The UK Budget is still more than a week away, but it feels very long in the tooth already.

No wonder, though – briefings have been nonstop since the OBR was first commissioned to deliver its forecast updated on 3 September. But the speculation has reached a fever pitch in the last few days. From unusual pre-Budget speeches by the Chancellor to briefed U-turns on policies that had yet to be announced, Budget-mania is running wild through Westminster and the UK at large. It feels a million miles away from the promise of politics treading more lightly on the general public’s lives.

Why is this such a difficult fiscal event for the Chancellor?

It’s worth going back to Rachel Reeves’ previous fiscal statements to understand just how she has ended up in such a conundrum.

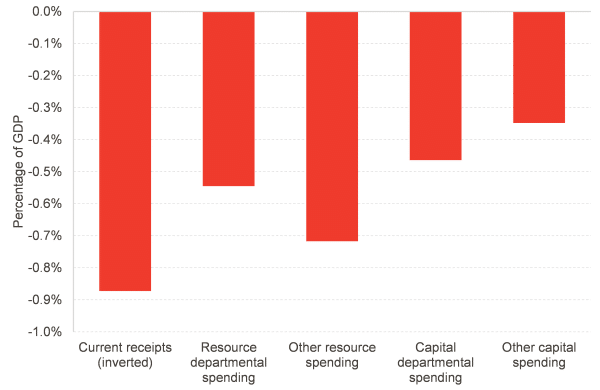

Last year, the Chancellor arrived at 11 Downing Street to find a relatively challenging set of circumstances. Jeremy Hunt had greatly reduced the ‘fiscal headroom’ – but which we mean the difference between his plans and what it would take to break the fiscal rules – to around £9bn, or just over 0.25% of GDP. Given that the average OBR forecast error five years out is 0.7% of GDP, this was clearly a hostage to fortune.

Not only that, but Jeremy Hunt had just cut employee National Insurance Contributions by 4 percentage points, at an annual cost of £20 billion. The sums added up only due to frozen tax thresholds – which raised receipts by around 1% of GDP over the five years – and spending falling by 2% of GDP, of which half was due to falling departmental spending relative to the size of the economy.

Chart 1: Breakdown of changes to net borrowing from 2023-24 to 2028-29 in Jeremy Hunt’s last fiscal event

Source: FAI analysis of OBR March 2024 Economic and Fiscal Outlook

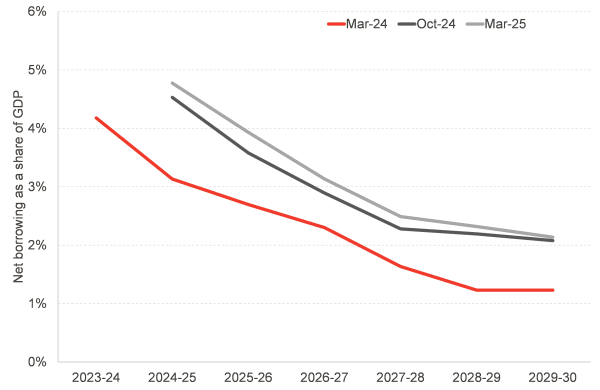

Rachel Reeves’ October 2024 Budget was very different in approach to Hunt’s. Departmental spending was substantially loosened, and while tax rises – particularly on employer NICs – raised nearly 1% of GDP in revenue, they were more than dwarfed by an increase in spending double that. The result was net borrowing higher in every year than was planned by the previous Government.

Chart 2: Successive forecasts for public sector net borrowing

Source: FAI analysis of OBR March 2024, October 2024 and March 2025 Economic and Fiscal Outlooks

Note that there’s still a large drop in the deficit towards the end of the decade, although from a higher point and at a less steep pace – particularly from 2027-28 onwards.

How did Reeves manage to achieve this, when Hunt had left such a small buffer against breaking the fiscal rules? She changed them, of course, making them less strict. On Hunt’s definition, the October 2024 forecast would have broken the debt rule.

But even with the less strict rules in place, all the headroom ‘gained’ was quickly exhausted by the increase in spending funded through borrowing. It meant that, much like her predecessor, Rachel Reeves would have no insulation against a negative shock – just £9.9 billion, or 0.3% of GDP. Remember that the OBR’s average forecast error is more than double that – so the Chancellor was left extremely exposed.

Bad news just kept on coming

After a January in which gilt yields kept climbing and the noises about tariffs from the budding Trump administration, the negative shocks that the Chancellor was relying on not coming to pass crystallised all at once. By the time she came to present the Spring Statement, she would have broken the current balance rule in the absence of any policy.

Faced with that prospect, the Chancellor pushed through a set of controversial measures on welfare, particularly aimed at restricting the eligibility for incapacity and disability benefits. These were combined with some typical Treasury chicanery that reduced assumed RDEL spending beyond the Spending Review period (more on this later).

