There has been much speculation about what the Scottish Government may choose to do with income tax when they put forward their Budget proposals this December.

This blog looks at some options and the amount of money that could be raised.

The outlook for the Scottish Budget

Our recent Scotland’s Budget report highlighted pressures on the budget through a mix of continuing UK fiscal consolidation and a fragile economic outlook.

Our report also highlighted how major Scottish Government commitments, in health, childcare, police and education, means that over half of the Budget can already be viewed as ‘protected’. This means that other public services must pick-up more of the burden.

Based on current plans, ‘non-protected’ areas could face real terms cuts of between 9%-14% over the current parliamentary term.

But this is not all. Some legacy payments – particularly those connected to past PFI/NPD commitments – tie up even more of the budget. New policy commitments also continue to be added, like lifting the 1% pay cap for public sector workers.

And whilst Scotland’s forthcoming social security powers provide opportunities to design new (and better) policies, there are significant financial risks attached to them.

The scope to raise income tax

Last year, the Scottish Government opted to set a different higher tax threshold than the UK. Whilst this was not a direct tax increase per se, under the new Fiscal Framework, it boosted the Scottish Budget because Scottish revenues grew more quickly than the Block Grant Adjustment.

The political momentum to go even further this year is gathering pace.

Last month, three of the opposition parties – the Greens, Liberal Democrats and Labour –backed the principle of raising income tax. The SNP abstained, instead promising to bring forward a paper outlining options for raising revenues before December’s Budget.

So what are the options? And how much revenue could be raised?

The government now has a relatively wide menu to choose from. Here are some possible options –

- Putting 1p on the basic, higher and additional rates would raise just under £500 million;

- Freezing the higher rate threshold at £43,000 in 2018/19 (rather than increasing it in line with inflation) would raise around £90 million;

- Putting a penny on both the higher rate and Additional Rate (so that these are 41p and 46p respectively) would raise around £130 million in 2018/19;

- Introducing a new 30p rate from £35,000 to the higher rate threshold would generate around £420 million in 2018/19;

- Reducing the threshold at which the Additional Rate becomes payable, from £150,000 to £80,000, would raise around £130 million in 2018/19; and,

- Raising the Additional Rate from 45p to 50p would raise around £145 million.

There is an important caveat. The numbers listed above are ‘static’ estimates – i.e. they estimate the revenues that could be raised provided taxpayer behaviour does not change.

But will some taxpayers choose to switch some (or all) of their earnings into dividends and savings (still set by the UK Government) to avoid higher taxes in Scotland? In the current financial year, a Scottish taxpayer has a higher rate limit of £43,000 for earnings, but £45,000 for savings and dividends. Will higher income individuals choose to re-locate? Will higher taxes discourage new investment? Or will better public services make Scotland more attractive for businesses and individuals to locate here?

No-one yet has the definitive answer to any of these questions. But there is a concern that the actual revenue raising potential – particularly for policies that impact on the highest earners – might be a lot lower than these static simulations suggest. Even in the UK there is uncertainty – the IFS have for example estimated that it is entirely plausible that raising the Additional Rate to 50p in the UK could either raise £1 or £2 billion of revenue or cost £1 or £2 billion of revenue.

Is the debate we are having the right one?

The debate thus far appears to be driven by whether or not income tax should rise and by how much.

But it is important to also consider the wider context.

The options paper that the Scottish Government will publish needs to go further than simply listing the different ways in which income tax can raise revenue.

Firstly, it needs to make the case that raising tax is preferable to savings in other areas. Many people may agree that raising income tax is desirable if it funds greater investment in the NHS or education. But is that preferable to trimming the concessionary travel budget, being less generous on the small business bonus or cancelling the planned cuts to Air Passenger Duty? Might replacing Council Tax with a more efficient local tax system raise more revenue and be less damaging to the economy? Whatever your views, it is important to frame any tax options in terms of the full ‘opportunity cost’ of a decision to raise tax.

Secondly, what happens next year and the year after? We know that, with an ageing population, many funding pressures are likely to only increase in the years ahead. What is the plan for the medium term trajectory for taxation and the sustainability of Scotland’s finances? And what is our strategy for the areas that are going to be squeezed?

