There is a great interest in data that can provide timely information on the impact of the Coronavirus pandemic on the economy and ultimately the living standards and wellbeing of the population.

One of the challenges is that, unlike many of the health measures that can be used to track the impact of the virus (such as hospital admissions etc.), economy measures aren’t as straightforward to collect or interpret.

Indeed, and unfortunately, traditional economic statistics, such as GDP, often aren’t the most useful at such times. They are published with a lag, they are built upon ‘sectors’ as defined by national accounts rather than type of business activity (which is most relevant for social distancing), and they are subject to a greater margin of estimation error than normal.

Moreover, the nature of this crisis means that we will see large swings in such measures. It’ll be important to interpret them carefully and to avoid reading too much into one month or quarter of data, but instead to look at the longer-term trend.

For example there is usually a reasonable link between movements in aggregate output and in overall employment, but we know that GDP is taking a hit through the present crisis while its effect on employment (which we care more about in many ways) is being cushioned through the policy measures that have been adopted.

Traditional economic statistics also don’t measure things that might be of particular interest to policymakers at the current time, for example the risk of collapse and insolvency.

So instead, we have to rely upon different types of data and information gathering to build up a picture of the economy.

Here we produce a summary of some of the data for Scotland and highlight key gaps.

As an aside, we’re seeing a lot of interesting developments to improve up-to-date information on the economy. The ONS’ new weekly update is a vital source of information. We’re also seeing new datasets being used for the first time, such as mobile phone tracking. And there are many excellent summaries (see the Resolution Foundation here).

Economic activity

With traditional measures of activity suffering from a lag, business surveys are a vital indicator of current conditions. Some caution needs to be exercised, as they can ‘overshoot’ (e.g. after the EU referendum) and at such times the overall scale and direction of travel is more important than a specific point estimate.

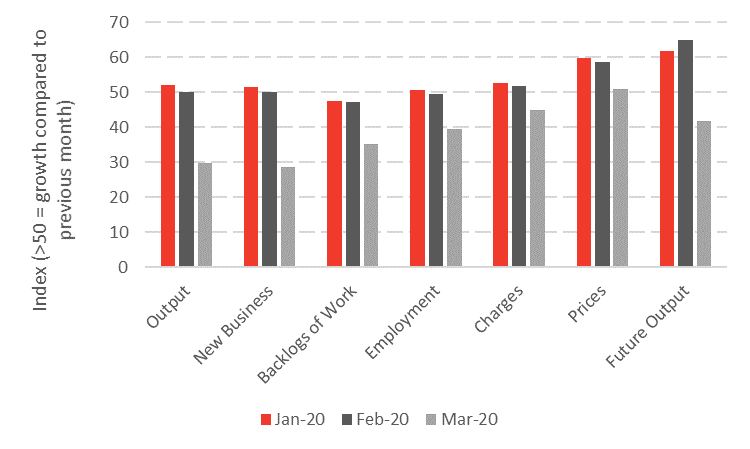

The most recent Scottish Purchasing Managers Index (PMI) – 15 April – showed that private sector activity in March declined at the fastest rate since the survey began in 1998.

Chart 1: Composite PMI indicators for the Scottish economy

Source: Royal Bank of Scotland, IHS Markit

This echoes our own Scottish Business Monitor. We found that the number of firms seeing an increase in their volume of business during Q1 2020 fell to its lowest level since Q1 2009. The outlook for the next six months is even more stark, with the survey recording its worst result since it was first launched in 1998.

In a welcome development, the Scottish Government has announced plans to produce a Monthly Business Index (MBI) and Monthly GDP estimates (mGDP). This will provide a much earlier measure of economic activity.

Care will be needed in interpreting such data, however. Scottish GDP statistics are naturally more volatile than for the UK given the relative size of the Scottish economy and breadth of data coverage that statisticians can draw upon. Moreover, introducing such new data at a time of volatility in the economy increases the risk that the statistics will be subject to an unusually large margin of error.

