As the full lockdown in Scotland begins its third week, we are all getting used to the restrictions on social distancing, and, for those of us lucky enough to be working from home, new ways of working.

The focus of course remains as it should on the public health crisis. Large parts of the economy have been effectively mothballed in order to support that effort. Other parts have had to cope with significant restrictions placed on them.

A question we have been asked is to try to quantify the impact on the economy, both in the short term and in the long term.

We have avoided – and will continue to avoid – providing an exact forecast for what might happen to the economy over the next year or so. There is simply too much uncertainty around both the virus itself and the response of the economy.

What we will continue to do is to walk through the avenues through which the economy might be impacted, and to highlight the scale of the challenge.

In previous articles, we have discussed the possible long-term effects. In this blog, we discuss the possible scale of the short term hit to economic output in Scotland if the current restrictions were to continue for (say) a three-month period, in some form.

We do this through two channels:

- First, we look at the relative scale of different sectors in the Scottish economy to see how changes might impact upon the overall level of activity;

- Second, we draw on our emerging evidence and intelligence from businesses and other sources – including from our own forthcoming Scottish Business Monitor – to get a handle on the scale of the drop-off in demand we’re seeing reported.

This enables us to provide a high-level assessment of the impact of the current lock-down on day-to-day activity in Scotland. In this regard, it is important to focus upon the scale and direction of travel rather than any point estimate.

We estimate that if similar restrictions continue for a 3-month period, that Scottish GDP could contract by around 20-25%.

It is important to remember that this is NOT necessarily an exact prediction for growth in (say) Q2 2020.

This is both because (i) we do not yet know how long the restrictions will last and whether their nature will change (if the nature of the restrictions change, the impacts could be very different) and (ii) it is likely that large falls in output are spread over 2 quarters (both Q1 and Q2), given the restrictions began in March. Rather, it gives us a feel for the unprecedented nature of the likely impact on the economy.

How might the shutdown manifest in published GDP estimates?

To capture this, we need to first consider how short-term changes in activity are captured in the measurement of Scottish GDP. This effects how changes in output feed through to the estimates, from the first published estimates to how they may be revised in future.

An interesting (well, for National Accounts wonks!) source for this is the GDP sources catalogue. This is a useful spreadsheet, detailing all of the components of measurement of the Scottish volume and current price GDP statistics.

Interestingly, given some of the approaches used, the impact on growth in the short term might not be as severe as may be first thought given the way that GDP is calculated.

In particular, in many cases, short term movements in growth may be calculated by tracking changes in levels of employment (through measures such as workforce jobs). But it is not yet clear how furloughed staff will be treated (our first reading is that these staff will still be counted) and therefore the changes in jobs will not necessarily reflect that these staff are producing no output.

Of course, government statisticians may attempt to bypass this and introduce alternative estimates to come up with a more appropriate way of capturing the immediate and unprecedented hit to growth.

What we can conclude is that the first ‘estimate’ of the impact of the shutdown will be very much that, an estimate. Whilst revisions are part of producing national accounts, the current circumstances mean that normally reliable proxies for Scottish GDP may not do such a good job in capturing the real-world hit to the economy.

Agriculture

This sector makes up around 1.3% of the economy, and covers Agriculture, Forestry and Fishing (including aquaculture). The measurement of this sector relies on data that captures the physical volumes of production – fish landed, wood production, etc. Whilst there may be suppression in new forestry plantings, this is likely to be more than offset by increased demand for domestic agricultural products as import substitution takes place.

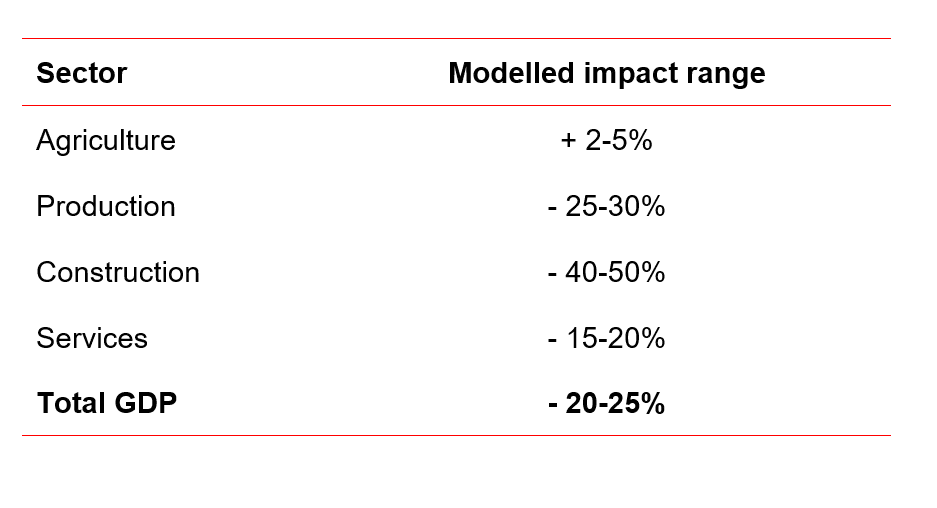

Overall, if the restrictions were to continue over a 3-month period, we estimate that this sector could actually see modest growth, of around 2-5%. However, it is important to remember that even a 5% growth in this sector will add less than +0.1 to overall Scottish GDP.

