Yesterday’s GDP figures show that the Scottish economy grew by just 0.2%, continuing the weak growth performance we have seen over the last 2½ years.

In this blog, we pick out some of the key points from the data.

Growth continues but remains exceptionally fragile

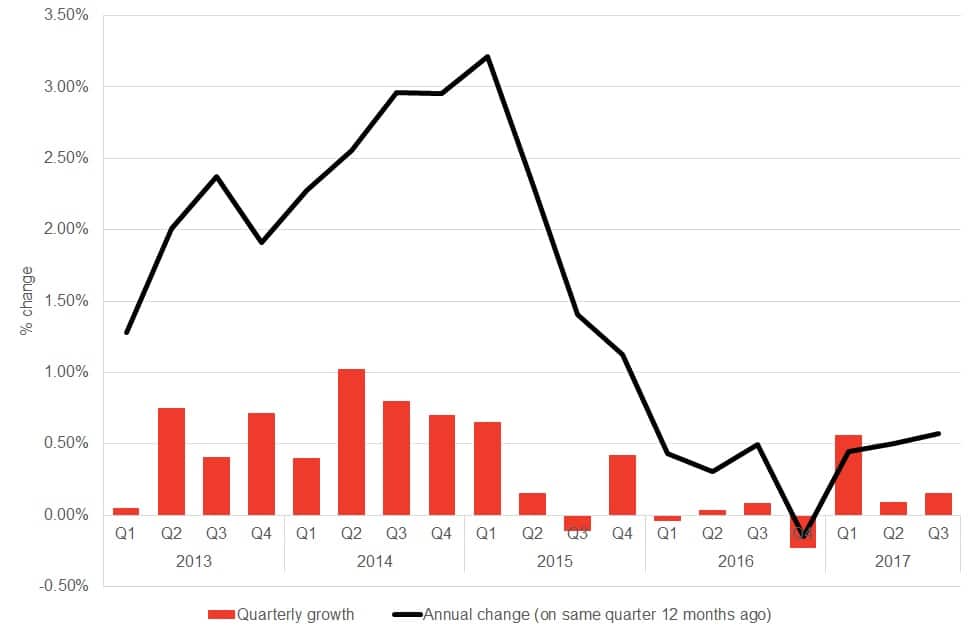

Yesterday’s aggregate GDP growth figure of +0.2% for the three months to September, is well below Scotland’s long-term rate of growth. Indeed it was a whisker away from being even lower, with the unrounded figures showing an increase of +0.15%.

Over the year, growth was 0.6% compared to UK growth of 1.7%.

Chart 1 Annual and quarterly Scottish GDP growth since 2013

Production grew 1.2% over the quarter, driven by very strong growth in the electricity and gas supply sector but also sustained growth in manufacturing.

Output in the electricity sector was up by 8% over the quarter. On its own, this increase contributed +0.2% to Scotland’s overall GDP figure – i.e. equivalent to the entire net growth in the aggregate economy for the quarter!

Given its volatility, it is perhaps more interesting to look at this sector over time. One positive result is that the sector is now reporting levels of output higher than before Longannet was switched off in March 2016.

Services grew by a relatively modest +0.2%, with most sectors showing weak – but positive – growth (with the exception of financial and insurance activities).

Construction output fell once more, down nearly 3% over the quarter (and 7½% over the year). More of this below.

Data revisions to GDP per capita

Yesterday also saw the publication of revisions to some of the data. In particular, there were some downward revisions to the GDP per capita series for Scotland.

GDP per capita is interesting as it provides a useful measure of relative economic performance that adjusts for changes in population growth.

Where there are differences between two countries because of substantially different structural changes in population – e.g. as has been the case (and projected to continue to be the case) between Scotland and the UK – it can provide a helpful picture of the underlying strength of the local economy.

As we have discussed, GDP per capita is also vitally important for the operation of the new Fiscal Framework to the extent that tax receipts per capita are correlated with GDP per capita over the long-term.

