Today we published our latest Fraser of Allander Economic Commentary.

Here we summarise some of our key conclusions.

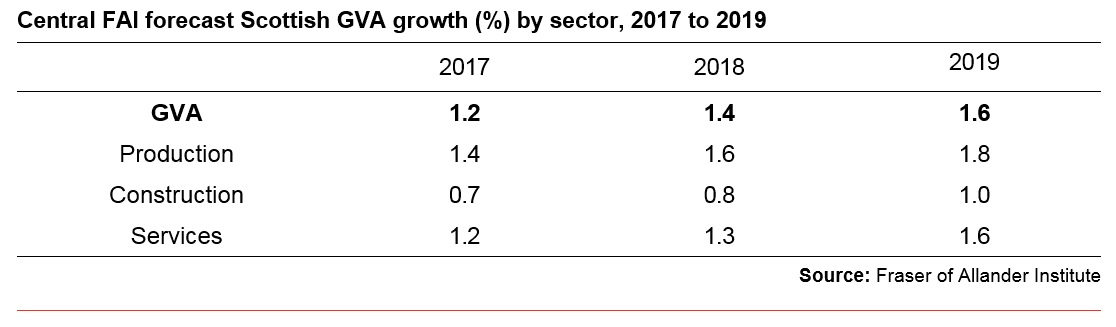

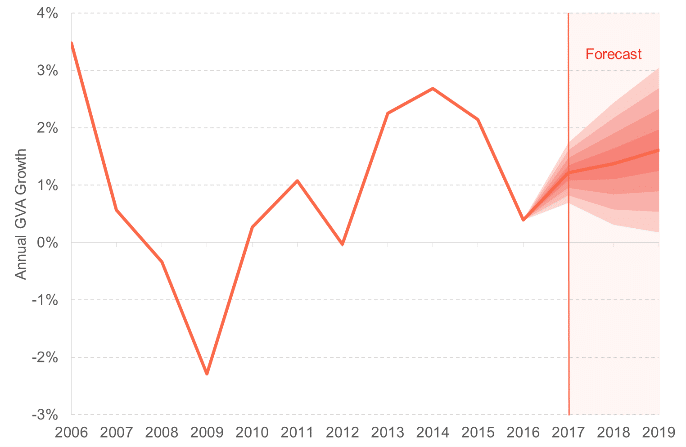

1. Overall, we expect growth in Scotland’s economy to pick-up over the next three years but to remain below trend. As we argued back in July last year, quarterly growth is likely to be quite volatile with further negative figures entirely possible. But on the whole, the latest indicators of activity suggest that there will be more growth in the economy than there has been over the past 12 months.

Central FAI forecast Scottish GVA growth (%) by sector, 2017 to 20190

In such uncertain times, we continue to recommend that just as much attention is given to the range of estimates that underpin this outlook as well as our central estimates.

Source: Fraser of Allander Institute

Some sectors stand to do quite well – particularly those such as food & drink and tourism who will continue to benefit from the low value of the pound. Others, particularly those that rely on household spending, such as retail, are likely to face tougher trading conditions.

