Today – in partnership with Deloitte – we published our latest Economic Commentary.

This blog summarises the contents and key message of the report.

Alongside the usual commentary on the Scottish economy there are some interesting articles from:

- David Eiser on the links between economic growth and income tax revenues;

- Grant Allan on what the latest FAI/AGCC oil and gas survey is telling us about the transition to low carbon energy systems in Scotland;

- Jennifer Turnbull and Kenny Richmond on Scotland’s recent innovation performance; and,

- A look by Viktoria Bachtler at Scotland’s recent performance in terms of high growth companies.

Here we summarise some of the key conclusions from our outlook section.

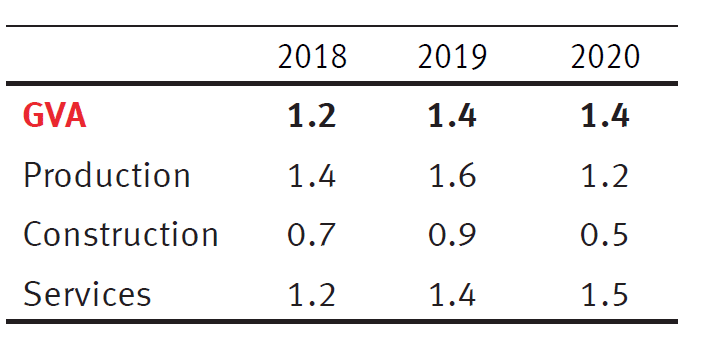

1. In the light of recent economic data, and a weaker outlook for productivity at the UK level going forward, we have slightly revised down our forecasts for 2018 and 2019 compared to our September forecast.

FAI forecast Scottish GVA growth (%) by sector 2018 to 2020

Our overall assessment is broadly unchanged, however. We believe that the Scottish economy will grow next year and the year after, but predict that such growth will remain below trend.

