q1 2017, how much of this came from services, construction and production

Figure 4: Contribution to growth: Q2 2016 to Q1 2017

Services contributed a net +0.2% points to overall growth – or 25% of the total; construction and agriculture had little impact (and might not be visible on the chart).

The remaining 0.6% points – or 75% of net growth – came from production.

Half of the net growth in the Scottish economy in Q1 came from sectors which together comprise just 6% of the Scottish economy

What is particularly interesting are the industry-by-industry results for the production sector.

Figure 5: Production industry performance in Q1 2017

Both mining & quarrying and food and drink grew strongly – up 2%.

But by far the most interesting results concern three sectors – ‘metals & machinery’, ‘refined petroleum, chemicals and pharmaceuticals’ and ‘other manufacturing, repair and installation’. This final category includes activity supporting the maintenance of oil platforms including decommissioning.

Combined, these 3 sub-sectors comprise 6.1% of the Scottish economy.

On this occasion they are estimated to have grown by such an amount that they accounted for around half of the entire net growth witnessed in Scotland during the first three months of the year.

There are a number of reasons for this.

Firstly, as our own surveys have highlighted confidence has been improving in the oil and gas supply chain. The data appear to indicate that this has fed through to actual activity in ‘metals and machinery’ and ‘other manufacturing’. But the scale of this turnaround – particularly in just one quarter – suggests this is only part of the explanation.

So the second reason given has been the re-opening of the Dalzell steel plant. Hopefully, and as in the past when major industrial facilities have been turned ‘on’ or ‘off’ or there have been ‘special events’, the statisticians will publish their analysis of what proportion of growth can be attributed to this plant vis-à-vis a general pick-up in activity.

As highlighted, when quarterly production growth has spiked, it has often been followed by a contraction next time. The hope this time will be that, by reflecting an improvement in optimism and/or new business models at key industrial plants, the outlook will be one of growth rather than any fall-back.

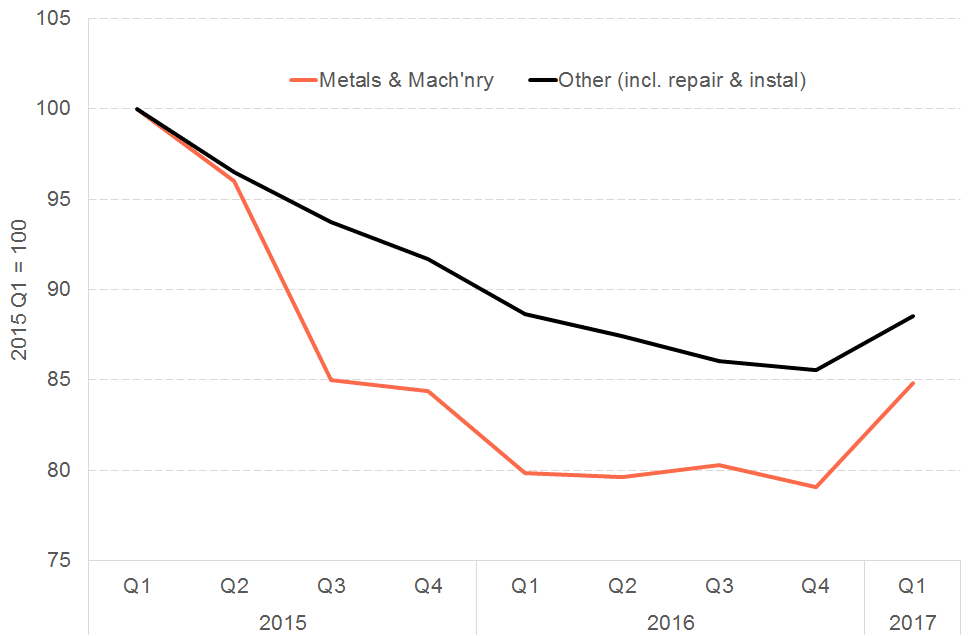

There is still ground to make up – see Figure 6. For example, output in the Metals and Machinery sector is still 15% below where it was in Q1 2015.

Figure 6: Metals and machinery and ‘other manufacturing’ (including installation): since Q1 2015

The third reason, and one area we would urge caution given its volatility, difficulty in measurement and interaction with the wider real economy, is the growth of over 12% in output from the refined petroleum, chemicals and pharmaceutical sector (which is largely driven by Grangemouth). This contributed nearly 20% (i.e. 0.16% points) to the overall net growth rate in Q1 for the entire economy.

Figure 7: Quarterly change in measured GVA from refined petroleum etc.

Conclusions

Three key conclusions can be drawn:

- For the 80+% of the economy made up of services, construction and agriculture, whilst there were some individual bright spots, overall growth was positive but unspectacular.

- The production sector led the rise in growth. Indeed, half of the net growth in the Scottish economy in 2017 Q1 came from 3 sub-sectors – bouncing back (but not fully) on the losses made over the last two years. A degree of success will be to hold on to the gains made this quarter.

- Of much greater significance will be the extent to which recent changes in individual manufacturing operations can evolve into a sustainable platform for jobs and investment over the medium to long-term.

Finally, some rather surprising comments have been made in the media in respect of our own analysis following Wednesday’s statistics.

To be clear, the GDP figures for Q1 2017 are entirely consistent with our assessment of the health of the Scottish economy set out in our recent reports and analysis.

Our expectation is that Scotland’s economy will grow this year; will do so more quickly than last year; but that growth will remain fragile. Total employment is expected to hold up but real incomes will remain under pressure.

We see nothing in Wednesday’s results to alter that view.

The improvement in sentiment identified in our oil and gas surveys was a key reason we raised our forecasts as far back as in December. How this improved confidence actually transpires into quarterly GDP statistics will always be uncertain which is why we forecast over the year as a whole. Indeed if the growth made in Q1 2017 can be held on to and subsequent quarters can hit their long-term average growth rate during the remainder of the year, annual 4Q-on-4Q growth in 2017 will be 1.2% – identical to our central forecast.

But it’s important not to lose sight of the fact that the Scottish economy has had weak growth for two years now.

The explanation for this is not down solely to the North Sea, as this quarter’s data once again outlined. And whilst, on balance, we thought growth would return in Q1, experience suggests that a pick-up in one quarter is no guarantee of sustainability – particularly after growth of 0.0%, 0.1%, 0.1% and -0.2% in 2016.

With volatility in a small number of sectors, large swings (positive or negative) in quarterly results are highly possible. As we have repeatedly made clear, in such times, whether or not the quarterly figures are above or below the line is largely unimportant, what is much more important is the longer-term trend.

In this respect, with current annual growth of 0.5% versus UK growth of 1.9%, Scotland’s economy remains in a position deemed sufficiently serious to unlock the emergency borrowing powers under the new Fiscal Framework. On any reasonable assessment, such a baseline, coupled with a likely renewed squeeze on household incomes across the UK, weak consumer confidence and positive (but still fragile) business activity indicators – not to mention any risks emerging from the Brexit negotiations – means that the Scottish economy remains in a challenging position.

So whilst Q1’s results are clearly welcome, and hopefully a sign of better things to come, there is clearly still much progress to be made.

With that in mind, the best course of action is to focus on the long-term drivers of growth and to be ambitious about tackling the structural challenges that exist in our economy, maximising our comparative advantages in areas like skills, natural resources and key sectors, and taking advantage of the opportunities that will exist in new markets and technologies in the years to come.

Authors

The Fraser of Allander Institute (FAI) is a leading economy research institute based in the Department of Economics at the University of Strathclyde, Glasgow.