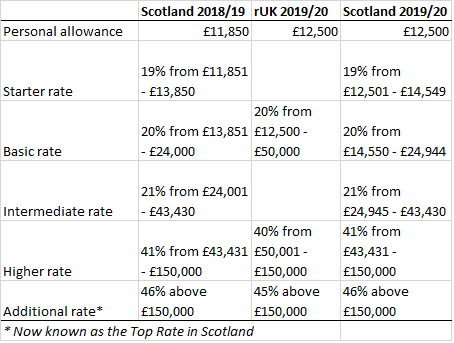

This afternoon, Mr Mackay set out the proposed income tax parameters for 2019/20 in the draft Budget.

These are shown in the table at the bottom of this blog, together with last year’s policy and the 2019/20 UK policy.

Mr MacKay said that 99% of Scottish income taxpayers will pay less tax in 2019/20 than they did in 2018/19.

This statement is correct in the sense that, in 2019/20, 99% of taxpayers will benefit from a higher tax-free personal allowance**, (and to a lesser extent the Scottish Government’s increase in the thresholds for the basic and intermediate rates).

What about comparisons with the rest of the UK? Mr Mackay pointed out that 55% of Scottish taxpayers will pay less income tax than rUK taxpayers with equivalent income.

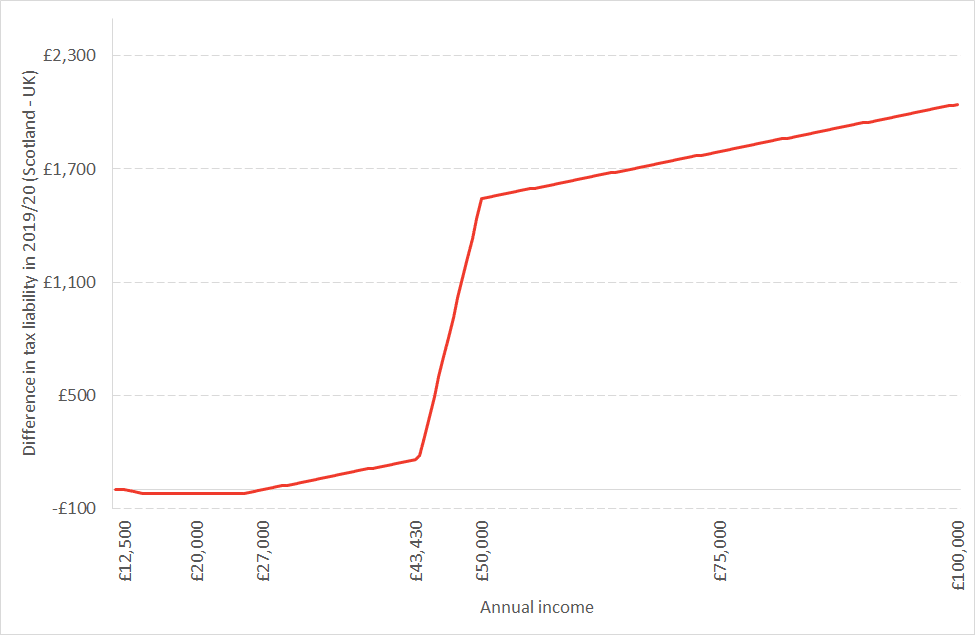

This is true in that the 19% Starter Rate in Scotland means that those with income less than £27,000 (slightly above the Scottish median income) will pay less tax than rUK counterparts.

It is worth bearing in mind however that the difference between Scottish and rUK tax liabilities at this end of the income distribution is small – the maximum benefit to Scottish income taxpayers is just over £20 per year.

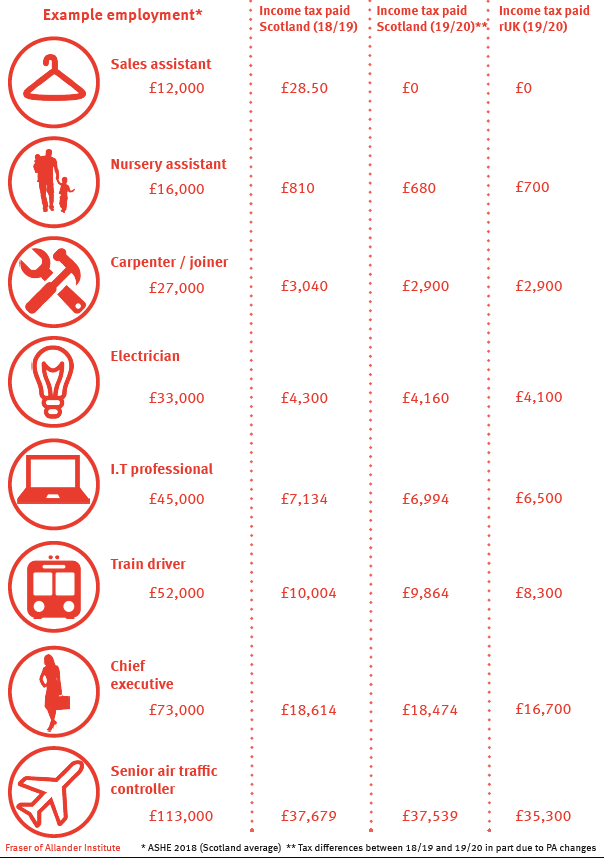

Some examples of the difference in liabilities for different salaries are given in the diagram below.

At incomes above £27,000, Scottish income taxpayers will face higher tax liabilities than those in rUK.

At an income of £40,000, Scottish taxpayers face additional liabilities of £130.

As a percentage of income, the difference is highest at an income of £50,000, when Scottish taxpayers will face liabilities of £1,544 more than those in rUK (3% of income).

Those earning £100,000 will face additional liabilities of £2,044 (2% of income).

Chart 1: Difference in income tax liability between Scotland and rUK in 2019/20

Of course the Scottish tax policy has important revenue raising implications. We estimate that the Scottish income tax policy raises approximately around £550 million in revenue compared to a policy to set the same tax parameters as in the UK.

The Scottish tax policy also has distributional consequences at a household level – which we will consider in our event this Friday.

Table 1. Thresholds and rates in Scotland and rUK

———————————

** The 1% of Scottish taxpayers who will pay more tax than in 2018/19 are from those who earn more than £124,000. The Personal Allowance is tapered away from those earning more than £100,000 at 50p in the pound and taxed at the higher rate. This means that someone with an income of £125,000 for example has no personal allowance. Such an individual will pay higher rate tax (41%) not just on the £106,570 band of income from £43,430 to £125,000, but also on the £12,500 of personal allowance that has been tapered away – so effectively on £119,070 of income. The effect of the Personal Allowance increasing whilst the Higher Rate threshold remains fixed is thus to expose these individuals to a greater band of income that is taxed at the higher rate.

Authors

David Eiser

David is Senior Knowledge Exchange Fellow at the Fraser of Allander Institute

Graeme Roy

Dean of External Engagement in the College of Social Sciences at Glasgow University and previously director of the Fraser of Allander Institute.

Head of Research at the Fraser of Allander Institute