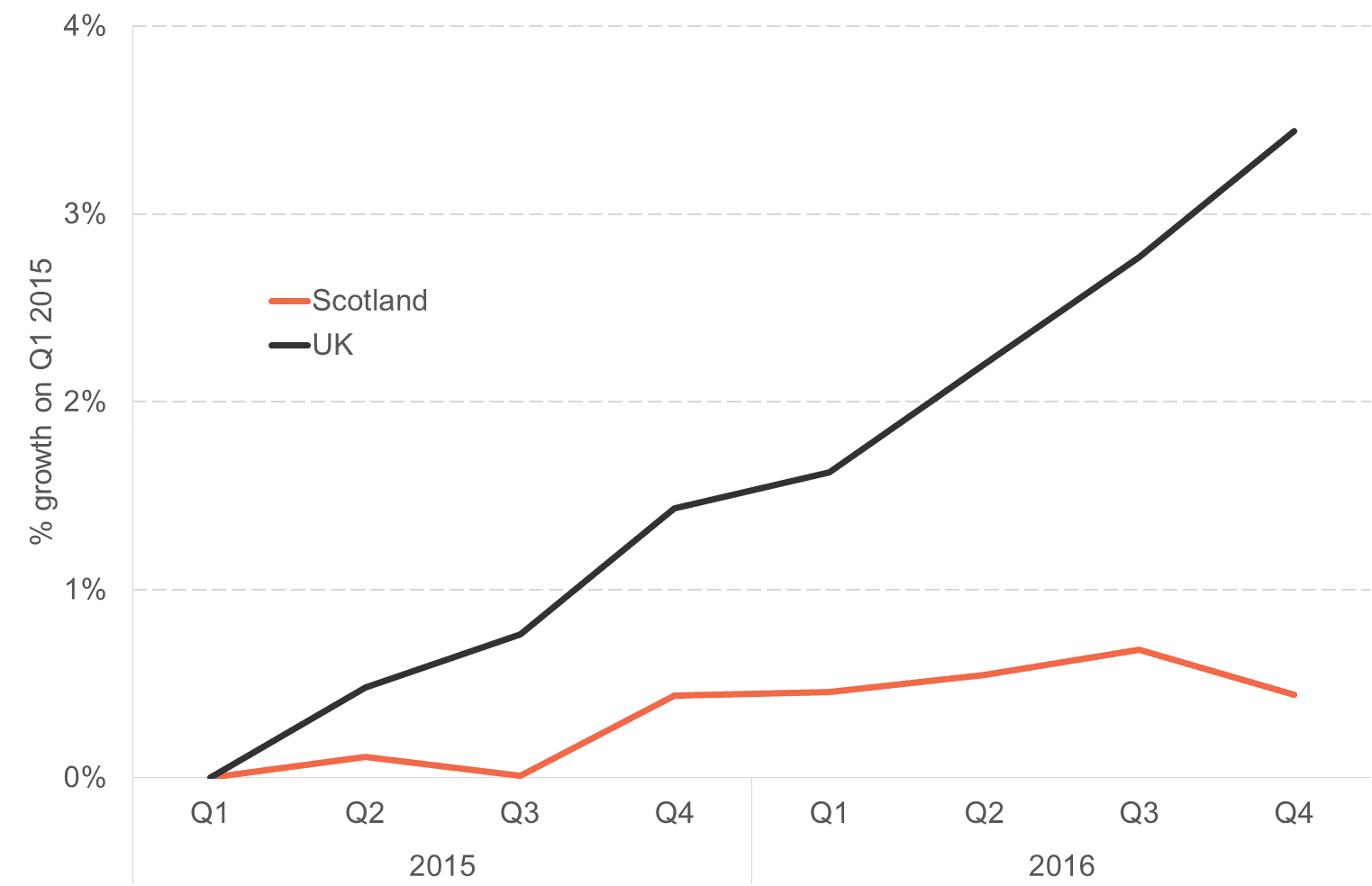

2. The latest economic data has – on the whole – continued to be relatively disappointing. Scotland’s economy shrank in the final three months of 2016, with the slowdown evident across most key sectors.

Whether or not next week’s data confirms a ‘technical’ recession (defined by economists as two consecutive quarters of falling output) is in our view not especially important. On balance, we think that the figure will be positive. But of much greater importance is the longer-term time trend and the gap that has opened up between Scotland and the UK. With Holyrood’s Budget now dependent upon how Scotland’s economy performs relative to the UK as a whole, it is now even more crucial that this gap is closed.

Scottish & UK cumulative growth – since 2015

Source: Scottish Government, Q4 GDP

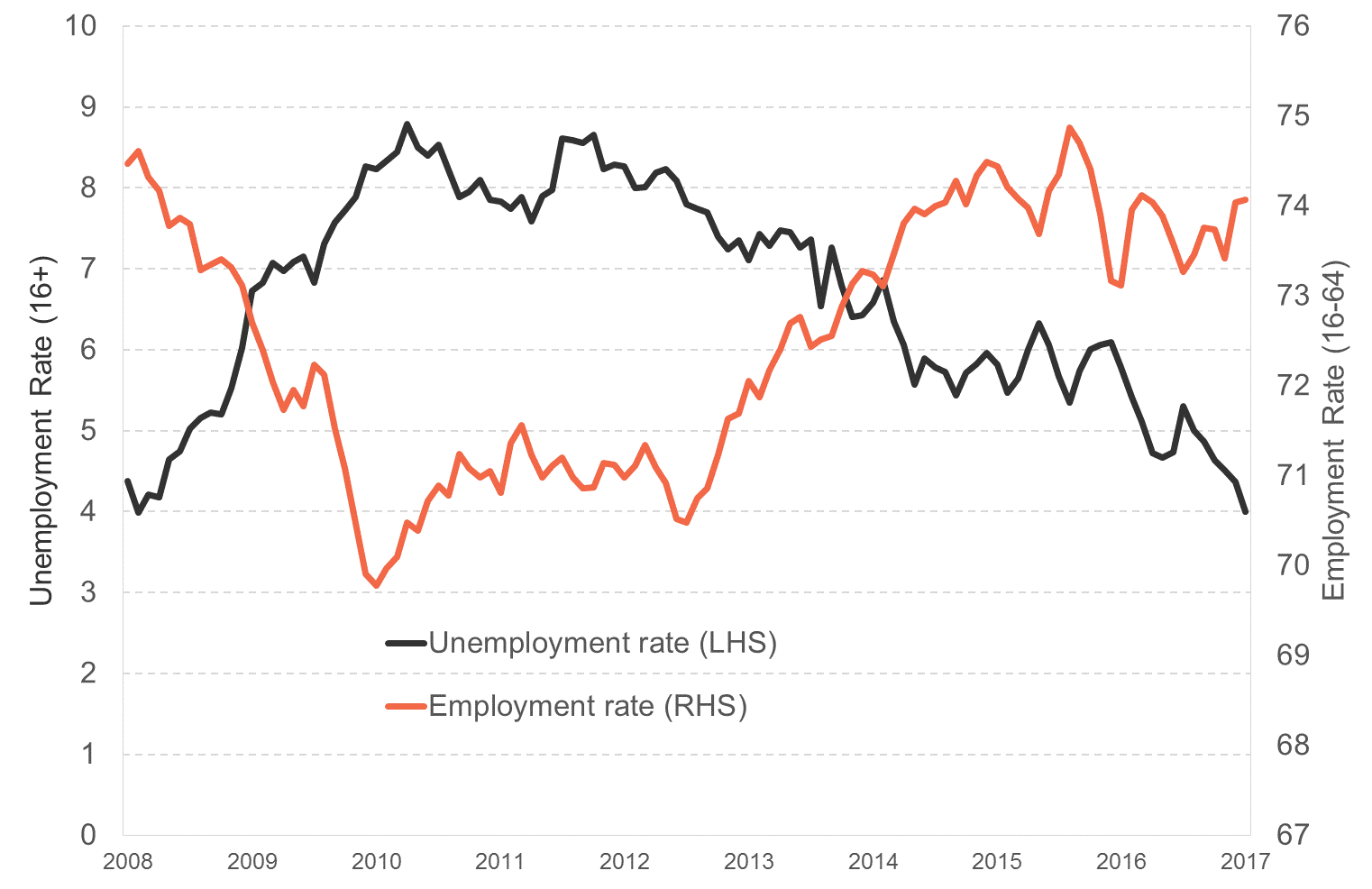

3. The one bright spot has been the labour market, as our recent Scottish Labour Market Trends report highlighted, where unemployment is now at a record low.

Underemployment has continued to fall, whilst Scotland has better labour market outcomes for 16-24 year olds. The Government are right to point this out and that this is better than we forecast last year.

Scottish employment & unemployment rate

Source: ONS, Labour Force Survey

But we continue to urge caution when interpreting the recent labour market data.