Production

The Production sector makes up 17% of the Scottish economy, the largest part of which is manufacturing, which makes up 11% of the Scottish economy.

Manufacturing

Manufacturing is made up of a number of detailed sectors:

- Food and Beverages (2.7%)

- Textiles (0.5%)

- Petroleum, Chemicals & Pharmaceutical products (1.5%)

- Metals & Machinery (1.6%)

- Computer & Electrical (0.8%)

- Transport Equipment (0.5%)

- Other manufacturing (2.8%) – which includes repair and maintenance.

These are measured through either:

- Physical production in tonnes

- Turnover from the ONS Monthly Business Survey (MBS)

Therefore, it is reasonable to assume that these measures will quickly capture changes in demand, both positive and negative. One thing to bear in mind though is that the MBS is a sample survey for smaller businesses, which can sometimes lead to volatility in the estimates.

There are of course sectors who are seeing increased demand, such as parts of food production. A suppression in demand for petroleum products (we’re hearing demand has fallen sharply, including supplies for the airline industry) is offset by demand for chemical and pharmaceutical production. In addition, we understand there is some import substitution for metal products.

So, it is very much a mixed picture for different parts of manufacturing.

Non-manufacturing production

In Scotland, this really covers three things:

- Mining and Quarrying (1.9%)

- Electricity & Gas Supply (3.3%)

- Water and Waste (1.4%)

First thing to remember is that Mining & Quarrying covers the onshore economy only. Therefore, apart from a very small amount of coal production, this is pretty much all Mining Support Services, i.e. onshore companies supporting our offshore industry.

As the vast majority of the UK Mining Support is in Scotland, the growth rate is taken from the UK series for this industry. It is likely that this will quickly pick up changes in turnover experienced by the sector. The feedback from the sector so far, especially given the collapse in the oil price, is that the impact has been severe.

Electricity and gas supply has seen a decline in demand of roughly 10% in the last few weeks, as reduced industrial demand more than offsets increased domestic demand as people stay at home. As this is measured by real-time consumption, again this is picked up quickly in the data.

Water and sewerage – measured by water supply – should see similar impacts to other utilities. In addition, it is clear that there is a suppression in demand for waste services, as recycling services have been restricted.

Taken together, and based upon the emerging evidence we are picking up so far, we estimate that 3-month restrictions could lead to a contraction in production of around 25-30 %.

Construction

The impact on construction continues to evolve, as more companies take the view that it is time to furlough staff and shut down operations. Construction accounts for around 6% of the economy.

This is measured using both the output in different sectors at the UK level and workforce jobs (WFJ). Falls in output in the UK data will be reflected therefore fairly quickly.

However, if the WFJ data doesn’t show any differential impact on Scottish employment (which is possible given the different advice in Scotland), then the true scope of the shutdown may not be fully felt in the first estimate of growth.

On balance, we’re seeing a shutdown in much of the housebuilding industry, and the mothballing of a large part of private construction infrastructure and repair. We assume that public infrastructure investment continues at its normal level (likely to be too optimistic, but this will also capture any additional demand for emergency construction work to escalate). We have used data from ONS’s publication Output in the Construction Industry, which shows the breakdown of different types of construction, to guide the scale of the impact on the sector.

Overall, if the restrictions were to continue over a 3-month period, and based upon the split of current activity, this would be pointing to a contraction in construction of as much as 40-50%.

Services

Services is by far the largest part of the Scottish economy, now accounting for 76% of output. It covers the following main sectors:

- Retail and wholesale (9.8%)

- Transport and Storage (4.4%)

- Accommodation and Food Services (3.3%)

- Information and Communication (3.5%)

- Financial and Insurance Services (6.8%)

- Real Estate Activities (12.4%)

- Professional, Scientific & Technical Services (6.3%)

- Administrative & Support Services (3.9%)

- Public Administration & Defence (6.5%)

- Education (5.7%)

- Health & Social Work (9.7%)

- Other Services (3.7%)

We’ll focus on the modelling we have done for a few of the sectors below: particularly where there are interesting measurement issues to consider.

Retail & Wholesale

Clearly, like manufacturing, it is a mixed picture for the retail and wholesale industry just now, with some sectors seeing increased demand, such as food retailers and online retailers, with others like traditional clothing retailers effectively in lockdown. The data used in GDP comes from the MBS again, so it is likely to pick up trends fairly quickly.