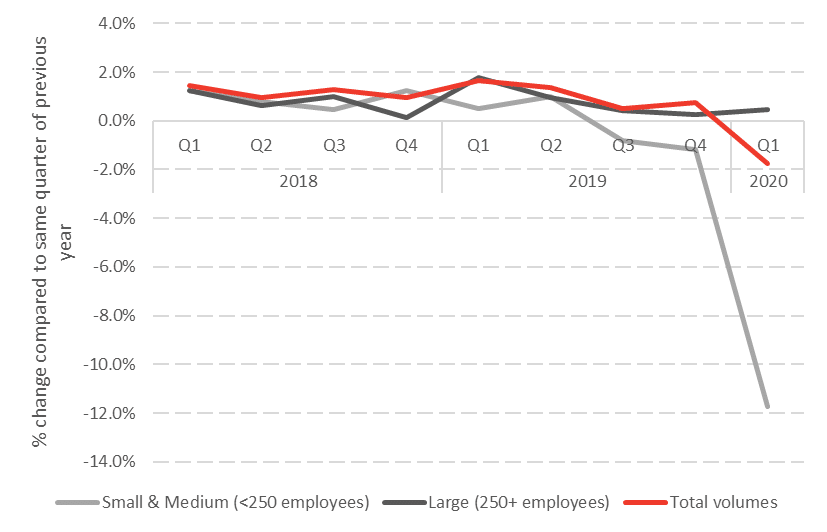

As time goes on, we’ll start to get more ‘official’ statistics. Last week, retail sales data was published by the Scottish Government for Jan-Mar (so covers the emerging shutdown).

As Chart 2 shows, there was an overall fall in volumes over the quarter, with a disproportionate hit to small and medium sized retailers. It is possible to speculate that the holding up of sales within larger businesses has been driven by supermarkets and the stock-piling of goods that we saw in March.

Chart 2: Volume of retail sales in Scotland, by size of business

Source: Scottish Government

Wider indicators

Beyond survey data and the like, we have seen a rise in ‘other’ sources of data which offer an insight on how the economy is performing at the current time.

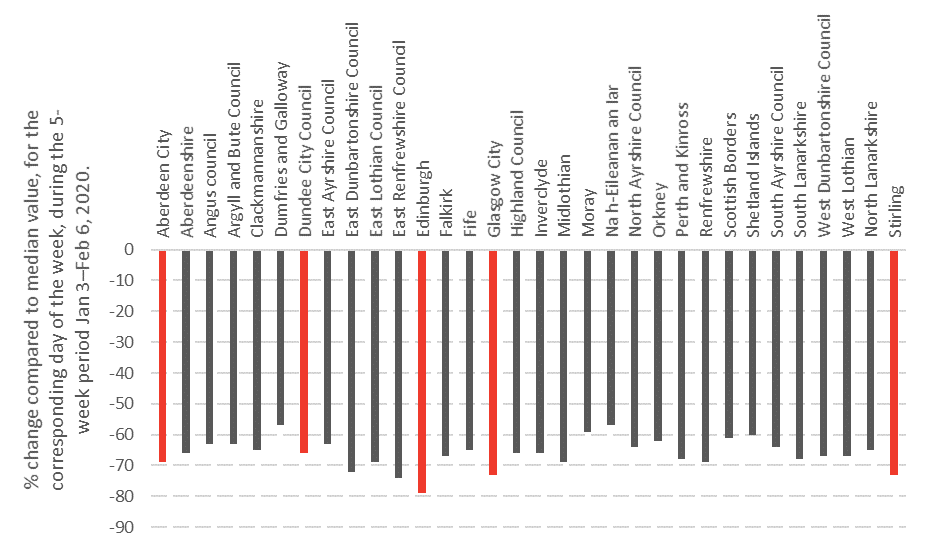

Chart 3 presents data from Google showing the percentage change in people travelling to their normal workplaces on Thursday 23rd of April with a pre-Covid baseline (based on anonymised data of people who have location history enabled) by local authority.

The declines are extraordinary with major falls across every local area. Edinburgh has seen the biggest fall in people travelling to work – close to 80%. Even Dumfries and Galloway and the Western Isles has seen drops of 57% according to this data.