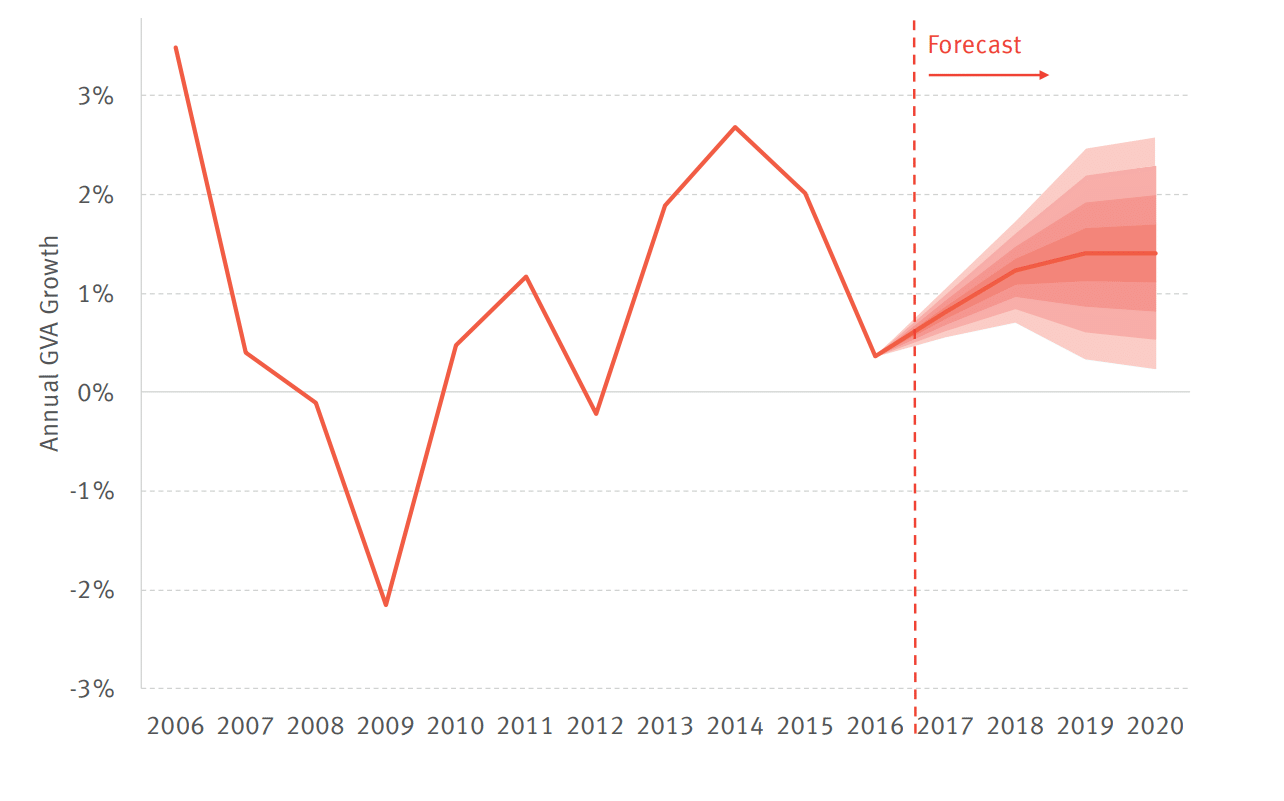

In these uncertain times, we recommend that just as much attention is given to the range of estimates that underpin this outlook as well as to our central estimates.

FAI Scottish GVA forecast range 2018 to 2020

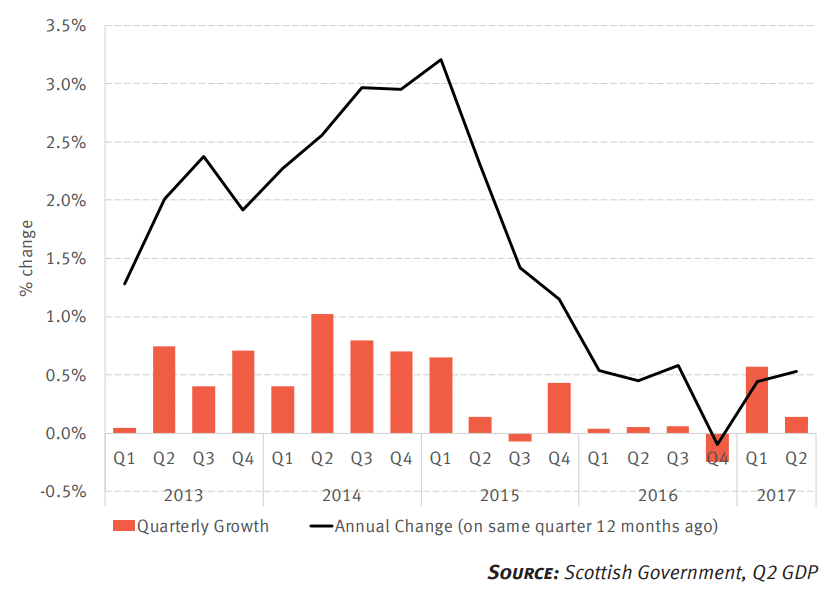

2. The Scottish economy grew by 0.1% in the second quarter of 2017. Annual growth has risen to 0.5%, but is still well below trend and a third of the rate in the UK.

Scottish GDP growth (quarterly and annual) since 2013

In five of the past six quarters, Scottish growth has been 0.1% or lower.

The poor performance in this most recent quarter was driven by a further sharp fall in construction output and some back sliding on the gains made in manufacturing during Q1 (when there was strong growth in a number of small and often volatile sectors).

