Today’s ‘fiscal event’ contained some of the most substantial tax policy changes seen in recent decades. Combined with last week’s announcements on the Energy Price Guarantee and Energy Bill Relief Scheme, this constitutes a huge change in the fiscal outlook.

In this context, the decision not to involve the Office for Budget Responsibility (OBR) is irresponsible. It might be billed as a ‘Growth Plan’, but today’s announcements are a budget in all but name. The OBR plays an essential role in scrutinising tax and spend forecasts, assessing the likely impact of policy announcements on growth, the deficit and debt. Its exclusion from the process weakens transparency around the impacts of the proposals.

The new Chancellor used the first part of his speech to reiterate the government’s unavoidably large interventions in the energy market to protect households and businesses from energy price rises. In the remainder of the speech he announced a host of measures designed to stimulate economic growth through a combination of tax cuts and regulatory changes.

Tax changes – implications in Scotland

There were two ‘tax cuts’ that are more accurately described as reversals in recent or planned increases.

- A planned increase in the Corporation Tax rate from 19% to 25% will now not go ahead. The Treasury estimates this will cost £12bn in reduced revenue compared to its previous plans in 2023/24, and more in subsequent years.

- The Health and Social Care Levy has also been scrapped, together with the 1.25% increase in dividend tax rates. These changes will cost almost £18bn in reduced revenues in 2023/24 compared to previous plans.

Both of these changes had been pre-announced and apply UK-wide.

The big surprises came on income tax. Here the government announced the biggest reforms (at UK level) since 2009.

- The basic rate will be reduced from 20p to 19p one year earlier than expected, applying from April 2023 rather than April 2024.

- The 45p additional rate will be abolished in April 2023.

Income tax changes and implications for Scotland

Of course, with income tax being devolved, neither of the changes will apply in Scotland. Instead, the Scottish Government will see a smaller reduction in its block grant next year than it was expecting, boosting the resources available to it in 2023/24 (the reduction to the Scottish Government’s block grant is broadly designed to reflect what the UK government would have raised from income tax in Scotland if income tax had not been devolved, and if the UK government income tax policy had continued to apply in Scotland).

In the context of this additional resource through its block grant, the Scottish Government will then need to decide whether and how to respond through its own tax policy.

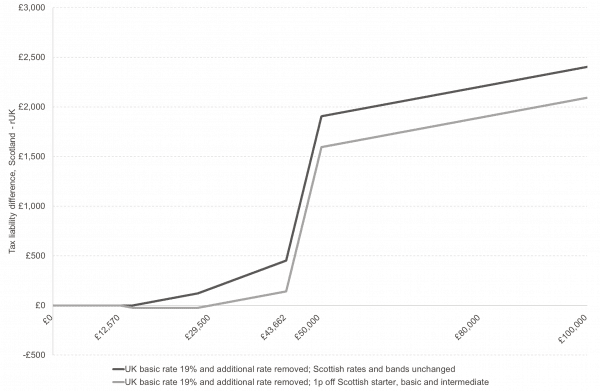

It could of course keep Scottish tax policy unchanged. This would enable it to use its additional block grant to invest in public services in Scotland. The cost of it doing this politically would be that the gap between Scottish and rUK tax policy would widen substantially. Almost all Scottish income taxpayers would pay more income tax than they would in rUK. A Scottish taxpayer with an income of £29,000 would face liabilities around £160 higher. A Scottish taxpayer with an income of £50,000 would face liabilities almost £2,000 higher (Chart 1, black line).

Chart 1: Potential difference in income tax liability between Scotland and rUK, in 2023/24

Alternatively the Scottish government could mirror UK tax cuts with tax cuts of its own. It could for example decide to reduce the starter, basic and intermediate rates by 1p. This would broadly retain the difference in tax liability for individuals between Scotland and rUK at current levels (Chart 1, grey line). It would allow the Scottish Government to retain its treasured mantra that ‘the lowest income half of Scottish taxpayers pay less tax than they would in rUK’. But such a policy would cost the Scottish government around £400m in foregone revenues.

Other policy decisions are possible. The Scottish government could decide to cut just the starter and basic rates in Scotland, rather than the intermediate rate as well, at a revenue cost of around £250m.

How the Scottish Government responds to the UK Government’s abolition of the Additional Rate will also be interesting. The Scottish Fiscal Commission is likely to forecast that abolition of the Additional Rate wouldn’t be extremely costly in revenue terms (there are expected to be around 22,000 Additional Rate taxpayers in Scotland in 2023/24 so charging them a few pence less tax on their income above £150k might not have a significant affect in aggregate, particularly if it is assumed, as the SFC will, that the tax reduction will induce some element of a positive behavioural response).