Chart 3: Proportion of people travelling to workplaces compared to pre Covid-19 baseline

Source: Google Covid-19 Community Mobility Data

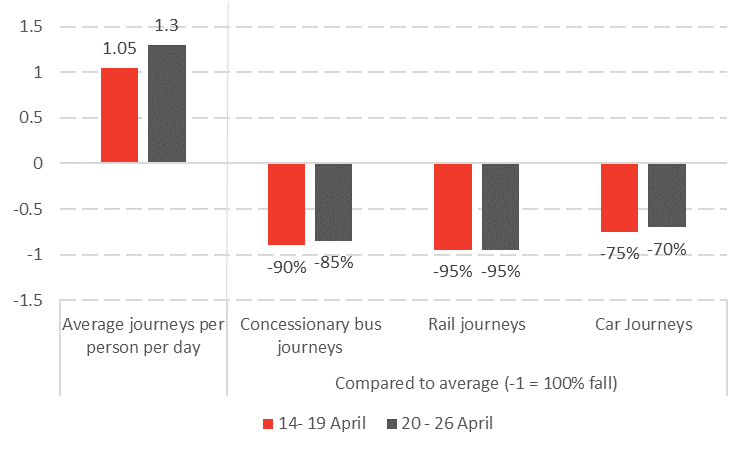

Similar trends are being picked up in transport data – see Chart 4 – with operators working at a fraction of normal demand.

Chart 4: Average journeys per person per day; transport usage compared to average

Source: Transport Scotland

So, it is clear that the economy is operating at levels way below capacity.

Households and individuals

So that covers the economy as a whole.

As yet, we have little data to show us how households and individuals are faring in Scotland.

The next labour market data will be published on 19th May. This will cover the 3-month period up to March. It might be a little earlier to pick-up much major movement in unemployment or employment, but it will be worth watching. At this stage it is unclear how furloughed workers, or those due to receive self-employment support, will be recorded.

The substantial rise in Universal Credit claimants is an important indicator, pointing to the loss of a large proportion, if not all, of claimants’ earned incomes. According to the DWP between the 24th of March and the 28th April, close to 1.5 million additional UK households had claimed Universal Credit. The only Scotland data available runs up to the 8th April where new claims increased by 61,000 (compared to 767,000 UK wide).

