At the end of the month, we will get new data on Scottish GDP. Recent statistics have been disappointing with the economy growing by just 0.8% in 2017.

One of the main drivers of the weak performance in 2017 was the sharp fall in construction output.

Digging into the data reveals that this is because infrastructure spending in Scotland fell by around 25% between 2015 and 2017. In this blog, we discuss the possible reasons behind this and the impact on Scotland’s headline growth estimates.

Construction in Scotland

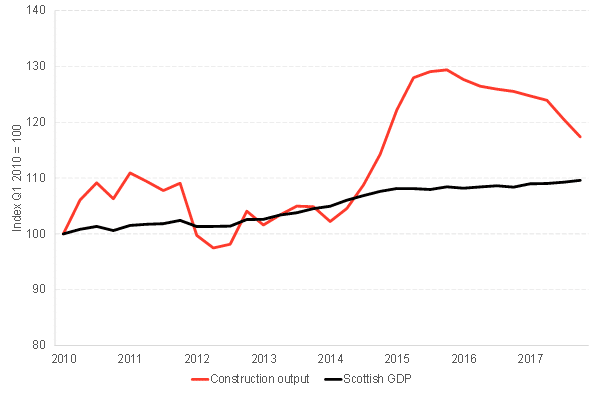

Construction sector output fell by around 6.5% during 2017 and is now nearly 10% below its 2015 peak. But as the chart highlights, all of this is on the back of a sharp spike in activity during 2014 and 2015 (where output rose 27%!).

Construction output and Scottish GDP since 2010

Source: Scottish Government/FAI

Such growth is unprecedented, even compared to the height of the construction boom prior to the financial crisis. As a result, much of the recent fall seems to be the series returning to more ‘normal’ levels.

The scale and pattern of these changes in construction have had a material impact on the headline GDP figures for Scotland.

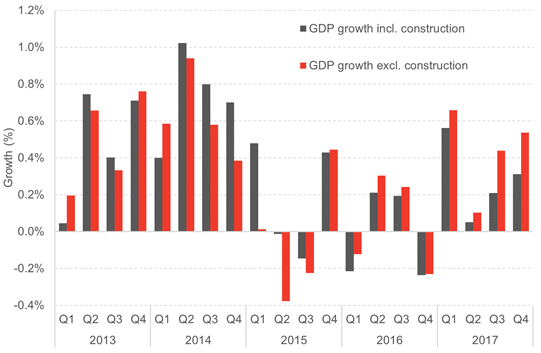

As the chart below highlights, removing construction from the headline growth figures leads to Scottish output being weaker in 2014 and 2015 than currently reported, but growth in 2016 and 2017 being that bit better.

Indeed, if we remove construction overall growth would have been 1.7% for 2017 as opposed to the 1.1% reported. To put this in context, UK growth in 2017 was 1.4%.

Scottish GDP with and without construction activity

Source: Scottish Government/FAI

What is driving the performance of construction?

The key source of information used by the Scottish Government to compile the construction data for GDP is the ONS’ Output in the Construction Industry series.

This dataset splits up construction output across the UK according to different classifications.

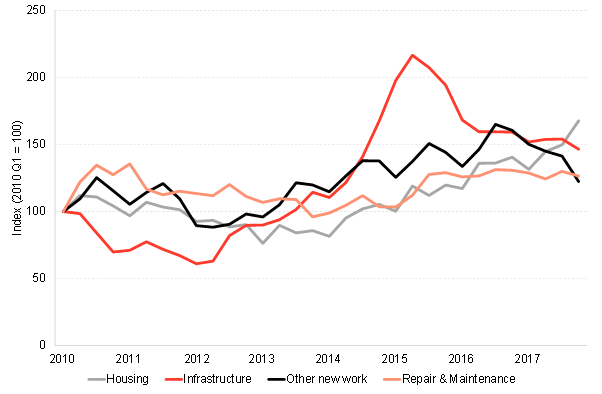

Components of output in the Scottish construction industry

Source: ONS/FAI

As the chart highlights, the key standout is the performance of infrastructure (although other new work – driven by the public sector element has also been falling sharply in 2017).

Apparently, infrastructure in Scotland grew by over 35% in 2014, a further 50% in 2015 before falling back again by over 20% in 2016 and 6% in 2017.

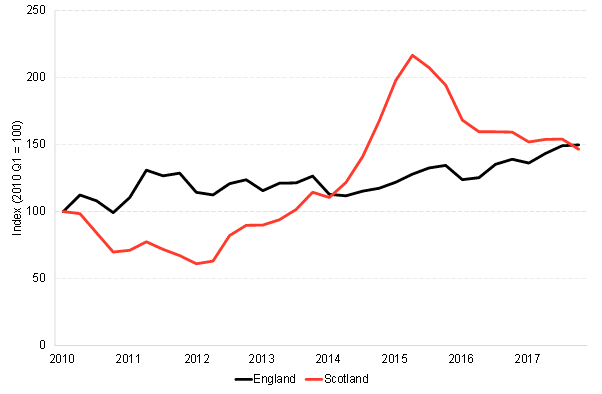

This pattern of activity seems peculiar. For comparison, the chart below shows the equivalent performance of infrastructure in England.