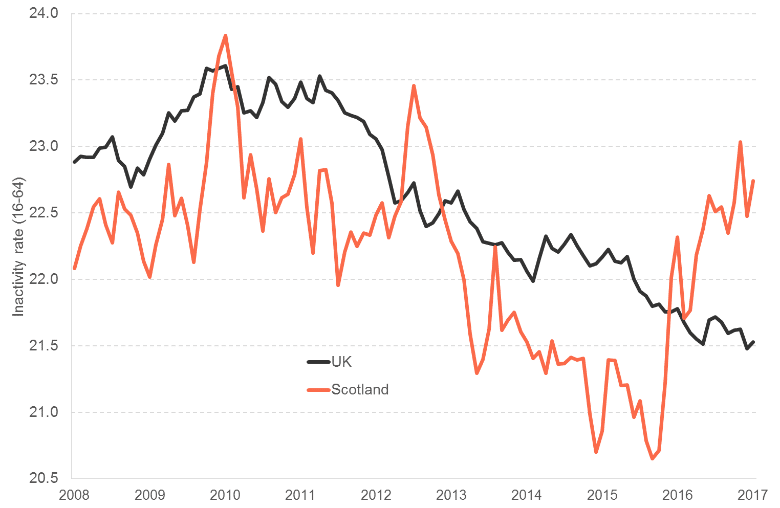

Firstly, some of the fall in unemployment in recent years has been driven, not by people finding work but, by people leaving the labour market entirely – that is moving into inactivity. If these people had continued to search for a job, then the unemployment rate would be higher.

Scottish & UK inactivity rates since 2008

Source: ONS, Labour Force Survey and FAI calculations

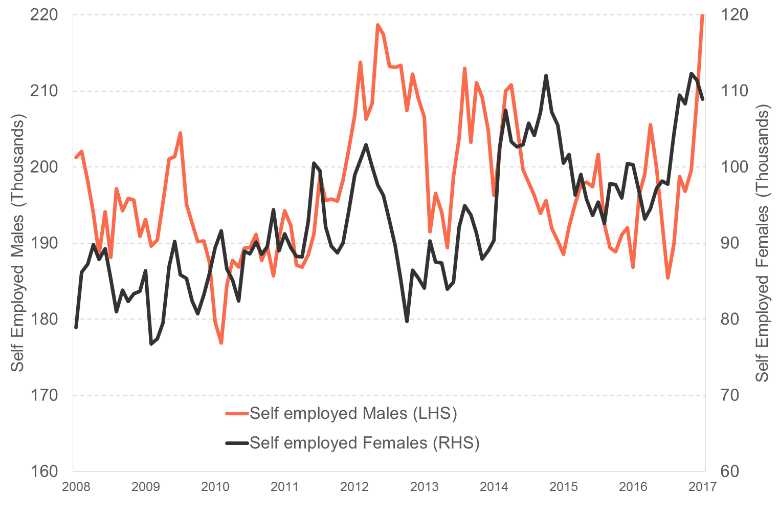

Secondly, almost all of the improvement in the employment figures has been in the form of self-employment. A concern that exists about this increase is that whilst, for some, the greater flexibility that self-employment brings is welcome, for others, it may come with less stable and rewarding opportunities and fewer protections.

Sharp rise in self-employment in Scotland

Source: ONS, Labour Force Survey

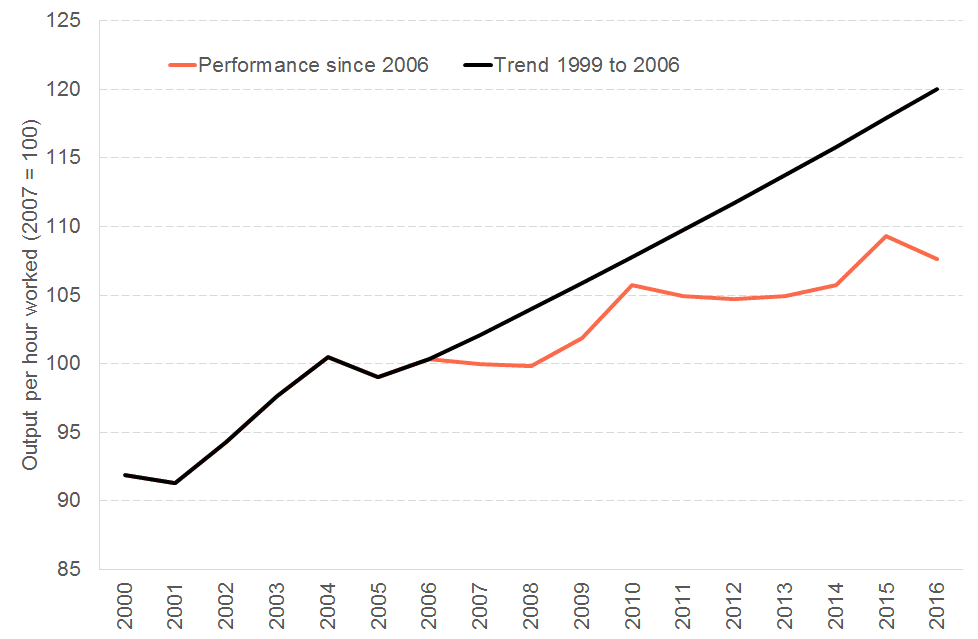

Finally, and much more importantly, with little growth in output and rising employment, this means that we’re producing less but with more people. In other words, productivity growth will continue to be poor. This explains, in part, why whilst employment has been growing, wages and earnings have seen very little in the way of real-terms growth.

