Recently we published an article looking at the emerging indicators of impacts of Covid-19 on the Scottish economy. In this article we look at some further timely indicators tracking the impact the Coronavirus is having on different parts of the Scottish economy including the impact on households and individuals.

The economy has been used as a tool to fight the spread of the virus by effectively mothballing large amounts of business activity. Despite recent pronouncements in England, this strategy is continuing in Scotland for the time being. Therefore, it is of no surprise that we are still seeing economic indicators pointing downwards (often to unprecedently low levels). This is inevitably translating to financial hardship for a great number of households and individuals, but the support put in place through schemes such as the Coronavirus Job Retention Scheme will be making a significant difference for many.

As we noted in our previous article, regular measures of the economy from sources such as GDP often aren’t the most useful at times like this as they miss out the nuances of what is happening to some of the most affected parts of the economy, and in particular, where we may be seeing signs of permanent scarring. They are also produced with a lag that makes them less useful for real time policy making during a crisis. Other indicators such as stock market trends are similarly of little value too as their movements are impacted greatly at this time by market sentiment and trends outside of Scotland.

We therefore need to look at other indicators that will help us do this. As we mentioned previously, the ONS have been on the front foot with this, and have a regular Business Impact of Coronavirus (BICS) survey. In their 7th May release, some of the data was been broken down to the Scotland level, which offers us crucial insights that we touch on in this article.

Data on household incomes come with an even greater lag, and hence the need to piece together different sources of information on how household finances are coping. Unfortunately, we still have no update Scotland level data on new Universal Credit claimants despite it being published at the UK level. Timely data on this has obvious value to policy makers in Scotland who are facing increased calls to help children in financial distress but unfortunately we now understand that will have to wait for the usually lagged monthly release in data. The next release for Scotland will be for data up till the 9th April whereas UK level data on new claimants currently includes data up to 5th May.

Business activity

The ONS Business Impact of Coronavirus (BICS) survey provides some timely indicators relating to business activity and it has now started to breakdown more of its data to Scotland.

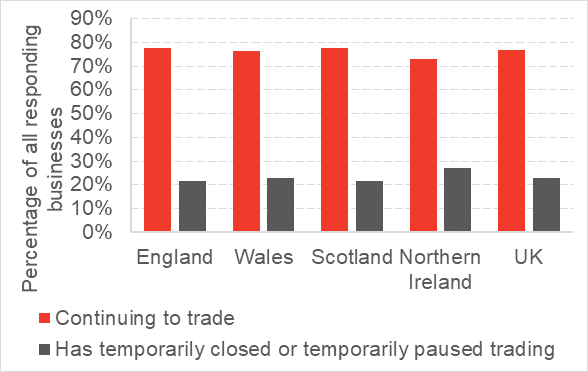

Due to the lockdown measures over 20% of all Scottish businesses have had to temporarily close or pause trading. This is a similar pattern to other parts of the UK too.

Chart 1: Current trading status of businesses in different parts of the UK (surveyed between 6th April and 19th April)

Source: ONS BICS

Chart 2: Change in turnover of Scottish businesses (surveyed between 6th and 19th April)

Source: ONS BICS

Almost 60% of Scottish businesses which continue to trade have seen a reduction in turnover. For almost a quarter of all Scottish businesses, the fall in turnover has been greater than 50% compared to the period prior to the lockdown.

The number of companies temporarily ceasing to trade, alongside the clear financial impact for those who are continuing to do so translates into uptake in government support schemes.

Chart 3: Percentage of Scottish businesses who have applied for government support initiatives (surveyed between 6th and 19th April)

Source: ONS BICS

The coronavirus job retention scheme and deferral of VAT payments are measures which have seen the highest take-up. Over 70% of companies have applied to the job retention scheme and over 60% have used the option of deferring VAT payments.

What is interesting is that all of these results are entirely consistent with the findings we collected at the start of April in our Scottish Business Monitor. Here businesses were telling us how much they expected their activity to be down (and by how much) and also what government schemes they would be applying for. That consistency suggests that future work to assess the expectations of businesses now will be crucial.

