Julia Darby & Graeme Roy

Fraser of Allander Institute and Department of Economics, University of Strathclyde

One of the interesting features of referendums is that they are often motivated by the desire to resolve big debates or settle issues of strong divergent views.

Unlike countries such as Switzerland where referendums are commonplace, in the UK they are much less frequent (although like buses, you wait ages for one to come along and then three – the Alternative Vote referendum in 2011, the Scottish independence referendum in 2014 and the EU referendum in 2016 – come along in close order!)

One consequence can be a rise in economic uncertainty.

Recent levels of economic policy uncertainty and financial volatility

Higher levels of uncertainty can be more likely when the economic and political stakes are high. The effects are also likely to be strongest when the outcome is in the balance – as was the case during the Scottish independence and EU referendums (opinion polls put both sides within sight of victory).

In a world of 24hr news coverage, it is now much more likely that every scrap of information – both credible and more speculative – is shared across a wider number of people.

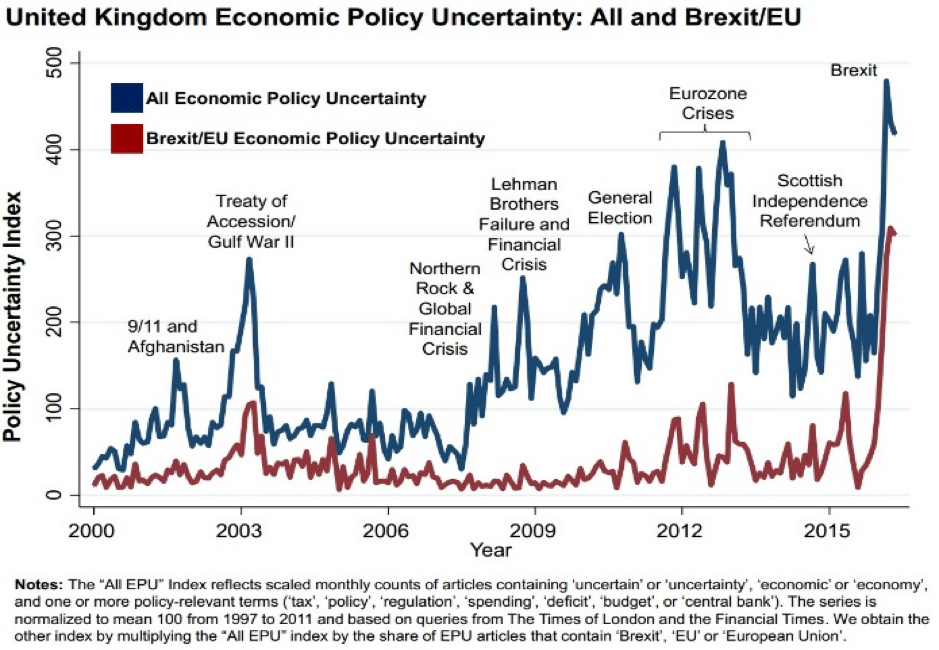

This was evident in the recent EU referendum as highlighted in this chart from the team at www.politicaluncertainty.com. Their measure of economic policy uncertainty is based upon counts of newspaper articles containing specific words, as indicated in the note under the chart.

A referendum is a great natural experiment for testing different hypotheses for how and when markets react to major political and/or constitutional events.

There are a number of other ways to measure uncertainty, including evidence from business or consumer surveys, measures of financial market volatility and measures based on changes in the predictability of economic activity over time.

In recent months, we’ve been tracking how financial markets performed both in the run up to, and immediately after, the Scottish independence referendum. These results remain exploratory, but they are nevertheless interesting and worthy of further research.

To be clear, our analysis isn’t an attempt to assess whether or not Scottish independence is a good or bad thing. Nor does it reveal that. Instead it is simply designed to examine the impact of the referendum itself on short-term financial market volatility.

Of course, the outcome of a referendum can have more fundamental and sustained impacts on financial returns – both positive and negative – but that is beyond the scope of this exercise.

Financial market volatility itself can carry costs for firms (and ultimately the national economy) – for example, if it impacts on lenders’ risk assessments. But this matters less if any heightened volatility is short lived. If this volatility is driven by – or itself drives additional uncertainty – then this may have its own costs. But again, if it is short-lived then a lot of the impacts will simply be displaced activity that will come again in the future.

