The FAI has been doing lots of work recently to try to understand what the data is telling us about the differential impact of the COVID-19 pandemic on regional economies. As part of this, we have held some business webinars to find out how this data chimes with the experience of firms in these economies.

This article summarises some of our main findings on the effect the pandemic has had on GVA, local businesses, trade, and the labour market in West Midlands and has been published as part of our contribution to the ESCoE project.

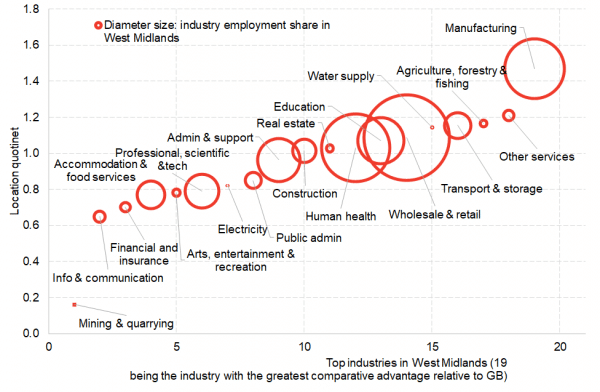

The West Midlands economy is different from the rest of GB due to its unique sectoral make up. Chart 1 below shows location quotients which indicate the sectors where West Midlands has a larger share of employment than the UK average. A location quotient of 1 implies that there is a larger share of employment in a given sector in West Midlands compared to GB as a whole.

Chart 1: Location quotients for West Midlands and the UK

Source: BRES, FAI calculations

West Midlands clearly has a heavier concentration of jobs in the manufacturing sector. Furthermore, the wholesale & retail sector is the sector which employs the most people.

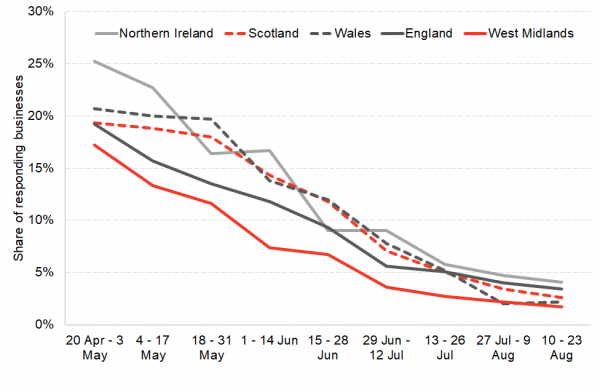

Manufacturing took a strong hit at the start of the pandemic. However, as shown in Chart 2, despite facing lower demand and capacity utilization, a lower percentage of businesses have had to completely pause trading in West Midlands compared to other UK regions.

Chart 2: Share of businesses which are temporarily closed or have paused trading, West Midlands & UK nations, 20th April – 23rd August 2020

Source ONS BICS

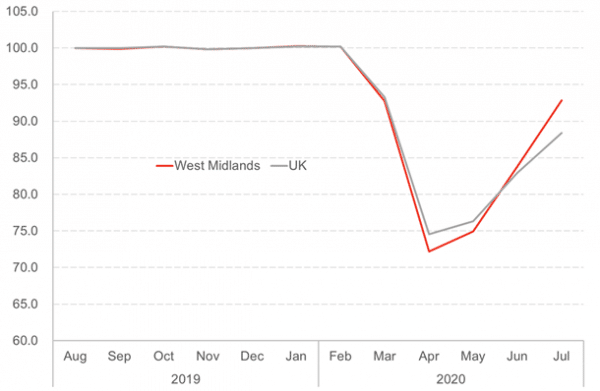

This meant that once demand started picking back up again businesses in West Midlands were able to quickly utilise spare capacity and resume production. Our modelling thus shows that due to its sectoral make-up the West Midlands economy has initially fallen more sharply compared to the UK average, but it has been able to recover slightly faster – Chart 3.

Chart 3: Modelled monthly GVA based on sectoral employment shares, West Midlands and the UK, August 2019 – July 2020

Source: ONS, FAI calculations

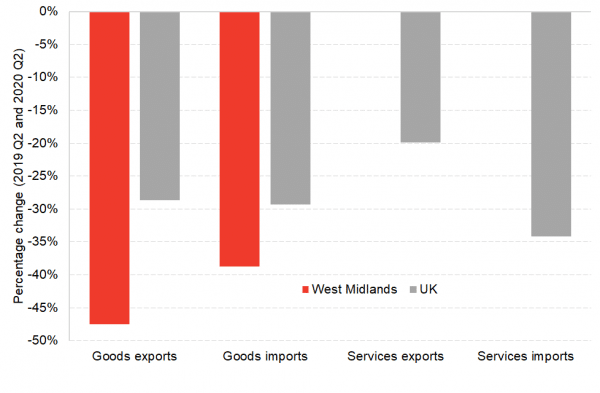

Data from the ONS Business Impact of Coronavirus Survey shows that during the second half of May around a third of all businesses in West Midlands have had challenges with exporting activity due to Coronavirus-related transport restrictions. This has resulted in a sharp decline in the volume of trade to and from the West Midlands – Chart 4.