Thirdly, what are the implications for the Scottish economy from any tax change? Like it or not, the Fiscal Framework revolves around our relative economic performance. If we grow more quickly than rUK then we retain the additional revenues, if we grow more slowly we lose revenues. With our economy currently growing at around 1/3 the rate of the UK, the Scottish Government will no doubt be nervous about any tax policy that could make closing that growth differential more difficult. In this regard, it would appear to make sense for the Scottish Government to publish an economic assessment of any planned major change in tax policy.

Finally, as ICAS argued in Chapter 2 of our Scotland’s Budget report, there is a strong case – whatever the level of revenue raised – for keeping the tax system as straightforward and transparent as possible. The more complex it becomes, the more inefficient it is.

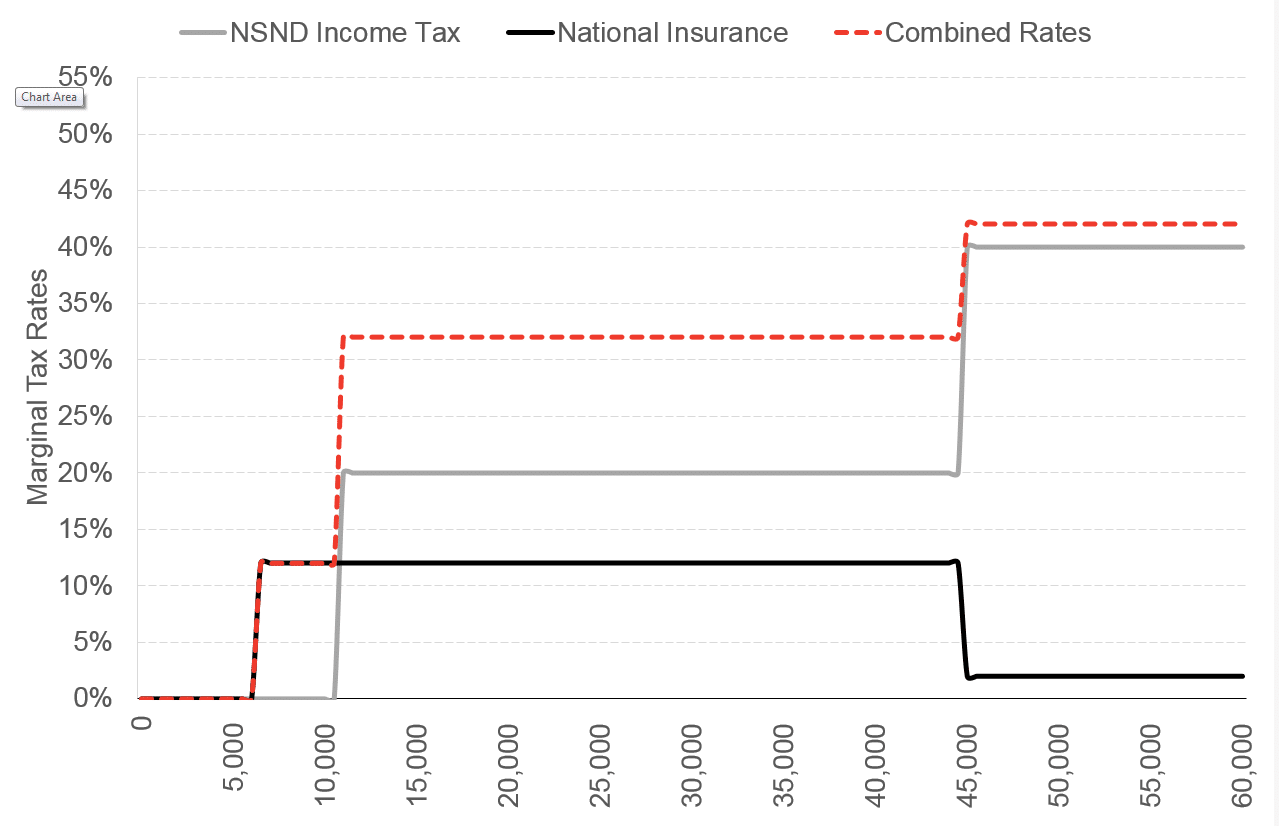

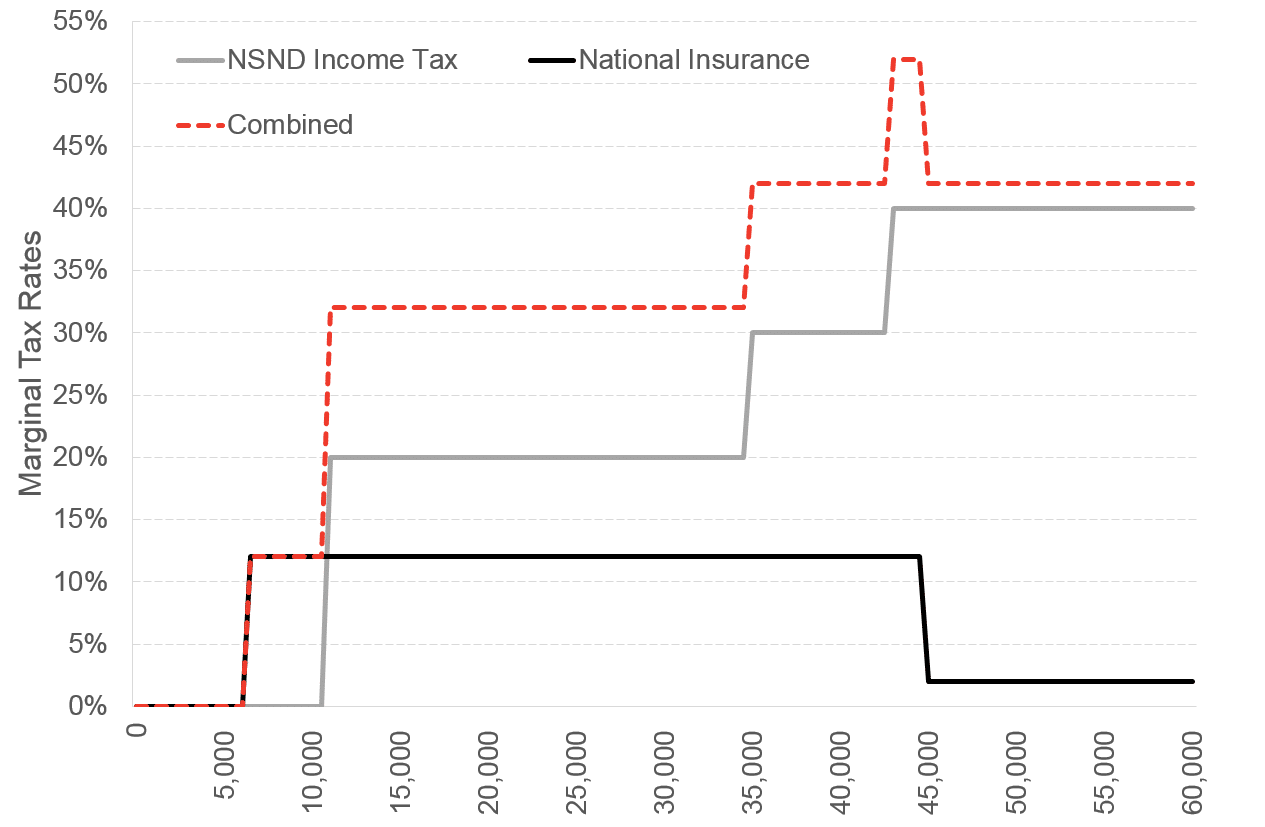

Some of this can arise from unintended consequences, such as the link between devolved and reserved taxes. For example, for income tax and national insurance we already have the situation of some Scottish taxpayers – those in between the Scottish higher rate threshold of £43,000 and the current UK rate of £45,000 – facing a marginal tax rate of 52%.

As the charts highlight, this would only become more complex if a 30p rate was to be introduced for example.

Chart 1: Current UK marginal tax rates by income level

Chart 2: Scottish marginal tax rates by income level (including a new 30p rate & Scottish-specific higher rate threshold)

Final thoughts

All of this is not to argue against using the Parliament’s income tax powers. However, the debate needs to be much broader than simply a discussion of how much revenue can be raised in one year in isolation.

The upcoming budget debate is an important opportunity for policymakers from all sides to set out what they would do, yes on taxation, but also on expenditure and growth.

The new income tax powers provide some measure of relief, but it’s far from the only game in town.

Authors

The Fraser of Allander Institute (FAI) is a leading economy research institute based in the Department of Economics at the University of Strathclyde, Glasgow.