The Additional Rate policy therefore puts the Scottish Government in a difficult political position. If it retains the Additional Rate it will be accused of undermining the ‘competitiveness’ of the Scottish economy, for little direct revenue gain (without any changes to existing policy, a taxpayer with an income of £200,000 would face an additional £5,900 in income tax liabilities in Scotland compared to an equivalent taxpayer in England).

But abolition of the Additional Rate would provide a significant tax cut for the highest income 0.5% of the Scottish adult population (an individual with income of £200,000 would be better off to the tune of £2,500 if the Additional Rate is abolished). The regressivity of a cut to the top rate in Scotland is difficult to reconcile with the Scottish Government’s aspirations for progressivity.

Stamp Duty changes and implications for Scotland

The Chancellor also announced changes to Stamp Duty in England and NI, amounting to an increase in the threshold at which Stamp Duty applies to residential transactions.

As with income tax, these changes will not apply in Scotland. As with income tax, the changes to English policy will pose dilemmas for the Scottish Government when considering its policy on the Land and Buildings Transaction Tax.

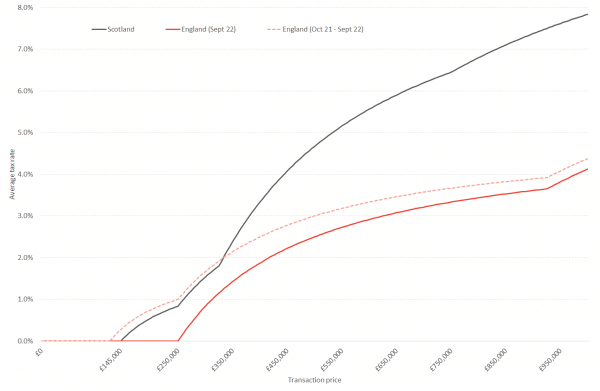

The Scottish Government has until now set LBTT in such a way that homes sold in Scotland for less than around £335,000 pay less tax than an equivalent property in England. Above this price, transactions in Scotland face noticeably higher tax liabilities. The changes announced by the UK government today mean that – if there are no changes to the existing Scottish LBTT rates – all property transactions in Scotland would face higher tax liabilities than they would in England (see Chart 2).

The Stamp Duty cuts in England will generate some additional resources for the Scottish Government via its block grant. In ballpark terms the increase in resource might be around £80m. It could use this additional resource to fund public services, or to cut LBTT rates in order to maintain existing tax differentials.

Chart 2: Residential property transactions tax liabilities in Scotland and England

Investment zones – an option for Scotland but at what cost?

The UK government announced the establishment of several dozen ‘investment zones’. It is hoped that these zones will ‘drive growth and unlock housing… by lowering taxes and liberalising planning frameworks’.

Policies implemented within the investment zones will include business rate reliefs for newly occupied or expanded premises, and stamp duty relief on land bought for commercial purposes, and a zero-rate of employer National Insurance Contributions for new employees earning below £50,270.

The hoped-for impacts of these investment zones on UK-wide economic activity – as opposed to their effect on displacing economic activity within parts of the UK – is based more on hope than on empirical evidence.

Several dozen potential zones have been identified in England. The UK government says that it will work with the Scottish government and local authorities to identify zones in Scotland.

What is not yet clear is how the costs of investment zones in Scotland – in the form of reliefs on business rates and stamp duty (which are devolved) and NICs reliefs (which are not devolved) – will be distributed between the Scottish and UK governments. The Treasury’s costing document does not seem to give an indication of the funding associated with the planned investment zones in England, so it is difficult to get a sense of the fiscal scale of these interventions at this stage.

U-turn on IR35

In another regulatory reform design to unlock growth, the chancellor announced the repeal of the anti-avoidance legislation commonly known as IR35. This legislation was designed to reduce so-called “disguised employment”, whereby workers could work long-term for businesses as self-employed contractors rather than employees – and in so-doing reduce the tax liabilities faced by both themselves and the company that they were contracted to.

The IR35 regulations were introduced for public authorities in 2017, and for medium and large enterprises in 2021. The regulation has big impacts on the nature and shape of the workforce in particular sectors.