What have we done?

We have identified companies headquartered in Scotland whose shares are listed on the London Stock Exchange during the period January 2011 to December 2015.

Using share price and market capitalisation data for each of these companies we have constructed a capitalisation weighted Scottish stock price index.

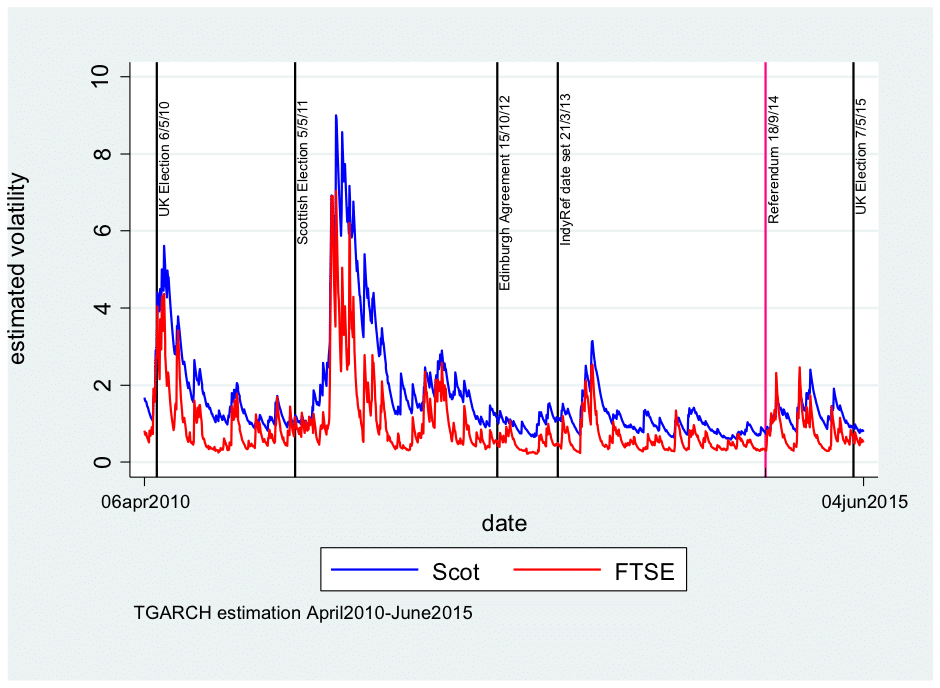

We then calculated stock returns (the daily percentage change in the Scottish stock price index) and used various technical methods – a range of multivariate and univariate GARCH models – to model and compare the conditional volatility of Scottish stock returns on the one hand and stock returns for the FTSE all share index on the other.

For the Scottish series, we undertook some sensitivity analysis – e.g. looking at the importance of individual sectors/companies to the overall results. We find, unsurprisingly that the inclusion/exclusion of RBS has some influence on the overall results (more of that below).

What do we find?

Looking at the volatility of the series as a whole, we find that both the Scottish data and the FTSE tend to be highly correlated with each other. This is unsurprising. Most listed companies operate in global markets and are impacted by the same issues – e.g. swings in stock market sentiment in Wall Street. Similarly, given the close linkages between the Scottish and rUK economies, the economic outlook for the UK will be highly correlated with the economic outlook for Scotland.

We also find however, that the Scottish series tends to be slightly more volatile – i.e. the blue line (measuring volatility in the Scottish series) lies above the red line (measuring volatility in the FTSE). In plotting the timing of the referendum on the graph below, we see that overall the absolute level of volatility – as measured by the methodology set out above – was actually relatively low in comparison to some other periods between 2010 – 2015. For example, the European debt crisis of 2011 can be clearly identified in the chart as can the political uncertainty following the UK election in 2010.