Chart 4: Exports of goods and services, West Midlands and the UK, 2019 Q2 – 2020 Q2

Source: HMRC, ONS, FAI calculations

In Q2 of 2020 goods exports from West Midlands fell by 48% y-o-y. This compares to a decline of only 29% for the UK. The primary factor behind this difference is the heavier reliance of the West Midlands economy on the manufacturing of goods, whereas the UK economy has a higher concentration of economic activity in the service sector, where trade has been less severely affected.

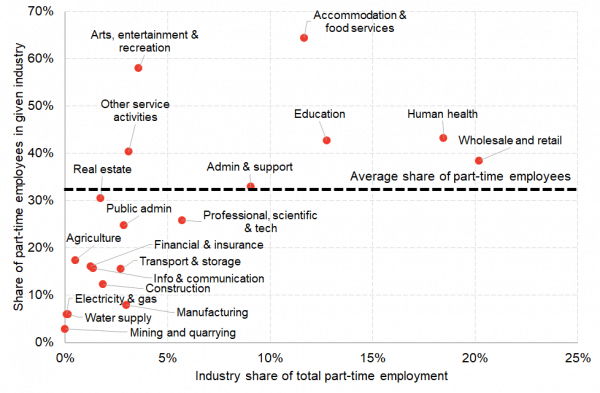

Economic output is an important indicator of performance, but the effect of the downturn on the labour market is a key determinant of wellbeing of workers. In general, part-time workers are more likely to have zero-hour contracts and see falls in working hours during economic downturns. They are also typically less trained than full-time workers and may thus be more vulnerable when businesses decide to implement job cuts. Furthermore, part-time workers are more prevalent in some sectors of the West Midlands economy compared to others – Chart 5.

Chart 5: Share of part-time workers in each industry and industry’s share of total part-time employment, West Midlands, 2018

Source: BRES, FAI calculations

The wholesale and retail sector, which supports the highest number of jobs in West Midlands, has a slightly above average share of part-time employment. However, accommodation & food services and arts, entertainment and recreation are sectors which employ the highest proportion of part-time workers relative to full-time workers. These are also the sectors where activity has been most negatively impacted by the lockdown and social distancing measures.

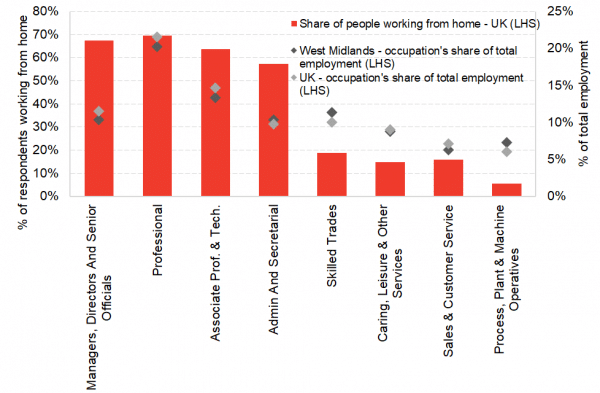

Some companies have been able to adapt to social distancing measures by allowing employees to work from home. However, not all workers are able to work from home.

Chart 6: Share of people working from home across different occupations (UK, April 2020) and share of total employment of each occupation (West Midlands & UK, 2018)

Source: ONS UK Labour Market Survey, LFS/NOMIS

Approximately two thirds of workers across the UK in managerial and professional occupations have worked from home at some point since the start of the pandemic. However, less than a fifth of all workers in low-skilled occupations were able to work from home. Chart 6 shows that West Midlands has a higher share of employment in these low and mid-skilled occupations than the UK average and as a result may have a lower share of workers capable of homeworking.

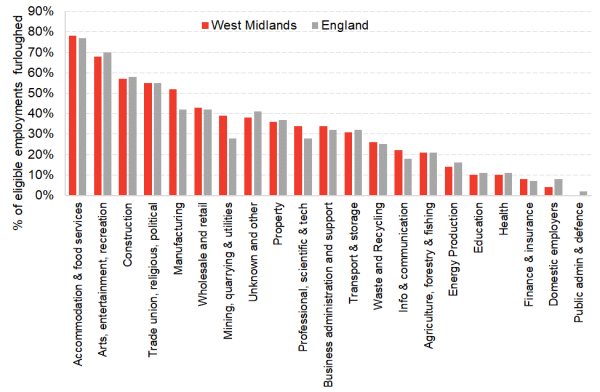

For those employees who have not been able to transition to homeworking companies have made wide use of the UK Government’s Coronavirus Job Retention scheme to support jobs. The magnitude of ‘furloughing’ has also varied amongst different sectors of the West Midlands economy.