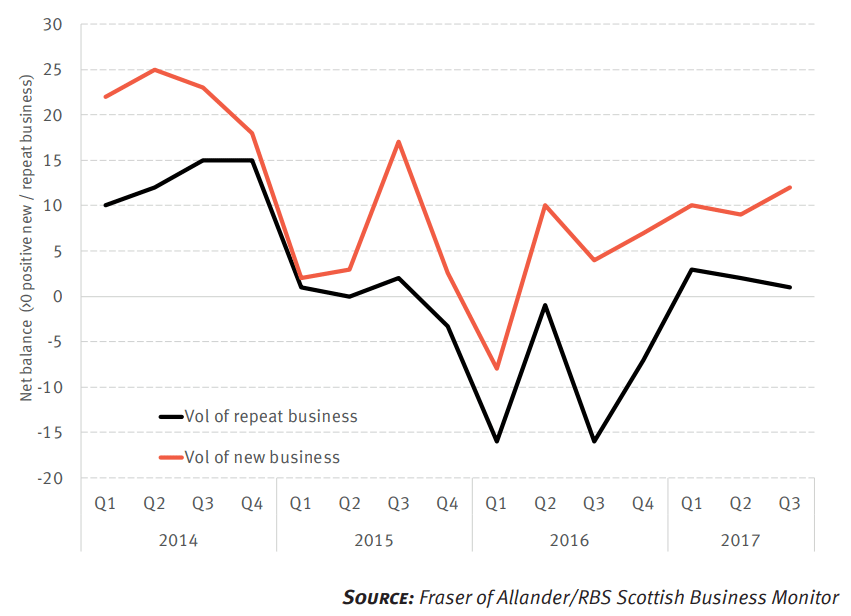

3. Our latest nowcasts predict growth of 0.4% in Q3 and Q4. So growth appears to be continuing – and arguably building some modest momentum.

A similar story emerges when looking at the latest business surveys for Scotland. Our latest FAI/RBS Scottish Business Monitor for example predicts increase repeat and new business, although indicators remain low by historical standards.

FAI/RBS Scottish Business Monitor for Q3 2017

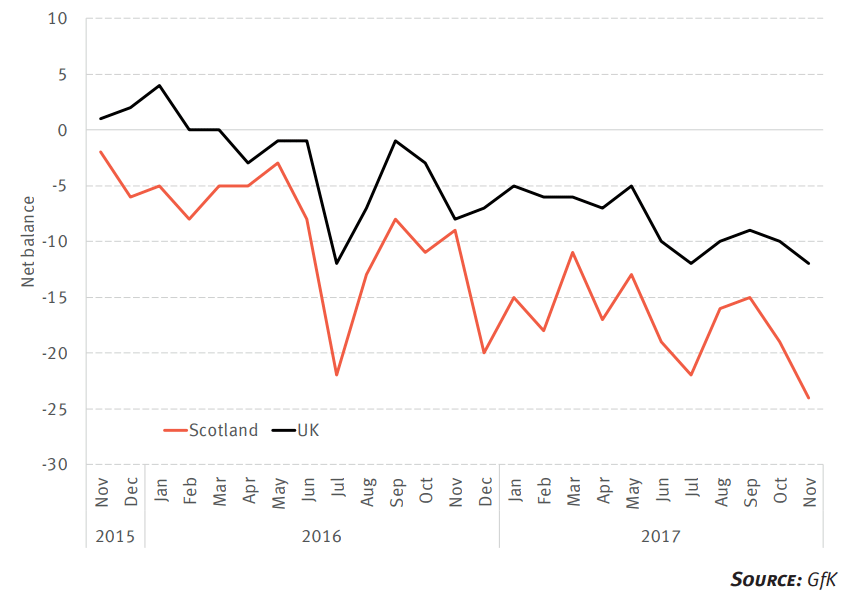

In contrast, indicators of consumer confidence remain much more negative – with Scotland lagging the UK as a whole.

GfK Consumer confidence indicator for Scotland and the UK (<0 = balance of households are pessimistic about the outlook)

The Commentary also shows how households at the lower end of the income distribution appear to be the least confident about the future than better off households.