The Scottish Government started regularly publishing data relating to the Coronavirus Business Support Fund, a grant scheme linked to the business rates support system paying £10,000 to eligible smaller businesses and £25,000 to larger retail, hospitality and leisure businesses.

Chart 4: Coronavirus Business Support Fund – number and total value of grants awarded across local authorities as at 5th May 2020

Source: Scottish Government

The highest number of business support grants to date were given out to companies in Glasgow and Edinburgh, totalling circa £60m in each of the two cities (a marked reversal on initial teething troubles with reporting and responding in Glasgow). Despite a lower number of awards in Edinburgh compared to Glasgow, the grants have on average been higher for companies in Edinburgh, in all likelihood reflecting the larger number of businesses focused on hospitality and leisure in the capital.

Overall, we can see that a significant proportion of businesses have been relying on various forms of government support.

Consumer spending

There are several high-frequency indicators which can be used as a proxy for consumer spending. Data from Google trends on search volumes for specific products or services can be used as an indicator of consumer demand.

Searches for theatres fell 75% immediately after the lockdown measures were put in place and remained 54% lower compared to the same time last year at the start of May. Consumer interest in hotels also declined by 58% compared to last year. The contraction in demand in the automotive industry appears to have been sharp at the point when the lockdown was put in place but has recovered slightly over time. However, it has remained 36% lower at the start of May compared to last year.

Chart 5: Google searches for specific products and services in Scotland

Source: Google Trends

Note: For cars the reported value is the average of the search index for UK’s top 6 most sold car brands.