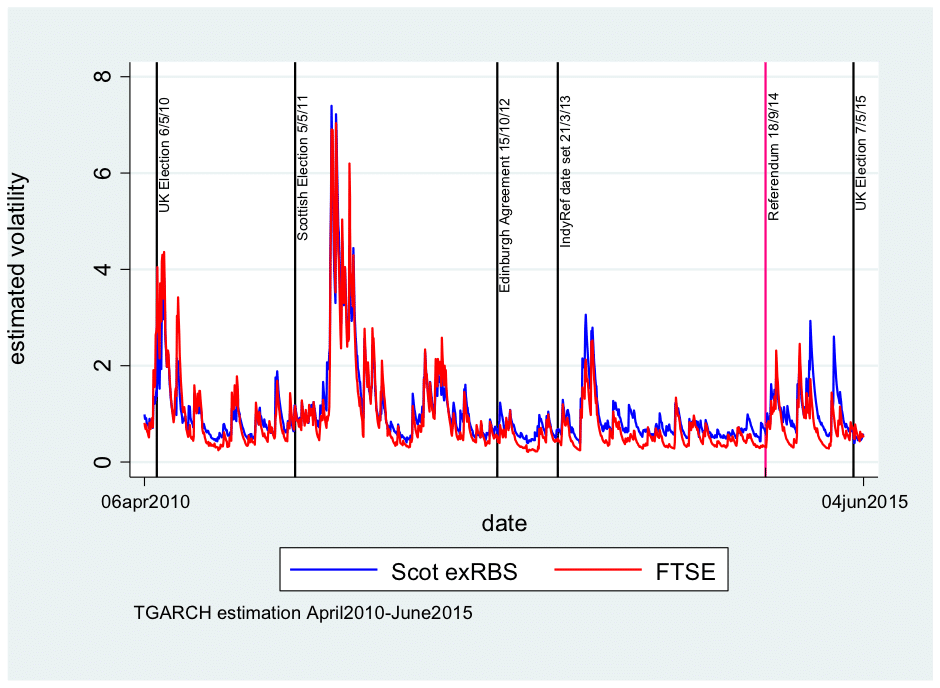

As mentioned above, the results are sensitive to the inclusion of RBS –RBS share prices makes up a large part of the Scottish series givens its sheer scale. [As an aside, not only is the size of RBS an important issue but there is also a question around understanding changes in the RBS share price on any given day during this time. In the years studied, there were regular debates about whether the government would or would not begin to sell its stake in the bank. These will have had their own unique impact on the RBS share price.]

Looking at the volatility of the Scottish series that excludes RBS some interesting features are noticeable.

Firstly, the measured volatility of the Scottish and FTSE indices is now broadly the same for the first part of the sample (i.e. the blue and red lines are very close to each other). In fact, up until the end of November 2013, we find that, from a formal statistical point of view, the volatility of the UK and Scottish stock returns can be described by the same process.

However, we find a statistical significant difference in the conditional volatilities of the two series after this point. That is, the balance of probability suggests that the differences that emerge in Scottish and UK stock market volatility are not due to chance. The Scottish series tends to be more volatile than the FTSE in the period running up to the referendum and beyond.

Simply eyeballing the estimated volatilities of the entire series can only reveal so much.