Infrastructure activity – Scotland and England

Source: ONS/FAI

What is the explanation for this?

The ONS doesn’t provide a breakdown of how much infrastructure spending in Scotland is public vs. private. For GB as a whole, the ratio is around 40:60 (i.e. 40% is believed to be public infrastructure).

We know of one major private infrastructure project which will have impacted on the figures for Scotland – in 2016, a new gas plant was opened in Shetland worth an estimated £800 million.

The Scottish Government has argued that one alternative explanation could be the recent completion of a number of major infrastructure projects – e.g. the Forth Replacement Crossing, the M8 completion etc.

Whilst this is undoubtedly the case, it only tells part of the story. Whilst a number of iconic public infrastructure projects have been delivered over the last 12 to 18 months, the actual amount of money available to the Scottish Government for spending on infrastructure has been rising.

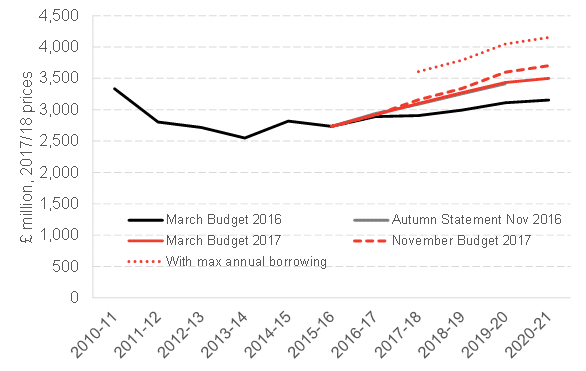

Scottish Government capital spending

Source: FAI

So what might explain this peculiar behaviour of construction – and in particular infrastructure?

Firstly, it is entirely possible that the methodology used by ONS to allocate construction activity to Scotland is not fully capturing activity on the ground.

Their approach is to allocate activity across the UK by the location of the building site for new orders and by company address for repair and maintenance. In turn, the new orders are then distributed over time using a series of generic lag distributions. For example, the value of an infrastructure ‘new order’ is spread over 11 quarters (with the majority of activity allocated to around 1 year after the order was signed).

Whilst an ok methodology for ‘normal’ times, it might not be perfect 100% of the time. It is at least possible, that major projects like the Forth Replacement Crossing or other complex revenue funded models could be skewing the series for Scotland. The ONS are currently improving their methodology, with new data to be released this month.

Secondly, aside from a methodological issue, it is also possible that the data could be reflecting ‘real’ activity in Scotland.

As highlighted above, the Scottish Government’s traditional capital budget is on the rise. And local government capital spending has also been increasing.

But back in 2015, a ruling by the ONS classified a high-profile NPD project – the Aberdeen Western Periphery Route – as ‘public sector’ meaning that for accounting purposes the project (and similar ones like it) had now to be treated as being on balance sheet. The additionality provided by NPD, over and above traditional capital spending, was lost.

In the end, an accounting adjustment agreed with HM Treasury, meant that committed projects could still go ahead but the Scottish Government would have to use up its new borrowing powers to pay for them. Any new projects would have to be met from traditional capital budgets, resource transfers or additional borrowing.

How much of an impact might this have?

It’s hard to put an exact figure on this. In part, because the Scottish Government no longer publish information – as they used to do in their Draft Budgets – on the total amount of infrastructure spending in a given year by RAB enhancements, capital DEL, borrowing, capital receipts and NPD.

What we can be confident of is that the total amount of infrastructure spending planned to be undertaken by the Scottish Government must necessarily have been lower – and future growth will not be as great – relative to what they had hoped to spend given the loss of additionality.

Summary

The behaviour of the construction series has had a material impact on Scottish growth over the last 2 to 3 years.

Stripping out construction, we find that the Scottish economy was in a healthier position in 2017 than would seem at first glance.

Explaining why the construction series has displayed such odd characteristics is not straightforward.

Some of it might be methodological which, if this is the case, might be resolved with the change in approach to be taken by the ONS.

But some of it could be the legacy effects of the ONS’ decision to re-classify NPD projects as being ‘on-balance’ sheet. If this is indeed the case, and it has contributed to an overall weakening in the Scottish economy, it will only add to the debate about the role of off-balance sheet infrastructure investment, its costs, and its contribution to supporting growth when the economy is fragile.

Authors

The Fraser of Allander Institute (FAI) is a leading economy research institute based in the Department of Economics at the University of Strathclyde, Glasgow.