Scotland’s productivity growth since 2006

Source: Scottish Government & FAI calculations

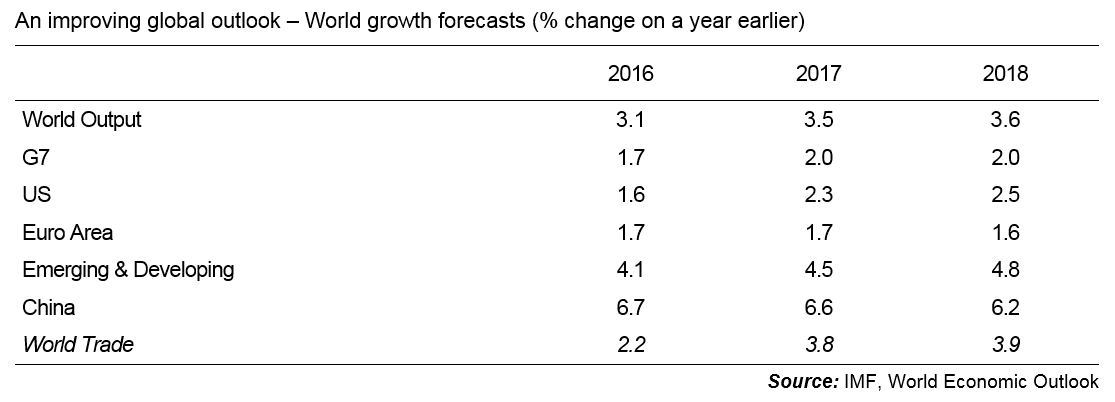

4. Global forecasts have improved in recent times – and this should help support Scottish exporters.

An improving global outlook – World growth forecasts (% change on a year earlier)

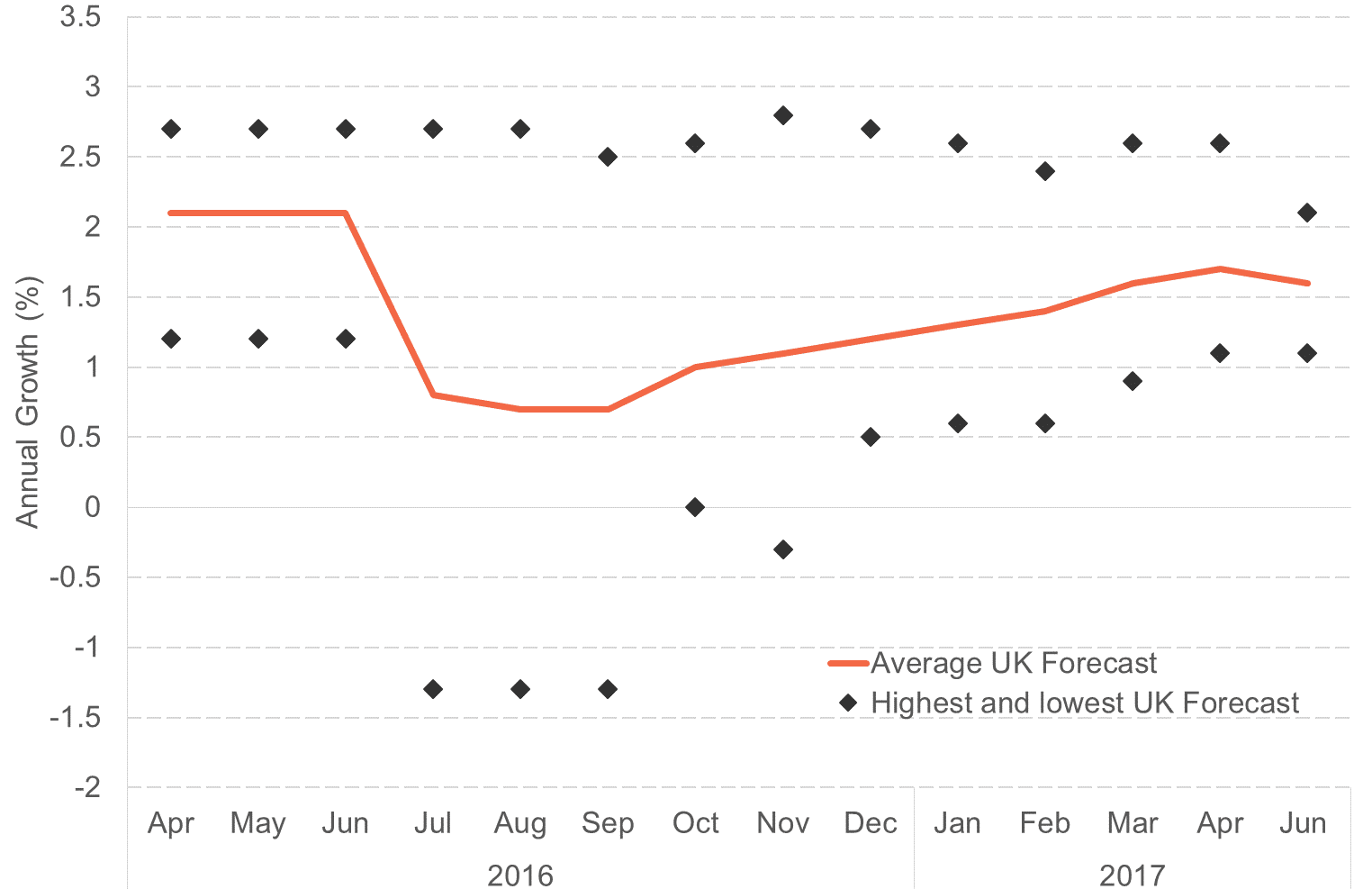

And overall, the outlook for the UK is better than most economists thought this time last year…

Evolution of UK forecasts for 2017

Source: HM Treasury

…but the effects of Brexit are expected to have an increasingly significant impact over the coming years, with most still predicting that growth –while positive- will slow down over the next few years.