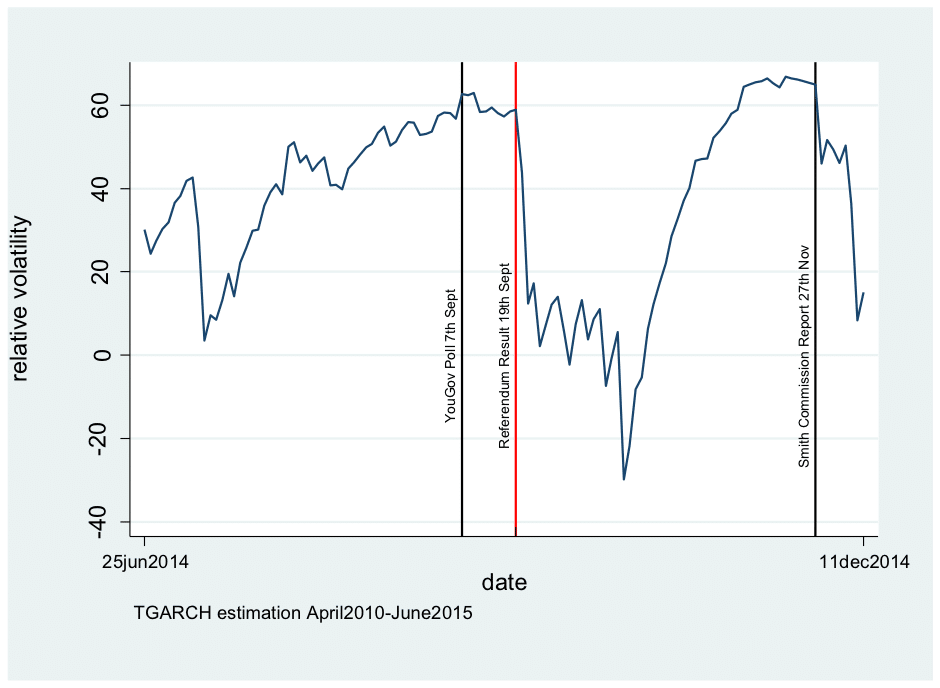

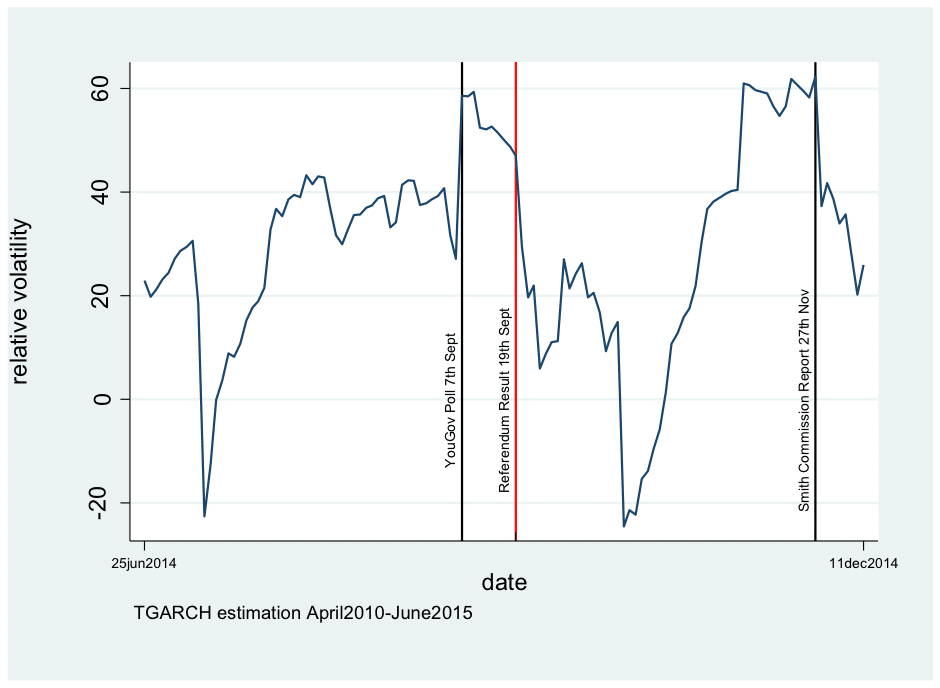

It is possible to zoom in on the referendum period itself and to compare the relative measures of volatility – i.e. a positive number means that the estimated level of volatility is higher in the Scottish series whilst a negative number suggests greater volatility in the FTSE overall.

The chart below shows that there was a marginal rise in the level of volatility in the Scottish series (including RBS) vis-à-vis the FTSE in the immediate run up to the poll. This receded immediately after the referendum but rose again shortly after.

These trends are more evident when RBS is excluded from the analysis. The rise in relative volatility is sharper before falling back in the immediate aftermath. On this sample you can see more clearly the impact of the Sunday Times poll that had the Yes side in the lead.

So overall, what do we conclude?

When RBS is excluded from the series, we find that whilst the volatility of Scottish and FTSE stock returns tend to track one another relatively closely in the run up to the 2014 referendum, the relative volatility of Scottish stock returns increased at the margin.

There is some evidence of a correlation between the referendum – and indeed even the Smith Commission process – and the relative volatility in Scottish stocks.

But, when this relative difference is put in context of overall measures of volatility, the independence referendum does not appear to have been a major driver of volatility of either the FTSE or Scottish series compared to other events around this time. We find that global events – such as the Eurozone debt crisis – tended to have a much more significant impact.

Whether or not this was because firms had clearly articulated contingency plans, or that they were less concerned by constitutional change compared to other factors cannot be backed out from this analysis. But it’s an interesting result nonetheless and one that we’ll return to in future research.

Authors

The Fraser of Allander Institute (FAI) is a leading economy research institute based in the Department of Economics at the University of Strathclyde, Glasgow.