As expected, the Bank of England increased interest rates today by 0.25 percentage points to 0.5% — the first interest rate rise in more than a decade.

So what might today’s announcement mean for the Scottish economy?

Today’s rate rise

Before discussing how today’s decision might impact on Scotland, it’s important to put the interest rate rise in context.

Interest rates have been extremely low for some time now. The new rate is still therefore well below ‘normal’, with monetary policy still extremely supportive of growth.

Today’s announcement should be seen as modest removal of some of the stimulus to the economy that the Bank has been providing rather than a sharp tightening of monetary policy.

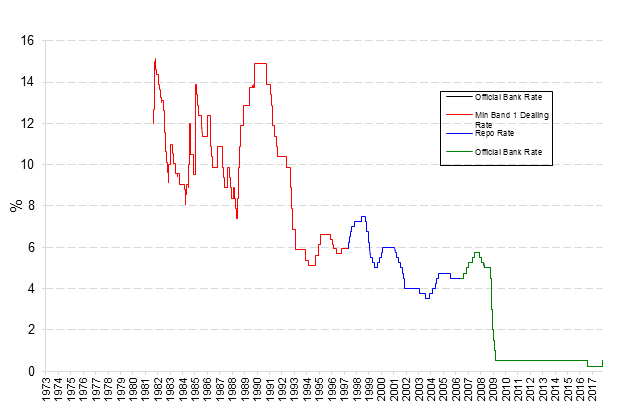

Moreover, as the chart highlights the increase to 0.5% just takes us back to where we were prior to the Bank’s decision to cut interest rates to 0.25% in August 2016.

If you recall back in summer 2016, a range of indicators were suggesting that the ‘shock’ of the EU referendum outcome might tip the UK economy into a sharp slowdown (or even recession). The cut to 0.25% – plus the additional round of Quantitative Easing – was largely an immediate response to help prop up the economy and to boost confidence.

In the end, growth has proven to be more resilient

Changes in Bank Rate

So today’s increase in itself is not that significant on its own. Nor is it a surprise, with the Bank having signalled for weeks now that a rate rise was likely.

What is much more significant is what the decision says about the future direction of travel for monetary policy in the UK. And here the Bank says that future increases will be “at a gradual pace and to a limited extent.”

Why has the Bank increased rates?

The decision to increase interest rates will have been considered carefully by the MPC.

On the one hand, the decision to increase rates might seem to have been an obvious one.

The Bank has a target for inflation of 2%. It is currently 3%.

And as highlighted above, UK growth has been stronger than the bank expected when they cut interest rates in 2016. Back then, the Bank was forecasting growth of +0.8% for 2017. Now they are forecasting +1.6% for 2017. Employment is also at near record highs.

But this is only half the story.

Much of the rise in inflation is believed to be temporary and driven by the sharp depreciation in Sterling witnessed over the last year. The fall in the value of Sterling pushes up the cost of imports. Core – or underlying – inflation is believed to be much lower (and closer to target). High employment is not (yet) leading to too much pressure on wages.

At the same time, whilst the economy has performed better than the Bank thought, the outlook remains highly uncertain. Indeed the Bank think that the economy will grow more slowly next year (growth of 1.6% for 2018) than they did when they cut interest rates in 2016 (when they were predicting growth of 1.8% for 2018). Should the Brexit negotiations take a further turn for the worse, then the outlook could look less positive.

From a strict macroeconomic perspective, the case for a rate rise might be seen to have been in the balance. In the end it was pretty emphatic with a 7-2 vote in favour of the rise.

Some of this may also reflect some concerns the Bank has had over the recent growth in consumer debt. The rise in unsecured lending – particularly car-loans – has been something that has caught the attention of both the Monetary Policy Committee and the Financial Policy Committee. By raising interest rates, the hope is that this will help to gradually cool any signs of too much debt being accumulated

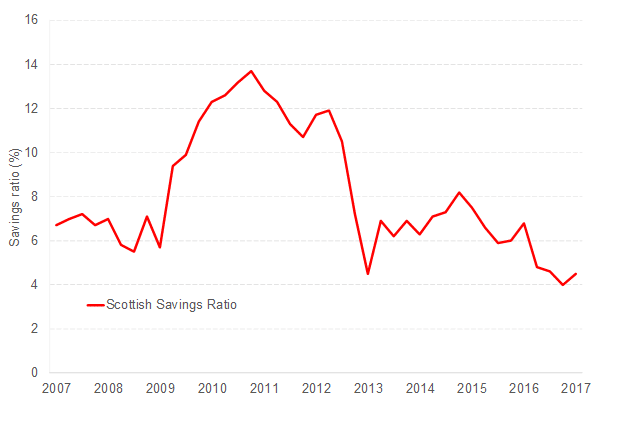

Savings Rate in Scotland – below that even during the credit boom just before the financial crisis

So what does this mean for Scotland?

Normally, a change in interest rates of 0.25% would be expected to only have a modest impact on growth.

In our modelling, raising rates by 1 percent is estimated to reduce output by between 0.5 and 0.7 percent over a 2-3 year period. So a quarter point rise could be expected to only trim around 0.15 percent from GDP.

However, today’s increase may have a larger impact if markets and businesses interpret the change as a clear signal that monetary policy will be tightened in the coming months.

There is also an important Scottish dimension to all of this. As we know, in recent times the Scottish economy has been lagging behind the UK as a whole.

The latest figures confirm that even with the standout performance of a number of sectors in Q1 2017, Scottish growth is around 1/3 that of the UK as a whole.

So whilst the Bank may judge that the UK economy is in sufficiently robust health to cope with a rate hike, a rate rise in Scotland may be more of a challenge.

That being said, the increase for now is still relatively modest when compared to our own latest forecasts.

But with the latest official retail figures published yesterday showing zero growth in Q3 2017 and consumer confidence still negative, it is clear that Scottish households are still finding economic conditions challenging.

Tighter monetary policy – and the impact this could have on Scotland vis-à-vis rUK – is only another factor that the Scottish Fiscal Commission now need to take a view on as we get ever closer to the Scottish Budget

Authors

The Fraser of Allander Institute (FAI) is a leading economy research institute based in the Department of Economics at the University of Strathclyde, Glasgow.