Labour market

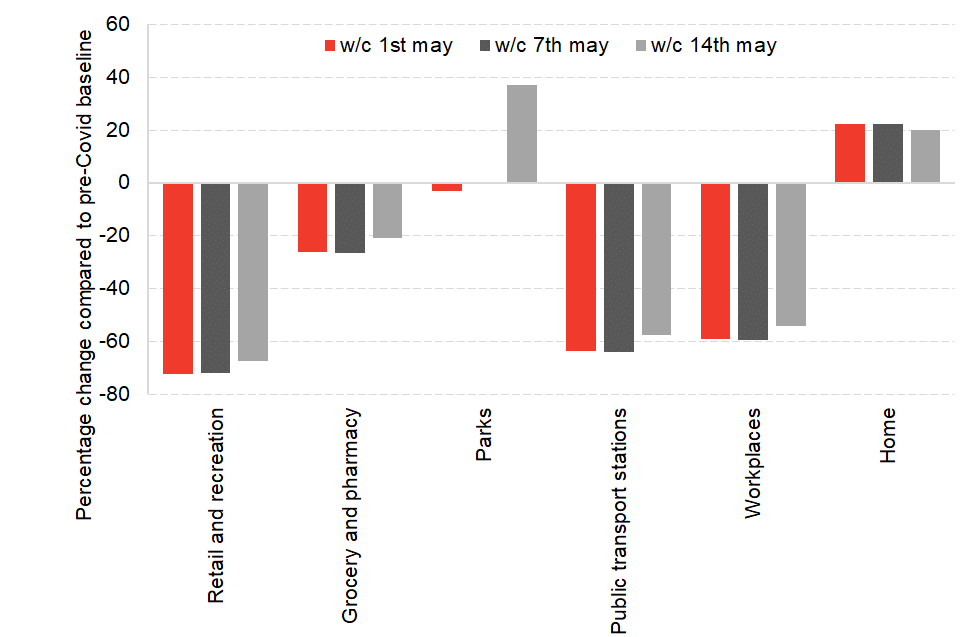

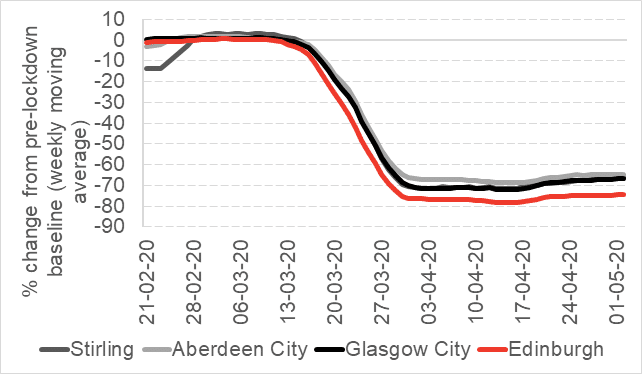

Labour market data is usually available with a significant lag and thus looking at indicators of mobility can provide a snapshot of how labour supply is developing. The ONS is due to release labour market data next week covering the period up until the end of March, which will start to provide a more comprehensive picture. More information on how the ONS will report changes in the labour market, for example the furlough scheme, can be found here.

Chart 6: Visits to workplaces in major Scottish cities

Source: Google Mobility Trends Report

Note: Pre-lockdown baseline is the median value for the corresponding day of the week during 3rd Jan – 6th Feb 2020)

The number of people commuting to work has not changed since we reported last week and remains way below the pre-lockdown average. This data will reflect that many people are now working from home but as well as the reduction in labour supply for sectors where work cannot be conducted from home.

Household Finances

Data on how many people claim different types of benefits are a useful indicator for how household finances are affected by the current crisis. DWP currently publishes estimates of the number of new claimants Universal Credit at the UK level, however as previously mentioned the data is not currently available at regional level at a high frequency.

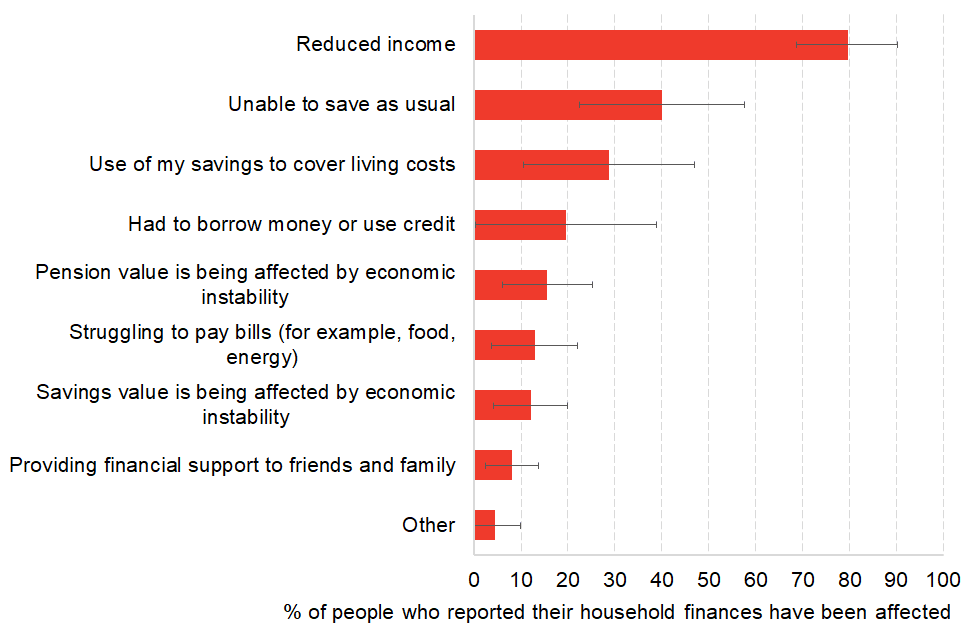

A recent survey for the Scottish Government has revealed that 41% of Scots believe the coronavirus crisis is already having a negative impact on their household finances. It also found that 48% of semi-skilled, unskilled, and casual workers have been negatively affected, whereas only 34% of those in managerial occupations have been affected. A negative effect has been reported by 46% of people with one or two children rising to 55% of people with three or more children.