The introduction of IR35 has been a huge undertaking by public authorities and corporations to ensure compliance with the legislation, so the change announced today is a big deal. It is a shame that we don’t have the view of the OBR of the impact this could have on Income Tax and National Insurance Contributions: but the costing published today by the Treasury suggests it could cut tax receipts by £1.1 billion in 2023-24, rising to £2 billion by 2026-27.

The Energy profits levy – the existing windfall tax

Interestingly, although the Prime Minister has made it clear that additional windfall taxes were not going to be introduced on oil and gas companies, we need to remember that the Energy Profits Levy announced in May is still in place.

This is a 25% additional surcharge on the extraordinary profits that are being made by the oil and gas companies. When it was announced in May, it was expected that this could raise £5 billion this year, although there was a great deal of uncertainty about this.

Under current plans this levy will remain in place until December 2025, and on the basis of the costings published today, the Government has no plans to end it early. The policy is now forecast to raise £28 billion over the next 4 years (including this year). This is another area of costing that it would be particularly useful to get independent scrutiny from the OBR.

Summary: a gamble on growth with long odds

It is undeniably the case that the UK (and Scottish) economies have been characterised for the last 15 years by very weak growth. This has resulted in stagnation in household incomes and living standards, and constrained the growth of government revenues – with implications for investment in public services.

It makes sense therefore for the government to put the objective to raise economic growth at the centre of its strategy. But setting a 2.5% annual growth target, as the UK government has done, is much easier said than achieved.

The government’s decision to reverse the Health and Social Care Levy and cancel the planned Corporation Tax increases merely take policy back to where it has been in the recent past. It is a return to orthodoxy rather than a break from the norm, and in this sense it is difficult to see that it will make any difference to growth.

The substantial cuts to income tax do represent a bigger change to existing policy. But the hope that these will stimulate the economy is based more on blind faith than on any tangible evidence. There is no evidence internationally that countries with lower tax rates grow more quickly. Historically, UK growth rates were highest when tax rates were higher.

Whether today’s announcements unleash economic growth remains very much to be seen. Strikingly, what there was no mention of today was any plans for additional public sector investment. Despite the government’s rhetoric about reforming the ‘supply-side’ of the economy, there was little mention of the role that the skills and health of the population play in influencing the capacity of the economy to grow.

Whilst the government seems comfortable borrowing an additional £30bn or so a year to fund the tax cuts announced today, and is apparently relaxed about an over-growing burden of national debt, the path set out today will constrain the government’s room for manoeuvre on investment in public services in coming years.

At a time when parts of the public sector are struggling to deal with the legacy of the pandemic and other longstanding challenges, the implied prioritisation of tax cuts over public services investment will prove highly contentious, particularly given the regressivity of the cuts. Households in the top 10% of the income distribution in Scotland will be better off by around £24 per week on average as a result of the cancellation of the Health and Social Care Levy, whereas those in the middle of the distribution will be only £4 per week.

The hope that the policies announced today will boost growth and hence revenues despite cuts in tax rates is a big gamble with long odds.

Authors

David Eiser

David is Senior Knowledge Exchange Fellow at the Fraser of Allander Institute

Mairi is the Director of the Fraser of Allander Institute. Previously, she was the Deputy Chief Executive of the Scottish Fiscal Commission and the Head of National Accounts at the Scottish Government and has over a decade of experience working in different areas of statistics and analysis.

Ben is an Economist Fellow at the Fraser of Allander Institute working across a number of projects areas. He has a Masters in Economics from the University of Edinburgh, and a degree in Economics from the University of Strathclyde.

His expertise lies in various economic modelling approaches, social care, and evaluating social impact for organisations across the private, public and third sector, particularly where evaluation requires intuitive approaches.

Calum Fox

Calum is an Associate Economist at the Fraser of Allander Institute (FAI) and a Researcher at the Centre for Inclusive Trade Policy (CITP). He specialises in economic modelling and trade, and holds an MSc in Economics from the University of Edinburgh.

Ciara is a Knowledge Exchange Fellow at the Fraser of Allander Institute. Her main area of focus is macroeconomic and fiscal analysis. She has recently completed a secondment to the Scottish Fiscal Commission, where she worked as an Economic and Fiscal Analyst in the economy team forecasting macroeconomic conditions.

Emma Congreve is Principal Knowledge Exchange Fellow and Deputy Director at the Fraser of Allander Institute. Emma's work at the Institute is focussed on policy analysis, covering a wide range of areas of social and economic policy. Emma is an experienced economist and has previously held roles as a senior economist at the Joseph Rowntree Foundation and as an economic adviser within the Scottish Government.

Jack is an associate economist at the Fraser of Allander Institute.