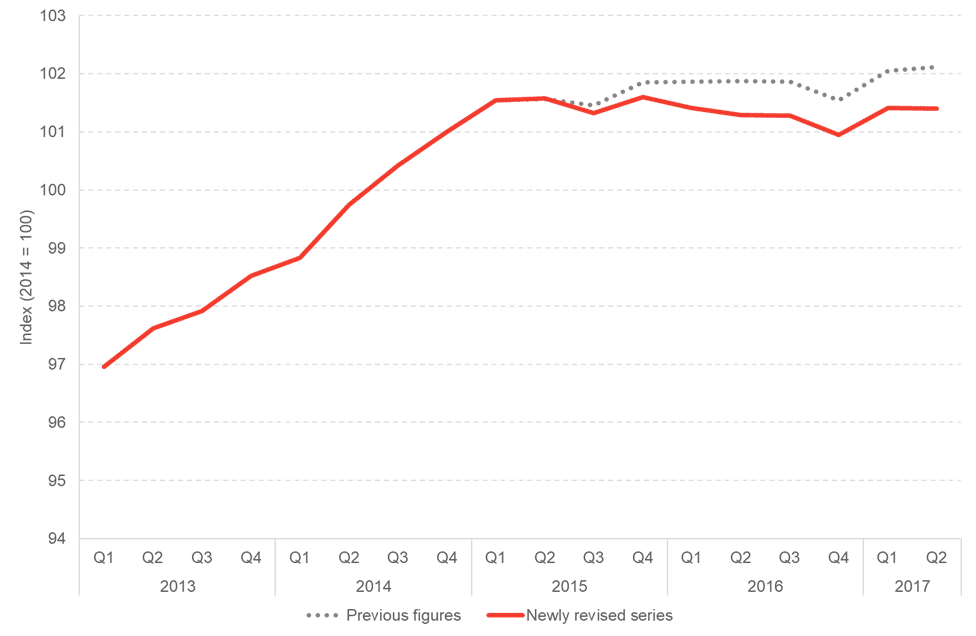

Chart 2 shows the time path of GDP per capita since 2013. We see that the statisticians have revised down growth in the Scottish series from early 2015 ever so slightly.

Whilst relatively small in the context of history, the revised figures now suggest that since 2015 – when the current slowdown in the Scottish economy started – whilst overall GDP has grown by a mere 1.1%, GDP per head has actually fallen by 0.1%. This flat lining in the economy over a sustained period is worrying.

Chart 2 GDP per capita – before and after today’s revisions

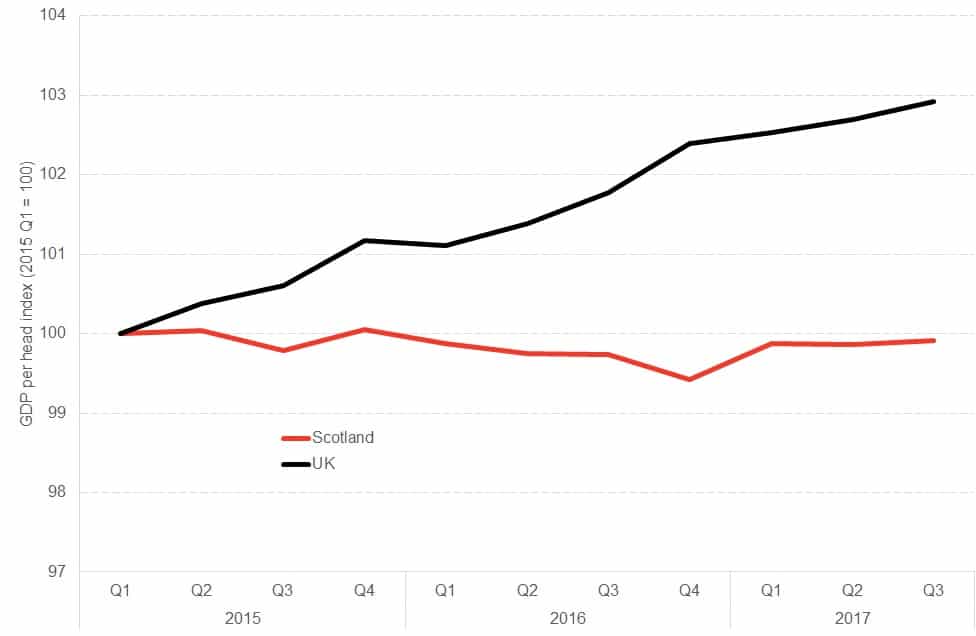

UK GDP per capita performance in recent years has also been weak. However, as Chart 3 highlights a gap has emerged between Scotland and the UK. It is now wider after these revisions.

Chart 3 GDP per capita Scotland and the UK since 2015

Of course, whether or not GDP and GDP per capita are perfect measures of economic performance is open to debate. They certainly do not provide a robust measure of wellbeing, prosperity or sustainability. But they do provide a useful proxy for overall activity in an economy. And given the importance of relative economic performance per head with the UK for the new Fiscal Framework, closing this gap in the years ahead will be important.

What explains these recent trends?

The downturn in the oil and gas sector has been frequently identified as the key reason for the slowdown in the Scottish economy in recent times, particularly relative to the UK.

Since the fall in the oil price in late 2014/2015, sectors tied to the North Sea supply chain – most notably in manufacturing – have been badly affected. However, we have started to see a stabilisation in many of these sectors more recently. Manufacturing rose 0.4% this quarter and by 2.9% over the year.