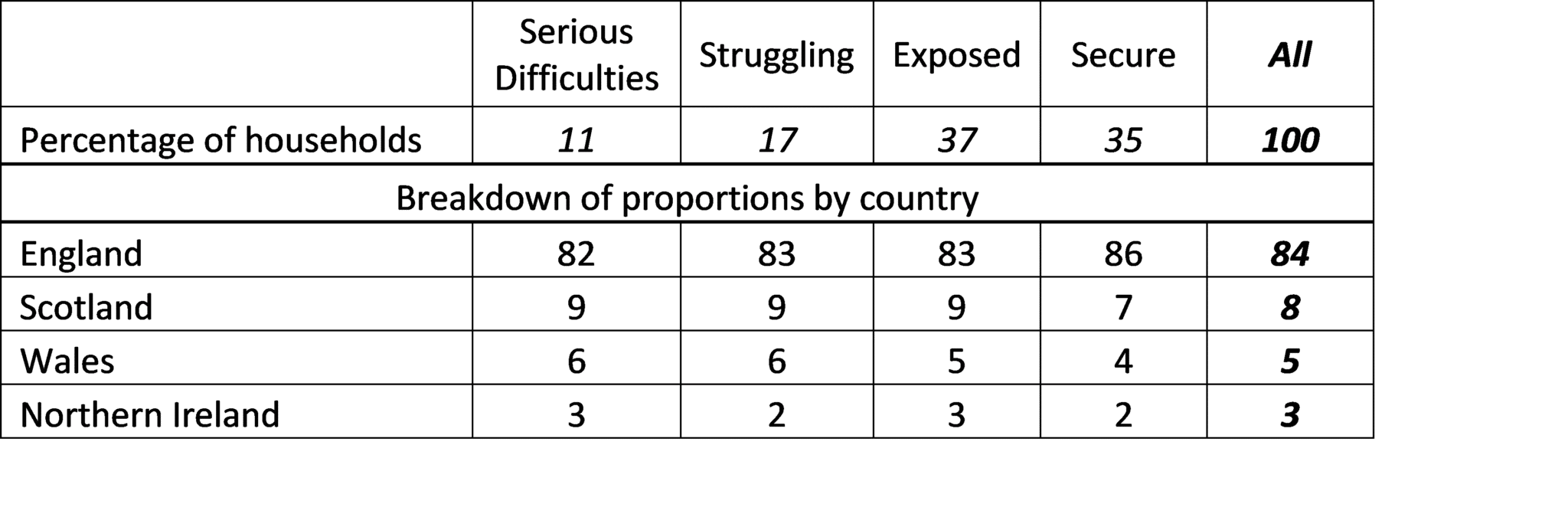

Another timely source of information on household finances for the UK came from a new survey published by the Standard Life Foundation. Headline results include that an estimated quarter of all people in the UK have lost a substantial part or all their earned income, with 28% experiencing financial difficulty. Scotland made up 8% of the sample, but as yet we haven’t got a full breakdown of Scottish results apart from a disaggregation of respondents to questions about financial wellbeing. The results, and other commentary in the report, suggest that responses Scotland are broadly in line with other parts of the UK.

Table 1: Disaggregation of responses to question on financial wellbeing

Source: Standard Life Foundation

Data Gaps

So a picture is starting to emerge of how the economy is faring. And more data will be released in the near future.

But there are gaps.

Most importantly, little is known about the situation within businesses at the current time – on issues such as cashflow, working capital debt etc.

It is this that is absolutely crucial at this time. But there is very little information on this available (NB: in this regard the current situation mirrors many aspects of recent economic shocks – e.g. the financial crisis of 2008-09 and the oil downturn in 2015-16 where crucial information on bank balance sheets and the links between oil and the real-economy were difficult to measure).

At the same time, traditional measures such as GDP etc, by failing to capture these underlying issues within businesses, might significantly under reported the scale of the risk that our economy faces (even if they are produced on a more timely basis).

With this in mind, the ONS responded quickly. They immediately launched a Business Impact of Coronavirus (COVID-19) survey asking detailed questions on how businesses have responded in terms of furloughing staff, how their turnover has been impacted and variations by sector.

Sadly, no data is available for Scotland either from within this survey or from an equivalent exercise by the Scottish Government.

The ONS deserve a lot of recognition for the way they have responded to the need for data and evidence during the current crisis. For example earlier this week they published a set of data looking at the effect of this crisis on people’s personal and economic wellbeing – something the Scottish Government will no doubt look at with some interest.

On business balance sheets, the data is even more limited.

Our Business Monitor found that when we asked businesses how long they could survive under current levels of trading, of those who responded to this question, 54% said less than three months while a further 32% said they could survive for four to six months. This is a worrying statistic, so tracking this over time will be vital.

Similar results were found in last week’s Scottish Chambers of Commerce coronavirus tracker. Almost half of companies (48%) responding to the survey said that current cashflow levels will only cover them for a period of up to or less than 3 months

