We’ll soon find out what the Scottish Government has in store for income tax in Scotland in 2019/20 when the Scottish Budget is published next week.

Taxpayers in the rest of the UK already know what to expect after Chancellor Philip Hammond announced changes to income tax in the UK Budget at the end of October.

These were to:

- increase the personal allowance from £11,850 in 2018/19 to £12,500 in 2019/20

- to increase the Higher Rate Threshold in the rest of the UK from £46,350 to £50,000.

As it is entirely possible that readers might not have made it through our 160 page Budget report on the 8th November, this blog will set out some tax options available to Mr Mackay for the forthcoming year.

Before we do so, here is a summary of the differences between Scottish and rUK taxpayers in the current financial year.

2018/19

Last year, the Scottish Government implemented major changes to income tax – moving from a three band tax structure to a five band tax system on non-savings non-dividends income (NSND).

In 2018-19, Scottish taxpayers pay:

Starter rate: 19% tax on over the personal allowance (£11,850) but below £13,850;

Basic rate: 20% between £13,850 and £24,000;

Intermediate: 21% between £24,000 and £43,430,

Higher rate: 41% between £43,430 and £150,000;

Top rate: 46% over £150,000.

The minority SNP government initially proposed – in its draft budget – increasing the higher rate threshold in line with inflation to £44,273. But as part of the budget deal with the Scottish Greens, the HRT was increased by just 1% to £43,430.

In the UK, the three band structure and rates were maintained, with the higher rate threshold increased to £46,350 in 2018/19.

As a result, Scottish income taxpayers with income below £26,000 pay slightly less tax in 2018/19 than those in rUK – with a maximum difference of £20. Those with income above £26,000 pay somewhat more tax than individuals in rUK with an equivalent income.

The Scottish Fiscal Commission forecast that the Scottish Government’s 2018/19 income tax policy would raise around £219m in additional revenue, compared to a policy of keeping the three-band rate structure, and increasing thresholds in line with inflation.

2019/20

The Scottish Government has no control over the personal allowance which is set at a UK level.

Giving evidence to the Scottish Parliament in June, Mr MacKay said that he believed that Scotland’s new five-band income tax schedule should be seen as ‘settled’. However, he did not rule out changes to the rates or thresholds within this structure.

Given this, there are a number of options available to the Scottish Government.

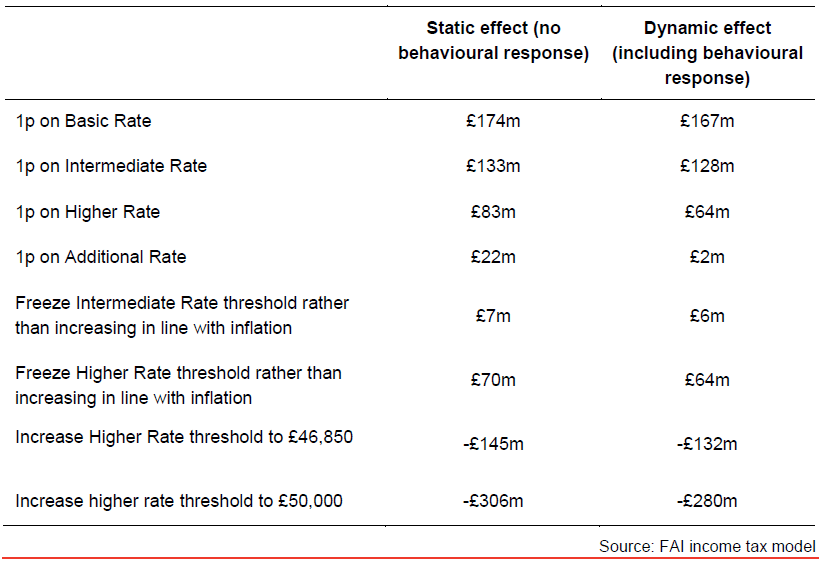

Some of these options for 2019/20 – retaining the existing five band structure – are shown in the table below, together with their estimated revenue effects. Our behavioural estimates are subject to particular uncertainty. They are estimated using broadly similar assumptions to those adopted by the Scottish Fiscal Commission.

Of course, whilst these are all options for the Scottish Government, there is a balance to be met between raising revenues overall; the perception of tax differences at the individual level between Scottish and rUK taxpayers; and the requirement for support from another political party to pass the Budget.

On the one hand, with the UK HRT going up to £50,000, there is the possibility for a widening portion of Scottish taxpayers to face significantly higher rates of taxation than those in rUK – should the Scottish Government choose to increase the Scottish HRT by proportionally less than it has been increased in rUK.

An inflationary increase in the threshold in Scotland would take it to around £44,470. This would widen the gap between the liabilities of Scottish and rUK higher rate taxpayers even further than in 2018/19. If this was the case, a taxpayer earning £50,000 would face an income tax bill some £1,350 higher than an rUK counterpart – although it would mean a reduction of around £60m in revenues compared to a policy of freezing the higher rate threshold.

On the other hand, if the higher rate threshold was increased by the same percentage as it has been increased in rUK, this would take it to £46,850. Whilst this would reduce the liability differential at an individual level, the tax cut on higher rate taxpayers would cost the government around £130 million in lost revenues compared to a policy to increase the threshold in line with inflation.

Politically, it remains to be seen whether such a policy could be supported by the Scottish Greens, whose support the minority government has required to get the Budget Bill through Parliament in each of the last two years – regardless of what the rUK policy is. One hypothesis is that the draft budget will propose a moderate real terms increase in the threshold, in anticipation of it being negotiated back towards the existing level as part of the budget deal.

Alternatively, perhaps 2019/20 will be the year that the higher rate threshold ceases to be the cornerstone of the budget deal. The leader of the Scottish Greens, Patrick Harvie, wrote to Nicola Sturgeon earlier this year to point out that progress on local tax reform would be the party’s next area of ‘constructive challenge’ when it came to negotiating a budget deal in 2019/20.

This brings us to an important point about income tax being viewed in isolation, rather than looking at policy changes from a distributional perspective.

For instance, councils across Scotland implemented a 3% council tax rise in 2018/19. Whilst this will raise around £70m to support local government spending, the distributional effects of this tax increase generally offset any gains that households might gain from the introduction of the lower 19% starter rate. Households in the lower end of the income distribution are generally not affected by income tax changes on average, as they do not earn enough tax to pay 1% less tax on their earnings between the personal allowance and the Starter Rate threshold.

Over the course of the next few days, we’ll be publishing a series of blogs in the run up to the Budget. We’ll reflect on the announcements in our free post Budget event next Friday.

Authors

The Fraser of Allander Institute (FAI) is a leading economy research institute based in the Department of Economics at the University of Strathclyde, Glasgow.