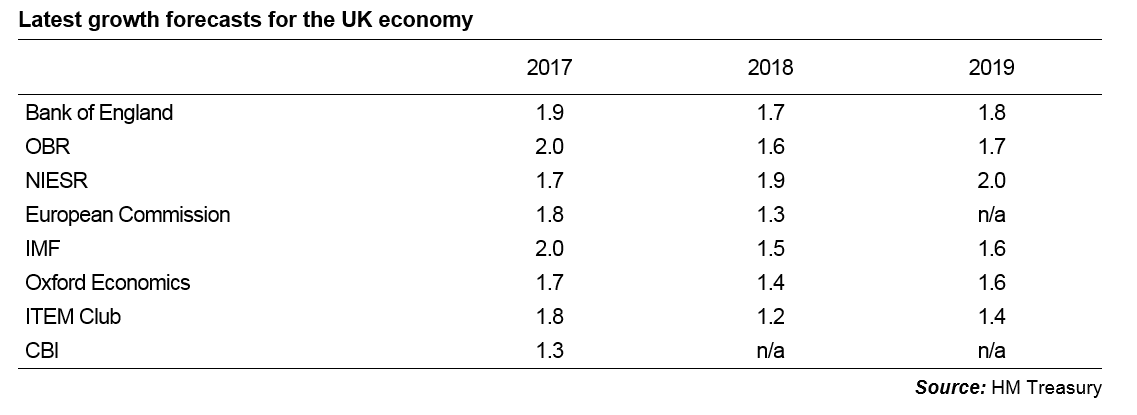

Latest growth forecasts for the UK economy

5. So what explains the gap between Scotland and the UK?

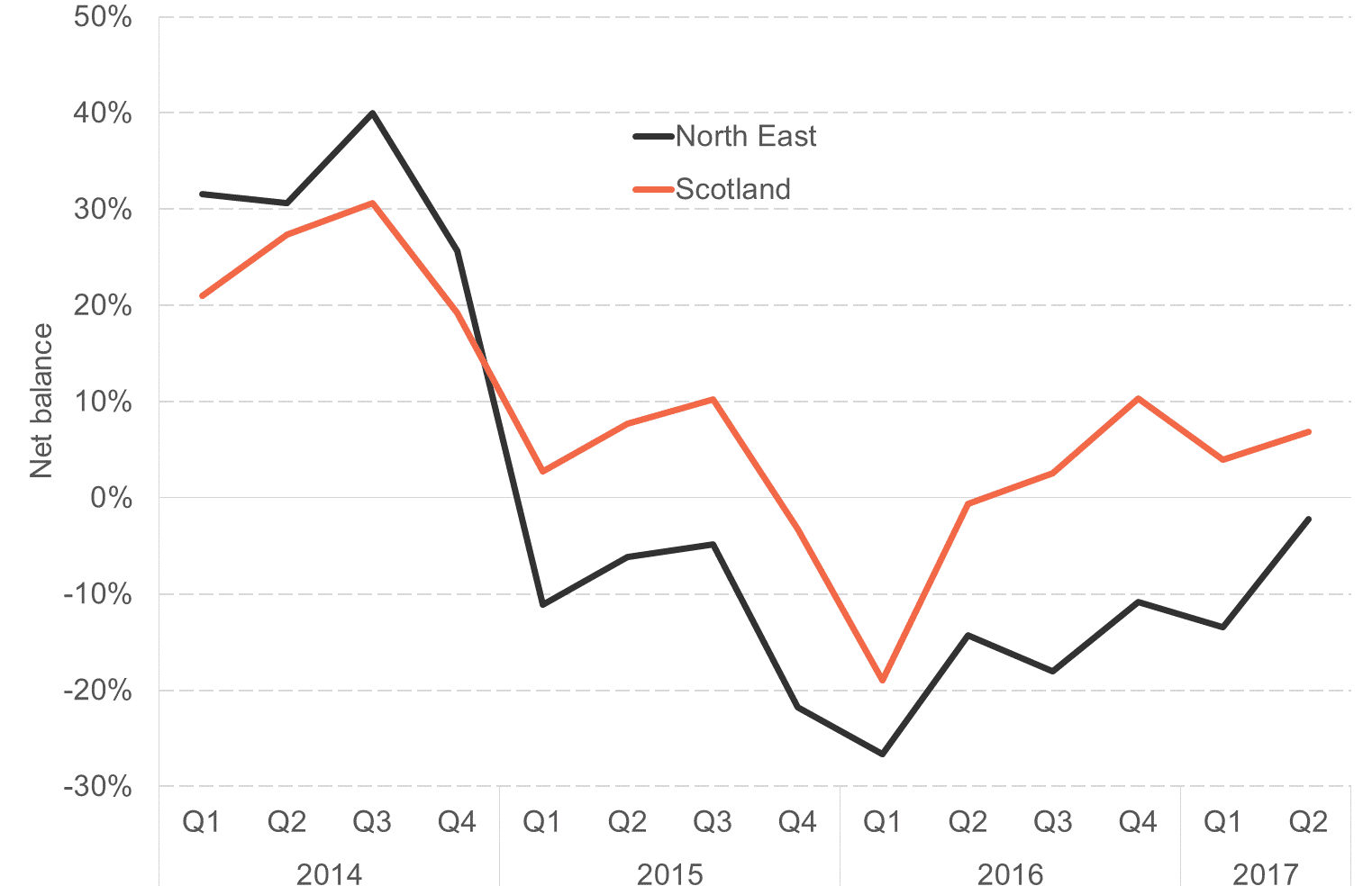

The downturn in the oil and gas industry clearly continues to have an impact.