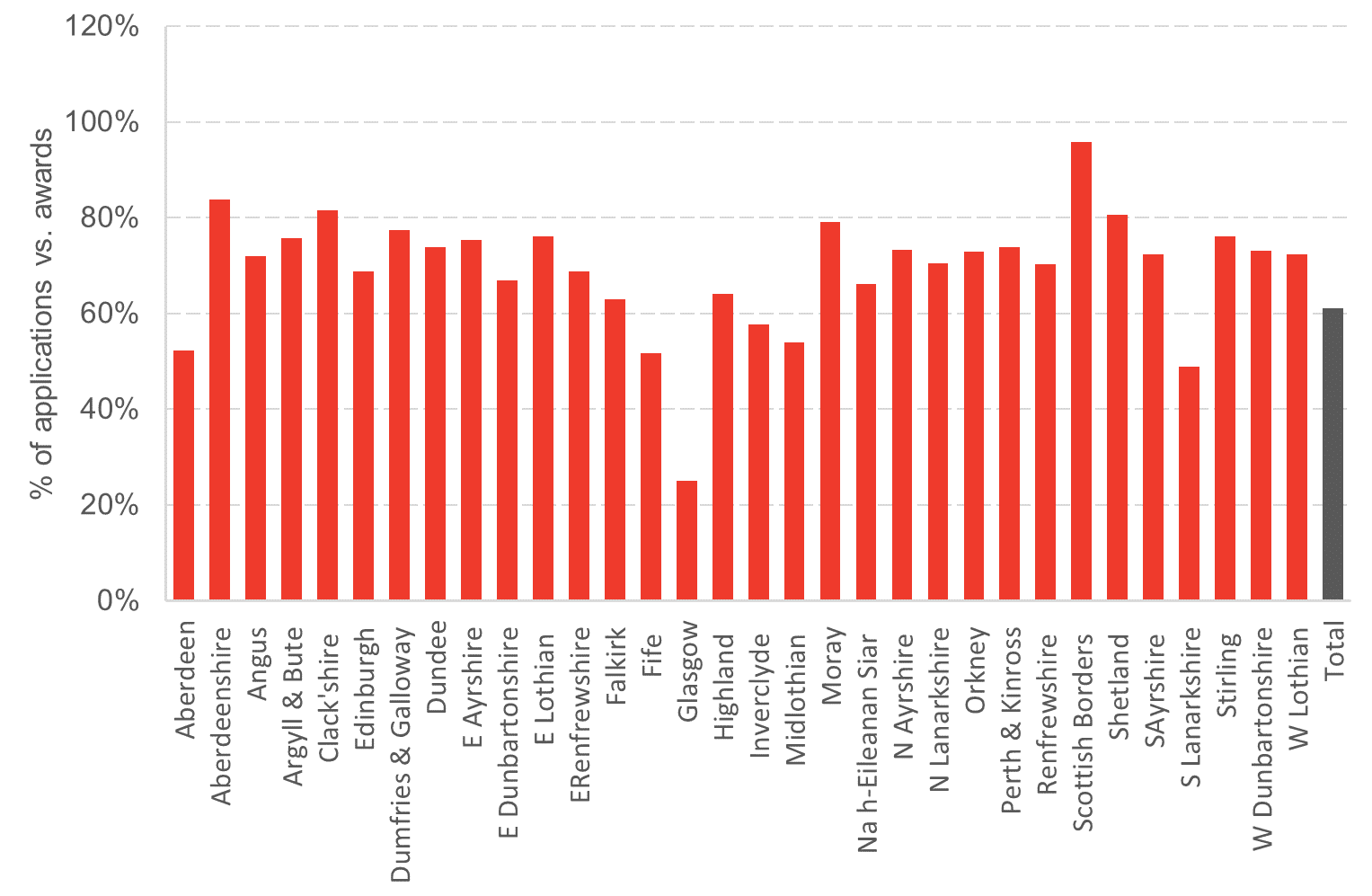

In time, we’ll start to get more information on take-up of government support. Last week the Scottish Government published data on numbers of applications and awards by local authority for business support.

Chart 5: Percentage of applications for business support receiving an award*

Source: Scottish Government

* Note: nature of data collection is such that results are subject to uncertainty at this stage, so it will be important to track over time.

There is a lot of emerging data on how COVID-19 is impacting upon the economy and business. Unfortunately, the nature of much of the ‘official’ data collected as national statistics isn’t that helpful at the current time. One implication of this crisis therefore is that it is only likely to accelerate the drive for new ways of tracking our economy in real time.

Understanding how economic crises translate to Scottish households and individuals is critical in being able to design appropriate support, but data here is very limited. Despite the UK Statistics Authority writing to DWP to ask for more information to be included in published management data on Universal Credit this hasn’t yet happened. Over the next few months, there will be official data released that covers Scotland, but this is of little comfort to families who are in financial distress and need support now.

Indeed, it will be a number of years before we get the ‘official’ view on how household finances have coped. As with economy and business data, more real-time information on where, and to whom, the greatest financial impact is being felt is crucially important in times like these.

We’ll update these summary measures in the weeks to come.

Authors

The Fraser of Allander Institute (FAI) is a leading economy research institute based in the Department of Economics at the University of Strathclyde, Glasgow.