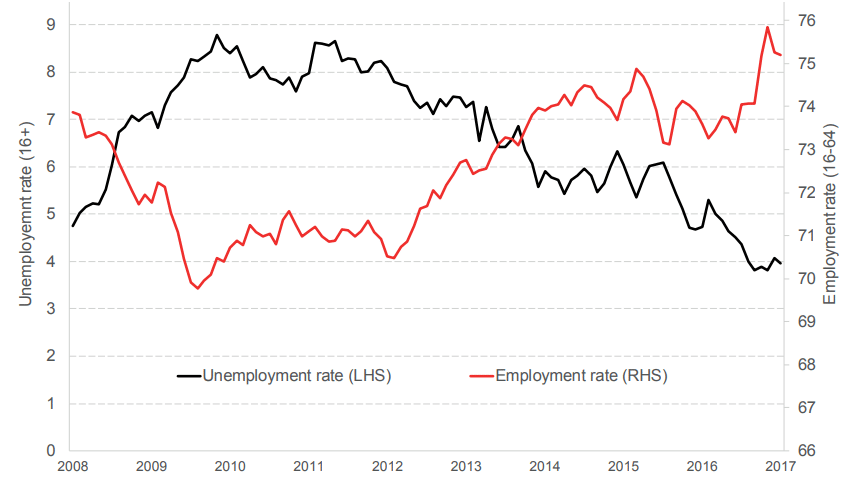

4. Despite the challenges in the overall economy, the Scottish labour market continues to hold up remarkably well.

Both Scotland’s employment and unemployment rates are close to the best ever recorded since the Labour Force Survey was first collected in 1992.

Scottish employment and unemployment since 2008

Over the year to September, employment has increased by 46,000. At the same time, unemployment has fallen by around 20,000.

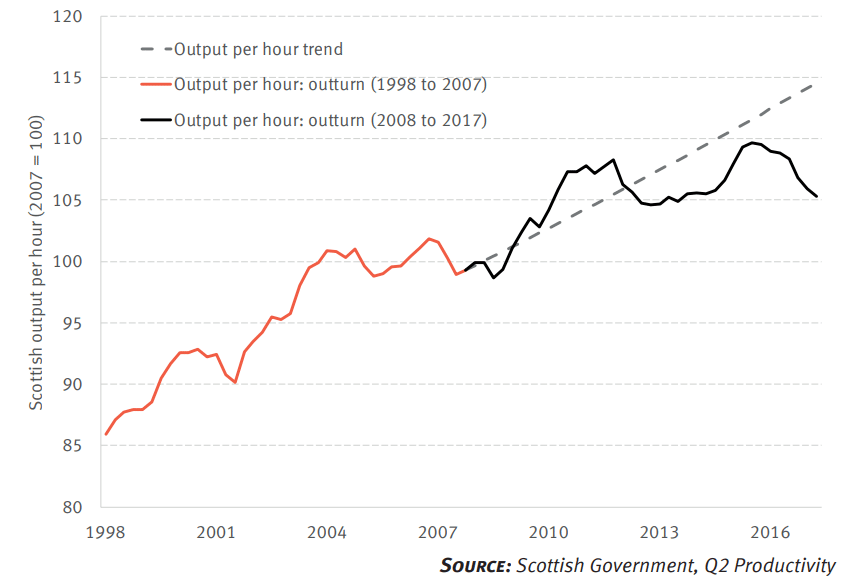

5. However only focussing on headline labour market indicators misses a wider understanding about how the economy is performing.

With limited growth in the economy, Scottish productivity has slipped. Output per hour – the key measure of labour productivity – is down by around 4% since 2015 moving it further away from trend.

Scottish productivity (output per hour) and trend since 1998

Weak productivity is the key reason why – although near record numbers of people are in work – the earnings that they are receiving continue to fall in real terms.