The welfare cuts were not only controversial, but led to a significant revolt amongst backbenchers, and were eventually nearly fully scrapped in chaotic scenes in early July. This followed on from a reversal of last year’s cut to winter fuel payments, and together pretty much eroded the razor-thin £9.9 billion headroom that had been restored in March.

The OBR’s long-awaited productivity review makes things harder

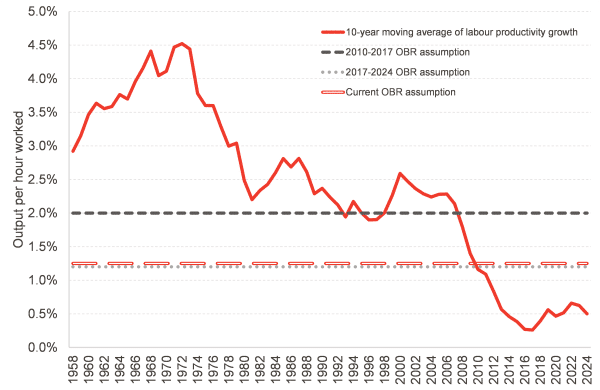

Over the Summer, the OBR has been reviewing its productivity assumptions. When it was created in 2010, the assumption was that growth in output per hour would return to the 2% it had averaged before the Financial Crisis.

Chart 3: Long-term averages of productivity growth compared with the OBR’s assumptions

Source: FAI analysis of OBR, ONS and BoE data

The OBR had already revised its assumption on productivity down to around 1.2% a year in 2017, but that too proved much too optimistic. It has not come close even to that lower figure, averaging around 0.5% over the past decade.

It is then unsurprising that the OBR is looking to finally adjust its view to be more in line with outturn data – even if it will probably still end up at the upper end of optimism among forecasters.

Why does this matter? Productivity growth drives growth in real wages, which in turn increases tax receipts. Slower growth reduces tax receipts, with the progressivity of the system increasing the size of that hit as fewer people end up in the higher tax bands.

With spending plans laid out in cash terms or linked to other variables, slower productivity increases the structural deficit, which leaves the Chancellor with a menu of pretty ghastly options. While she could in theory just borrow the additional funds, there are two main barriers to it:

- She is already close to breaking the fiscal rules, and the increase in borrowing from a downward revision in productivity would be enough to break them;

- But more importantly, bond investors are already demanding high yields in return for buying UK Government debt. A large increase in debt issuance would exacerbate these pretty high yields, and is therefore not feasible.

The Chancellor could of course cut spending to bring it in line with new (that is, more pessimistic) projections for tax revenues by the end of the decade. But just 5 months on from the Spending Review, reopening departmental settlements in the short run seems unlikely. And given the problems the Government had with the welfare cuts in the Summer, cutting other types of spending is politically hard to achieve.

This leaves tax rises as the likely outcome, and this is what the Government has been trailing all Autumn. Depending on how big the revision is, we think there might be as much as £20 billion needed to get back to not breaking the fiscal rules, plus any headroom that Rachel Reeves might want to have (more on this later).

The risks of going down the smorgasbord route

One option that was floated in the past few weeks was to go for a big, manifesto-breaking increase in income tax rates. Note that there are different rates in Scotland, and we have covered the knock-on effects of this on the Scottish Budget in detail.

In pure economics terms, this would be the cleanest solution. It would raise substantial amounts of revenue with a very high degree of confidence, and would not be overly distortionary. The basic rate in particular is paid by all people paying tax, and therefore it would mean a relatively small increase in tax for a large number of people.

Combined with this was talk of a ‘2 up, 2 down’ option, in which the basic rate of income tax would be raised to 22p while employee NICs would be dropped to 6p in the pound. This would be an economically sensible policy: Class 1 NICs are only paid on employment income by those below state pension age, while many more types of income are subject to income tax: rental income, pension income, savings, to name but a few. It would reduce the wedge between employment and other forms of income, leaving the net pay of employees untouched, it would not change the cost of employment and would raise a significant amount of money.

But on Thursday last week the FT reported that the Chancellor had ditched the income tax rise. Instead, she would opt for the so-called ‘smorgasbord option’, which would see a set of piecemeal, targeted tax rises in place of a big-bang rise in income tax.

To say bond markets were unimpressed is an understatement – gilt yields are around 0.2 percentage points higher from already historically high levels. But the decision appears to be based on the political deliverability and electoral consequences of breaking a manifesto pledge rather than cold, hard public finance calculations.