Business activity in the north east – as a result of downturn in oil and gas – lagging behind Scotland

Source: RBS/FAI Scottish Business Monitor

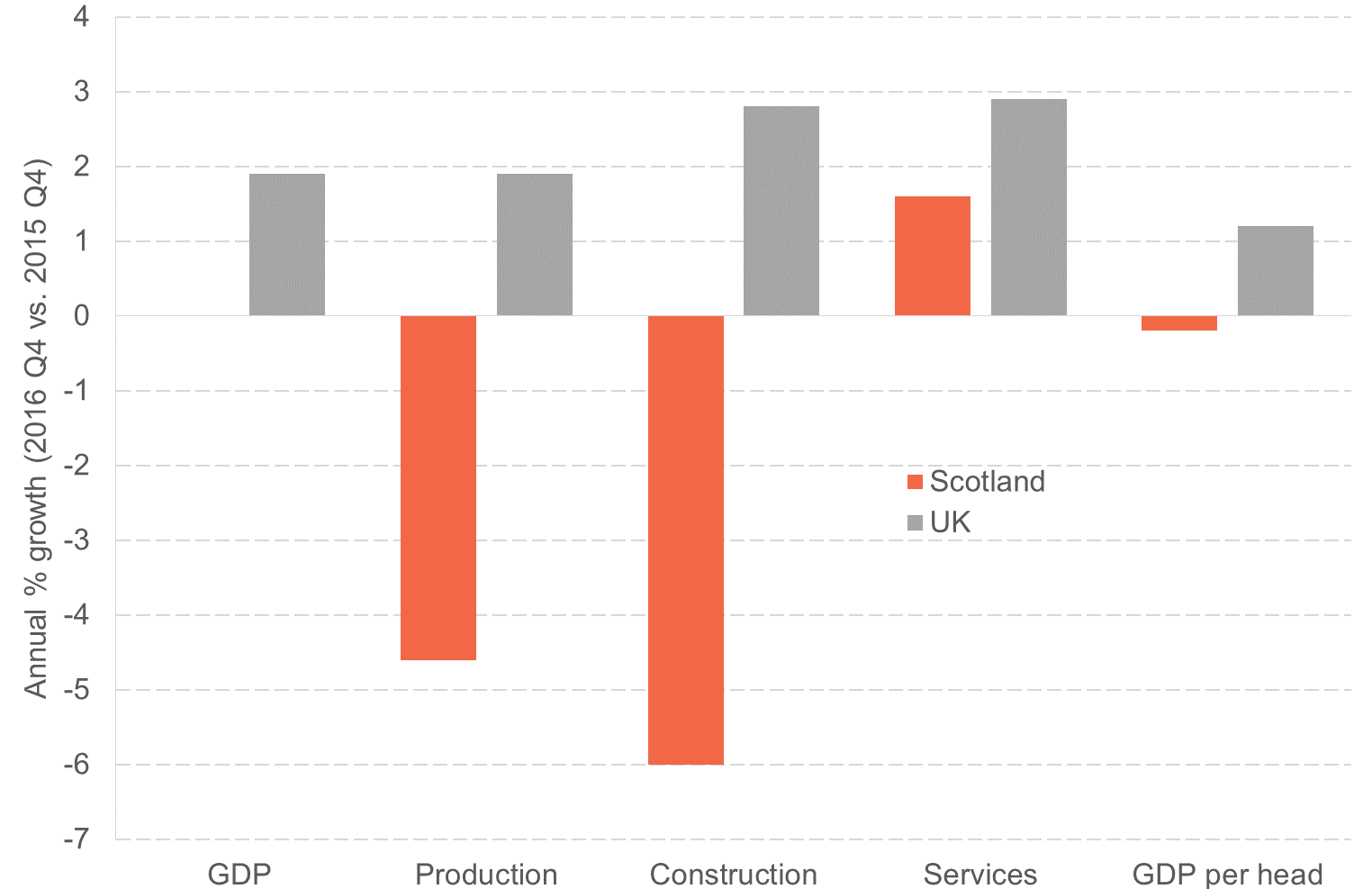

But the recent challenges appear to no longer be just limited to sectors tied to oil and gas. Construction has continued to fall, whilst services are growing at just over ½ the UK rate.

Weakness across sectors evident over the year in the Scottish economy

Source: Scottish Government, Q4 GDP

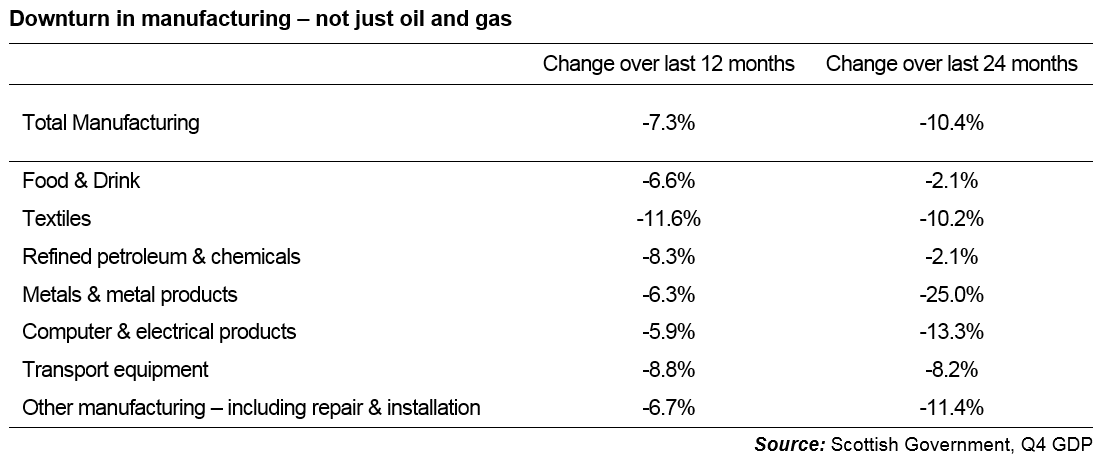

This is particularly evident in manufacturing, where sectors linked to the North Sea such as metals and metal products have clearly been badly impacted, but others such as Food and Drink and textiles have also weakened.