Chart 7: Share of eligible employments furloughed by sector, West Midlands and England, July 2020

Source: HMRC

In July, 78% of workers in accommodation & food services, 68% in arts, entertainment and recreation, 57% in construction were on furlough in the West Midlands. The most important sectors of the local economy, manufacturing & wholesale & retail, had between 40 – 50% workers furloughed. The share of furloughed jobs halved in August as the scheme is gradually wound down. Nevertheless, as we have previously pointed out in our October labour market update, it remains uncertain how many of these positions will still exist after the furlough scheme ends.

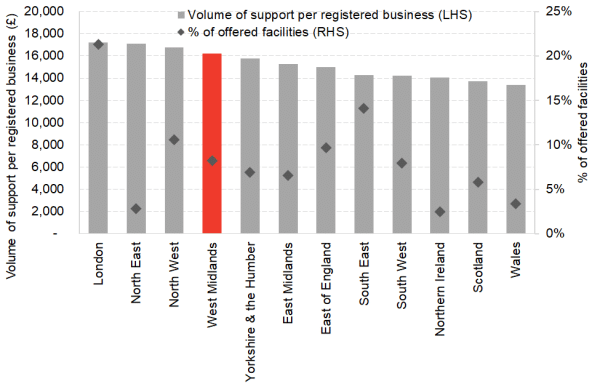

The UK Government has also supported companies through the CBILS and BBILS schemes. These schemes have provided support cash-flow support to businesses who were facing declines in demand. Chart 8 shows that businesses in West Midlands benefited from this scheme generously compared to other UK regions, with circa £16,000 awarded per registered business.

Chart 8: Amount of support for businesses under the UK Government’s CBILS and BBLS schemes, English regions & devolved nations of the UK, up to 27th August 2020

Source: British Business Bank, FAI calculations

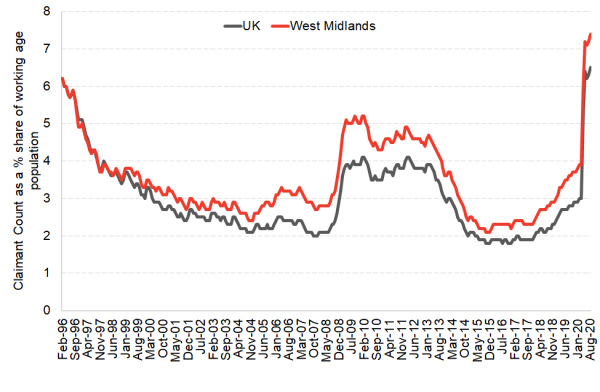

Despite the supporting measures from the government, not all jobs in West Midlands could be saved. It will be some time before headline labour market data such as the unemployment rate fully reflects the effect of the pandemic. In the meantime, the Claimant Count (the number of people on Job Seeker’s allowance and Universal Credit) can serve as an early indicator of people who have lost their jobs.

Chart 9: Claimant Count as a share of working age population, West Midlands, and UK, February 2016 – August 2020

Source: NOMIS

The Claimant Count as a share of working age population rose from 3.9% in February to 7.4% in August in West Midlands. The magnitude of increase has been similar to rUK, but structural factors in the West Midlands labour market have meant that historically the region has had a higher share of claimants.

Summary

The West Midlands labour market has been sharply affected at the beginning of the pandemic, but its sectoral mix has allowed GDP to start recovering faster compared to rUK once the lockdown was eased. Trade in goods declined significantly in West Midlands due to its reliance on the manufacturing industry. Furthermore, a higher concentration of jobs in low-skilled occupations means that only a small share of employees in West Midlands can work from home.

Early data shows signs of redundancies and job losses being on the rise in both West Midlands and the UK, which may be further exacerbated once the furlough scheme comes to an end.

Given the reliance of the West Midlands Economy on manufacturing, the looming end of EU exit transition period also adds to the uncertainty over the outlook. As restrictions are reintroduced and/or tightened, all parts of the UK economy face a challenging outlook. It is incumbent on Governments at all levels to consider the differential impacts on regional economies and what may be required to support the recovery to come.

Authors

Frantisek Brocek

Frank graduated from the University of Strathclyde in 2019 with a First-class BA (Hons) degree in Economics. He is currently studying on the Scottish Graduate Programme MSc in Economics at the University of Edinburgh.

He has experience from a variety of economic policy institutions including the European Commission in Brussels, the Slovak Central Bank and the Ministry of Finance.

Mairi is the Director of the Fraser of Allander Institute. Previously, she was the Deputy Chief Executive of the Scottish Fiscal Commission and the Head of National Accounts at the Scottish Government and has over a decade of experience working in different areas of statistics and analysis.