Overall, if the restrictions were to continue over a 3-month period, and given reports of footfall and our survey responses, we should not be surprised at seeing an overall contraction in retail, as the surge in online and food retail does not completely offset the mothballing of non-food retail.

Transport and Storage

This covers rail and road travel, air travel, support services for transport and warehousing and postal services.

Mostly, this is estimated using direct sources like passenger numbers or miles travelled, which are provided monthly or quarterly and therefore will pick up the complete sharp fall in demand for transport. However, this may well be offset in an increased demand for postal and courier services (which is measured through the MBS).

Overall, if the restrictions were to continue over a 3-month period, we think that our economy could be running at severely reduced capacity, pointing to a significant contraction in this sector.

Accommodation and Food Services

This has been one of the hardest and earliest hit sectors, with government first advising and then instructing bars, restaurants and hotels to close. With the instruction now clearly to avoid essential travel, accommodation providers across the country are seeing bookings being cancelled. Here we’re seeing businesses not just saying a reduction in demand but zero demand.

This again is measured through the MBS, and therefore should pick up trends quickly. However, this sector in particular suffers from the smaller sample coverage of smaller providers, so the statisticians will be working to find accurate ways of picking up the true scale of the shock.

Again, if the restrictions were to continue over a 3-month period, with the majority of the sector mothballed we estimate that there could be a very significant contraction in Accommodation and Food Services.

Real Estate

There has been a lot of coverage in the essential shut down of the property market just now, and one may expect that to have a big impact on this series.

It is true that the day-to-day operations of businesses in this sector will be severely impacted. But from a GDP perspective, the impact will be much smaller.

Why?

The majority of this is made up of what is called “imputed rent”, which as the name suggests, is an imputed payment which represents the value that owner-occupiers get from living in their homes. It is a modelled number using market rents, and is unlikely to move around much on a quarterly basis.

There is a series as part of this which reflects the activity associated with house selling, which we assume collapses during the shut-down period, but it is small compared to the series discussed above.

Overall, if the restrictions were to continue over a 3-month period, we estimate that there will be a contraction in Real Estate, but that it will be fairly modest compared to what one may expect.

The Public Sector

The sectors dominated by Government (Public Administration and Defence, Education and Health) collectively make up around 22% of the economy.

Some parts of the effect on this sector will be able to be picked up in quarterly data: so, for example, the surge in claimants for Universal Credit, and any public sector staffing increases to help cope with the crisis, are likely to be captured. However, others will be more difficult to see in the short term: the NHS is measured using a cost-weighted activity index estimated annually, so it is likely to be some time before increased activity is picked up.

In the short term though, we estimate that there could be a modest expansion in the Public Sector series.

Services overall

While we have not written about every sector in detail here, we have considered all sectors in the modelling. Like Production, Services is a mixed bag of sectors being mothballed and shut down and others seeing increased demand.

Taking everything together, and based upon the emerging evidence we are picking up so far, we estimate that there could be a contraction in services of around 15-20 %.

Overall impact

So what does all this mean? Bringing all this modelling together suggests that, if this sort of lock down were to continue for a 3-month period, we could expect to see around a 20-25% contraction in Scottish GDP.

Table: Summary of modelled impacts assuming lockdown restrictions for a 3-month period

Source: FAI calculations

Source: FAI calculations

It is important to emphasise again that these are not necessarily an exact prediction for growth in (say) Q2 2020 but simply an illustration of the scale of the ‘shock’ we are seeing to the economy.

What this shows us is:

- The scale of this shut down and therefore the impact are completely unprecedented;

- Whilst it is possible to use other assumptions about the possible scale of the ‘shock’ to individual businesses and sectors, any reasonable set of assumptions – given the size of the sectors being impacted – points to the impact being very large; and

- Production and Construction will be harder-hit than Services overall, although parts of retail, Accommodation and Food Services and transport are will be most severely impacted.

As we have discussed in other articles, these impacts will have quite different regional implications.

Now of course, many of these effects will be temporary. Once restrictions are gradually lifted, then we should see some of these sectors bouncing back. To what extent, we don’t yet know. As we pointed out here, it is likely to be a long-road to recovery.

Finally, we should all keep in mind how these effects will be captured in early measurement: it might be many months or even years before we actually know the full extent of the effect of the shut down on the Scottish economy.

Authors

Mairi is the Director of the Fraser of Allander Institute. Previously, she was the Deputy Chief Executive of the Scottish Fiscal Commission and the Head of National Accounts at the Scottish Government and has over a decade of experience working in different areas of statistics and analysis.

James is a Fellow at the Fraser of Allander Institute. He specialises in economic policy, modelling, trade and climate change. His work includes the production of economic statistics to improve our understanding of the economy, economic modelling and analysis to enhance the use of these statistics for policymaking, data visualisation to communicate results impactfully, and economic policy to understand how data can be used to drive decisions in Government.