Downturn in manufacturing – not just oil and gas

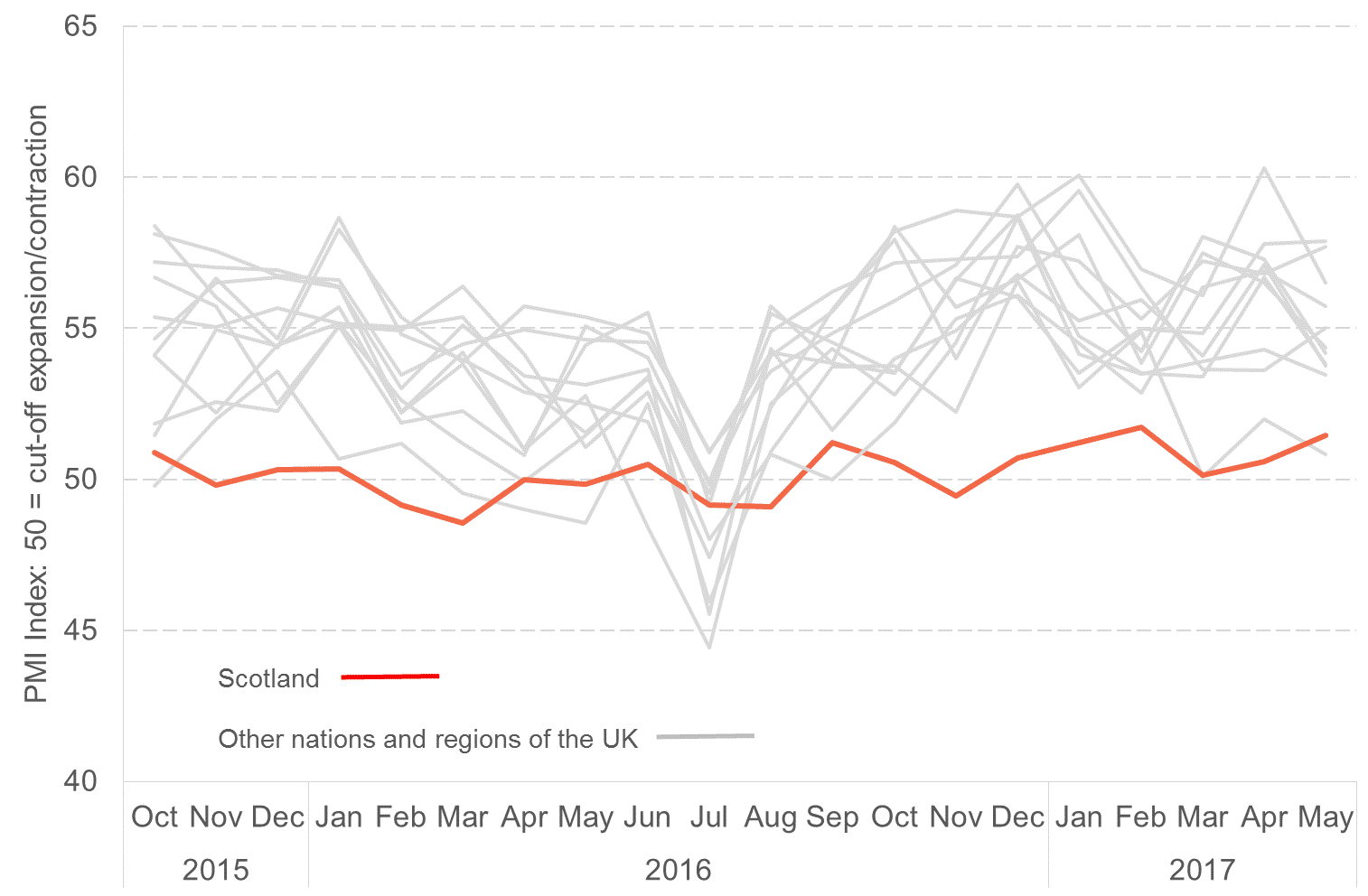

And with the UK growing more quickly, it’s not entirely clear that this can be explained (yet) by a unique Brexit hit in Scotland vis-à-vis the UK.