Similar findings came from a survey by IPPR Scotland and the Standard Life Foundation. It found that 49% of households with dependent children in Scotland find themselves in the two most serious categories of financial stress. One in five households with dependent children in Scotland were in the most worrying financial circumstances – ‘in serious financial difficulty’ – compared to 12 per cent of all households in Scotland.

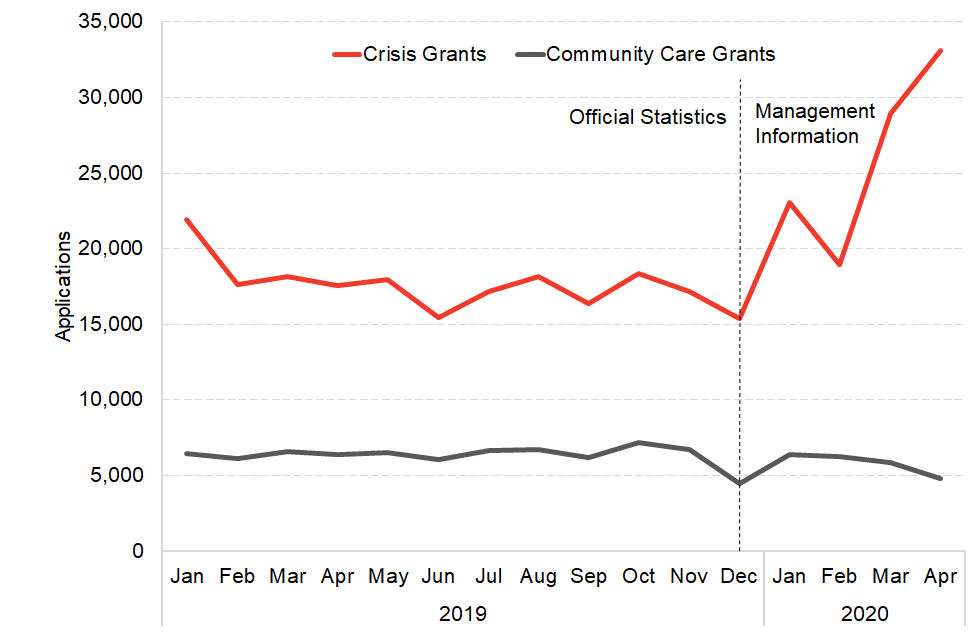

The Scottish Government recently published data relating to the Scottish Welfare Fund. This covers the period up to and including March 2020, so it captures some of the trends towards the start of the lockdown period. Crisis care grants provide support for low-income individuals facing a gap in their normal income because of a redundancy or change at work. It can also relate to other forms of unexpected crisis, such as a fire or flood or financial support with relocating due to domestic abuse.

Chart 7: Number of applications to the Scottish Welfare Fund

Source: Scottish Government

The number of applications for crisis grants rose by 60% in March compared to the same month last year. This indicates that households at the bottom of the income distribution started facing heightened financial insecurity and job losses immediately once the lockdown kicked-in. More money has been pumped into the Scottish Welfare fund although we don’t yet know how well the fund is able to meet demand.