The smorgasbord route, though, is full of hidden traps. It will of course add up for this forecast on the basis of the scorecard, but there’s no guarantee it will actually raise the revenue it is intended to. The freezing of thresholds is likely to be a sure bet (although we think this was always going to happen), but measures such as a tax on electric vehicles, restricting salary sacrifice on pensions and gambling levies will come with high or very high uncertainty ratings by the OBR. This will reflect the fact that they affect a much smaller set of people who will be hit much harder – and who therefore have a larger incentive to respond to the changes or make their displeasure heard than someone whose pay packet changed by a much smaller amount.

There’s also a risk in terms of coordinated campaigns by those badly affected by the changes. Those of us old enough to remember the Omnishambles Budget of 2012 and the debate as to whether a cold pasty would still be taxed as hot food will know just how much of a fuss can come from a seemingly small measure.

And if the measures don’t raise as much as intended, we could well be in the same position in a few months’ time. The cold buffet might look tempting, but a main course would definitely fill the appetite – so it’s a big risk to say no to it.

How much headroom is enough?

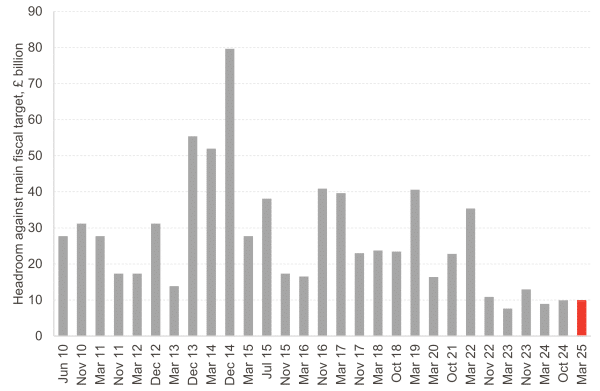

One of the main reasons for the difficulties faced by the Chancellor is how loose her fiscal policy has been – at that of all recent Chancellors since Philip Hammond, to be fair – relative to the fiscal rules. The £9.9 billion headroom against meeting the current budget rule was the joint-third lowest since the OBR was created, and follows a pattern since 2017 of shrinking buffers against shocks.

Chart 4: Headroom against the main fiscal target since 2010, with the latest fiscal event highlighted

Source: OBR

Coincidentally, this has been the whole time since the last OBR revision in productivity, which suggests that successive Chancellors have chosen not to adjust spending in line with a lower path for tax revenues, but instead to run riskier fiscal policy. But luck and fiscal space have finally run out, and the latest productivity downgrade looks set to force the Chancellor’s hand.

It continues to be briefed that the Chancellor remains intent on increase the fiscal headroom, having recognised that the buffer she has left herself has been too small to avoid having to increase taxes or cut spending in the face of events. This would be welcome, but although the noises are positive, the details are less encouraging. The Guardian reported that Reeves wants headroom of £15 billion, which eagle-eyed observers will spot would still put it at historically low levels.

Not to sound like a broken record, but the average forecast error is 0.7% of GDP, which would amount to around £25 billion. Anything less than that is not enough to cope with regular levels of uncertainty, and there is a good argument that a bit more than that would be the sensible course of action. So it’s quite likely that this would might be eroded in one or two forecasts’ time, and whoever is Chancellor then might have similarly unpalatable choices to make.

Smoke and mirrors expected

We’ll also be on the lookout for some hidden tricks that the Chancellor might pull to make her sums add up. Of course, we expect the fiction of increasing fuel duty to continue to embellish future years’ revenues – it would be a shock if the first increase since 2011 finally took place.

In her interview last week, Rachel Reeves mentioned that sticking to the manifesto plans might imply capital spending cuts. Not only does this imply that the main constraint is the debt rule (on net financial liabilities), as otherwise capital spending would make no difference. But we suspect there could be some bringing forward of spending from 2029-30 to make the figures add up. It would be hard, however, to cut capital spending from settlements that run until that year given the Spending Review was only in June.

However, the Chancellor might well be tempted to massage the resource departmental spending assumption for 2029-30 onwards, which is beyond the Spending Review period, even if she has no intention of delivering this. If she were to do so, she would be following in the well-trodden footsteps of Chancellors like George Osborne and Jeremy Hunt, who pencilled in undeliverable spending cuts to make projections add up. OBR Chair Richard Hughes raged against the ‘work of fiction’ in the Hunt plans, and if Reeves did the same, this Budget too might end up closer to the Booker Prize stakes than the annals of forecast accuracy.

Authors

João is Deputy Director and Senior Knowledge Exchange Fellow at the Fraser of Allander Institute. Previously, he was a Senior Fiscal Analyst at the Office for Budget Responsibility, where he led on analysis of long-term sustainability of the UK's public finances and on the effect of economic developments and fiscal policy on the UK's medium-term outlook.