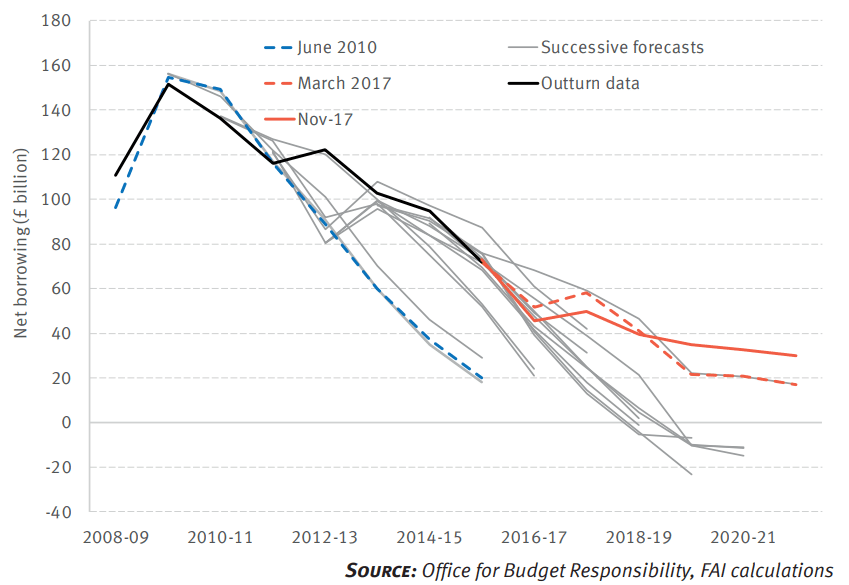

6. This weak productivity performance is not just limited to Scotland. The Office for Budget Responsibility are now much more pessimistic about the outlook for productivity at the UK level.

Productivity is not just crucial for earnings, it is also vitally important for tax revenues.

As a result, they have revised up – once again – their forecasts for UK public sector net borrowing over the next few years.

UK public sector net borrowing – outturn and forecast since 2008-09

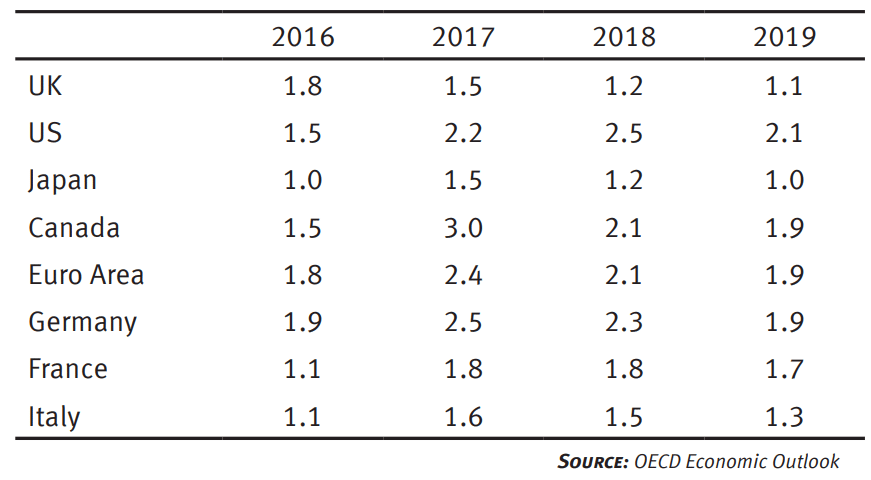

7. Whilst the outlook for the UK has become more gloomy, the global economy continues to power ahead.

Forecasts for G7 growth

Global growth is projected to be over 3.5% this year, rising to 3.75% in 2018 – the fastest rate since 2010. A robust global economy, particularly in emerging markets, provides an opportunity for firms to move into new markets and attract new consumers.

8. In the policy section of the commentary we discuss how the economic context will shape – and be shaped – by Thursday’s budget. Alongside the Scottish Budget, the newly independent Scottish Fiscal Commission will publish their forecasts for the coming years. This time last year the Scottish Government were predicted a steady return to 2% growth by 2021-22.

Scottish Government’s forecasts for GDP – Budget December 2016

It will be interesting to see the extent to which the Fiscal Commission will revise this outlook.

Authors

The Fraser of Allander Institute (FAI) is a leading economy research institute based in the Department of Economics at the University of Strathclyde, Glasgow.