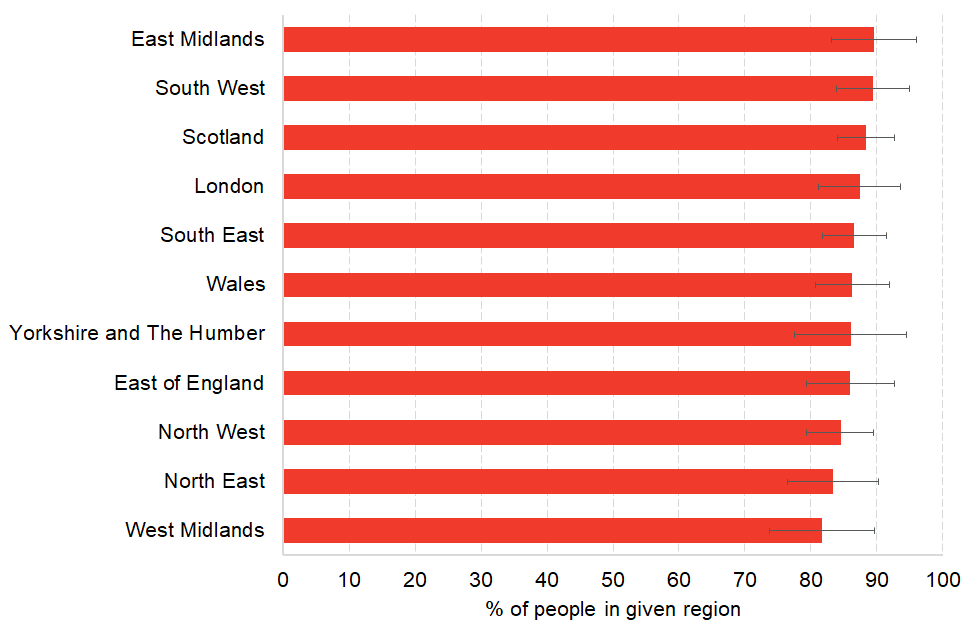

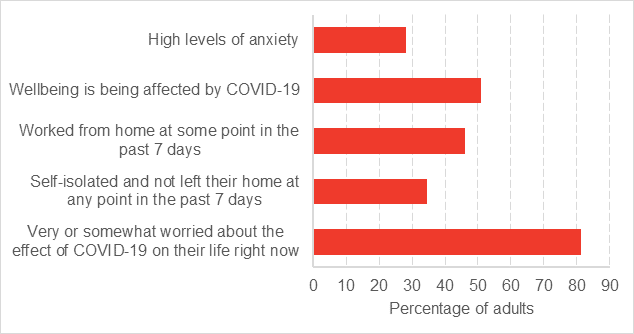

The lockdown can also have a significant impact on people’s mental and physical wellbeing. This can in turn lower the long-term productivity of the workforce and lead to a necessity of higher government spending on health and wellbeing in the future. The ONS started doing the Opinions and Lifestyle Survey (Covid-19 module) in order to shed more light on these aspects of life.

Chart 8: Headline indicators for social impacts of coronavirus in Scotland – Opinions and Lifestyle Survey (surveyed 17th to 27th April)

Source: ONS Opinions and Lifestyle Survey

The survey suggests that more than half of Scottish households’ wellbeing has already been negatively affected and over 80% are worried about the effect of coronavirus on their life. It further shows that only less than half of all surveyed people have been able to work from home.

Overview

These timely economic indicators show that the Coronavirus is having a profound impact on the Scottish economy. Government support schemes are seeing a large take-up and have allowed many companies to soften the blow and allow them to continue trading. With the imminent reopening of the economy, many businesses will slowly emerge from the crisis but until then the government’s support schemes are likely to come at a significant fiscal cost. This week’s announcement about an extension to the job retention scheme and only a gradual phasing out will hopefully help prevent further job losses but will come at a further increase in government debt.

Consumer demand and the labour market continue to operate at levels significantly below capacity and clear signs of a recovery are yet to be seen, which is to be expected given guidance in Scotland is yet to change.

The impact on household finances is troubling, and shows that despite the UK Government’s efforts, there are large amounts of people who are feeling financial distress. This is also having a toll on wellbeing and mental health. We are yet to see the impact of the Self-Employed Income Support Scheme and this could alleviate some of the stress for households eligible. However, there is likely to be long-lasting damage on many households’ financial situations, and these could get worse over time as businesses close. It therefore remains crucial to try and monitor these impacts as there are additional policy levers, both north and south of the border, that could be used to target support.

We will continue to monitor these indicators, and hopefully add more over the coming weeks.

Authors

The Fraser of Allander Institute (FAI) is a leading economy research institute based in the Department of Economics at the University of Strathclyde, Glasgow.