Scotland vs. the rest of the UK: PMI

Source: Markit IHS

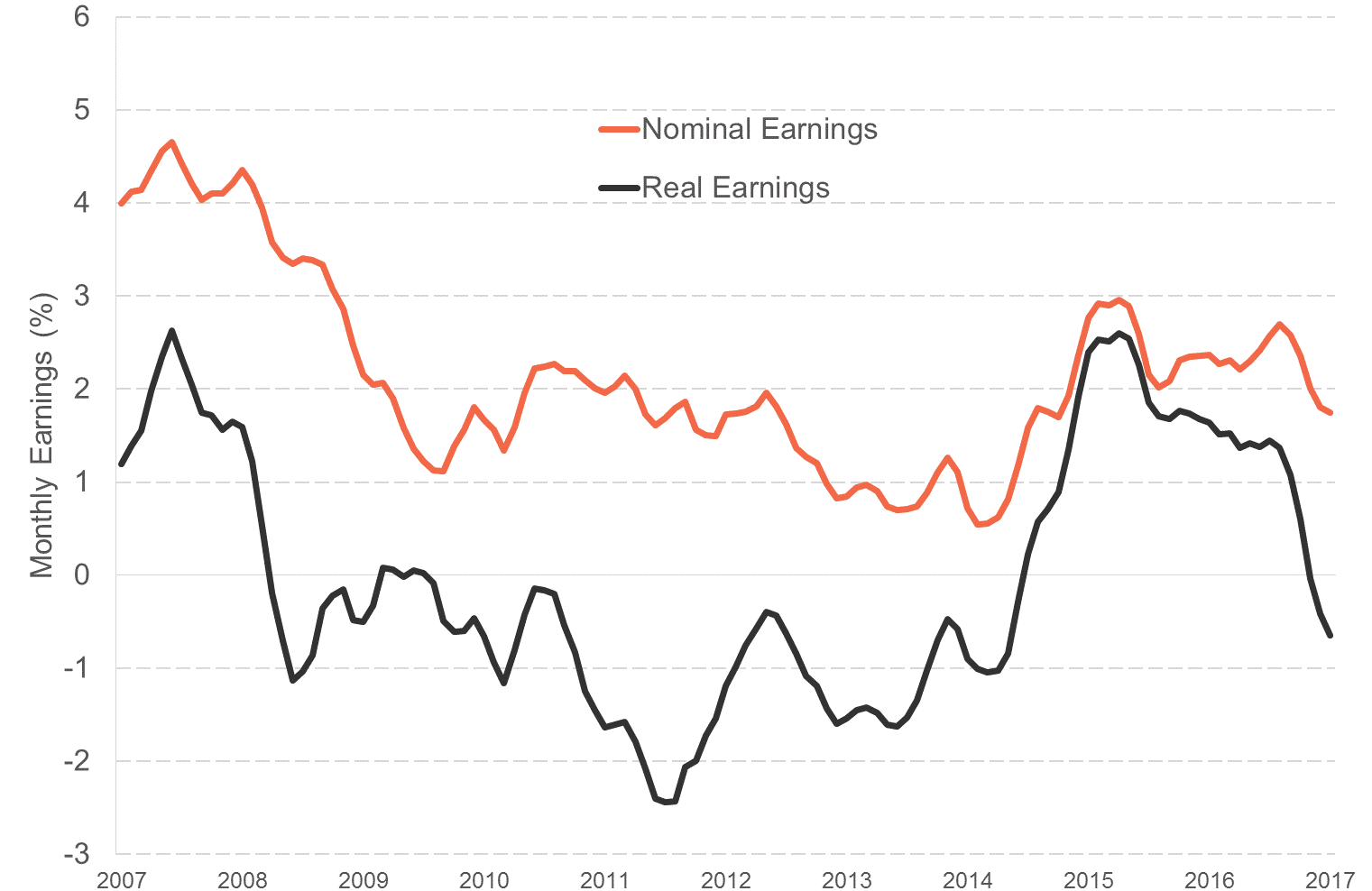

6. Finally, what does all this mean in the real world? Unfortunately, it looks as though households will have longer to wait for a sustained increase in their living standards.

Earnings across the UK have fallen once again…

UK average weekly earnings: 3-month average on same time a year ago

Source: Thomson Reuters Datastream, ONS

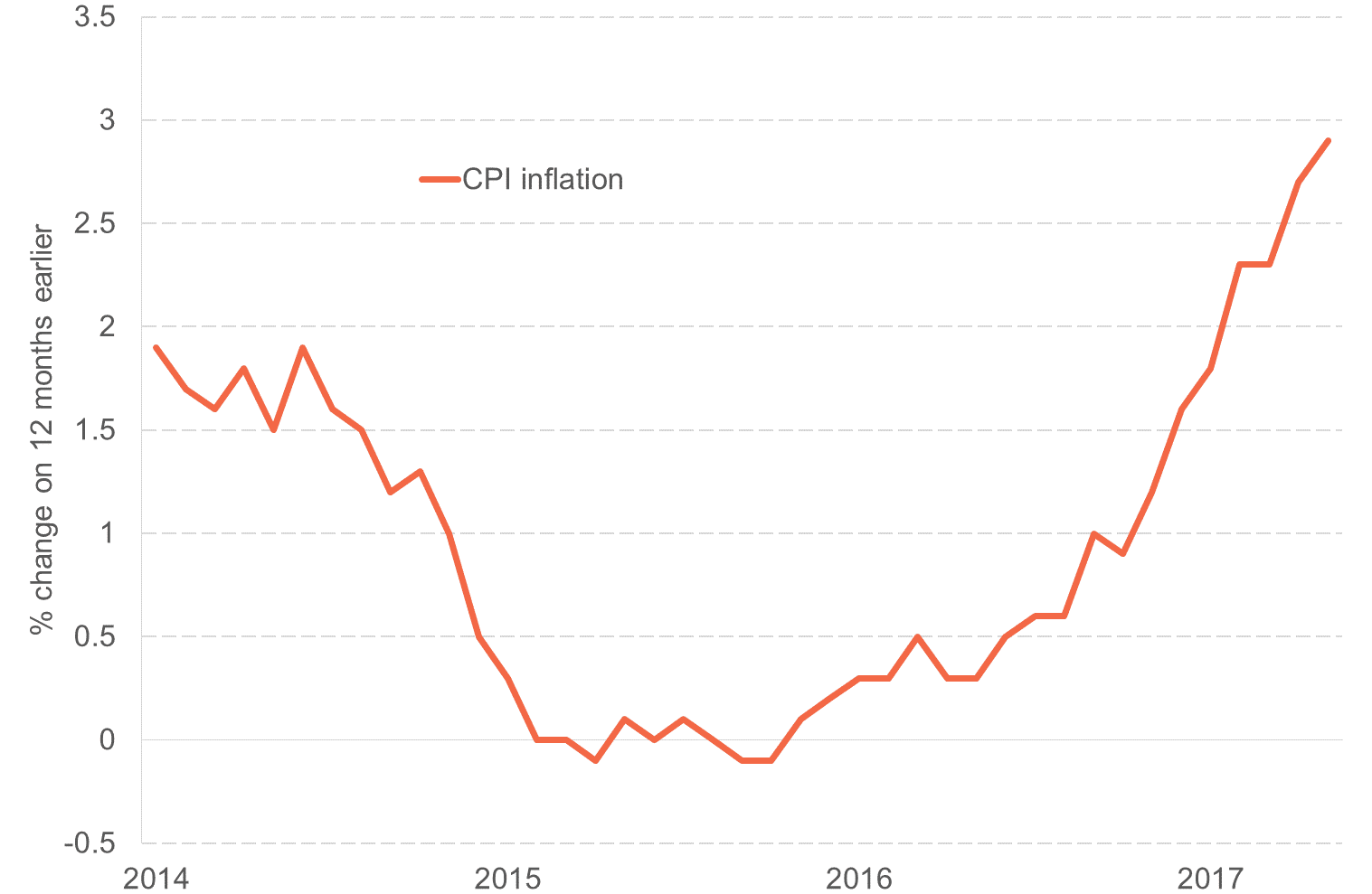

…..and with inflation expected to pick-up in the coming months, household budgets are likely to continue to be squeezed.

Inflation rising (and likely to exceed 3% in the next few months)

Source: Thomson Reuters Datastream, ONS

Authors

The Fraser of Allander Institute (FAI) is a leading economy research institute based in the Department of Economics at the University of Strathclyde, Glasgow.