Table 1 Growth in manufacturing over last 12 months

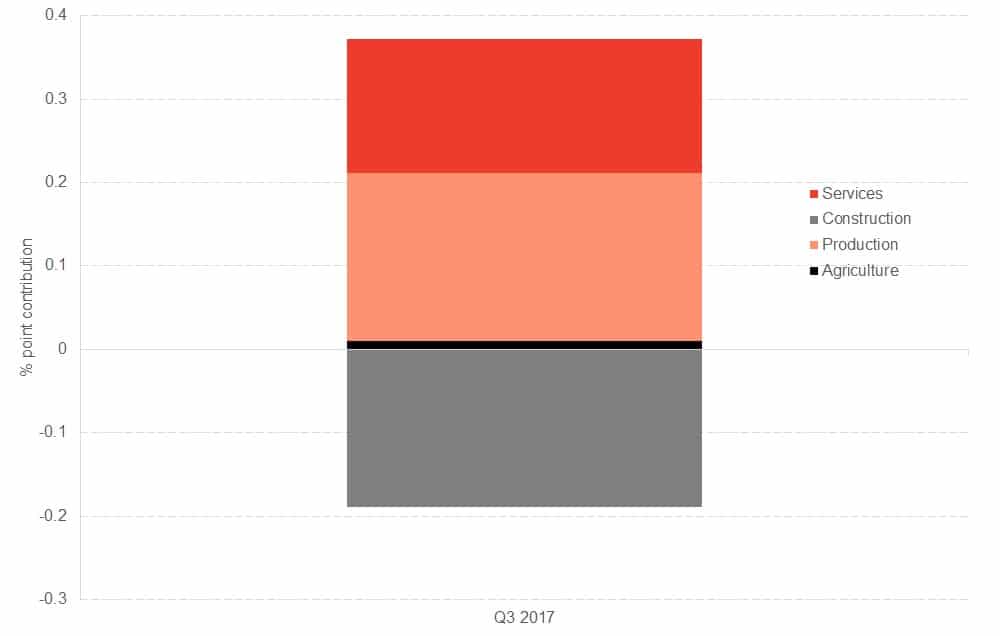

In more recent quarters, the biggest drag on the Scottish GDP numbers has not been sectors directly tied to the oil and gas supply chain but construction.

As Chart 4 highlights, construction knocked around 0.2% off the overall change in Scottish GDP in Q3 2017. Without that, the Scottish economy would have actually been close to trend.

Chart 4 Contribution to GDP growth by sector Q3 2017

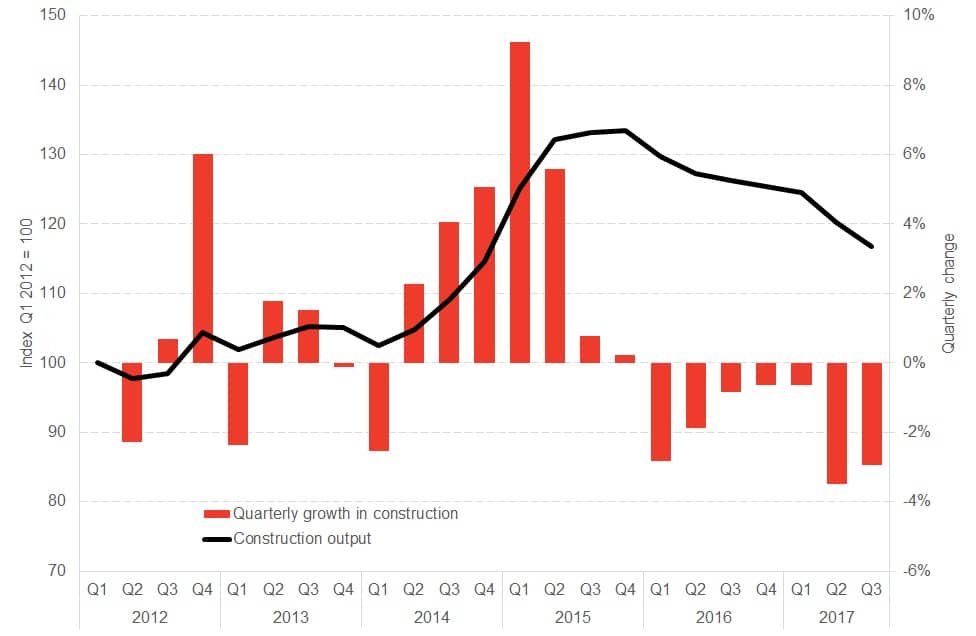

This is not a one-off. Output in the construction sector has been falling now for 7 consecutive quarters.

The Scottish construction series has been displaying some rather odd characteristics in recent times.

As Chart 5 highlights, there was very strong growth during the tail end of 2014 and early 2015. Over a two year period, construction output was estimated to have grown by 30%!!

Since then, we have seen falling output as the series adjusts to more normal levels.

Chart 5 Construction sector performance in Scotland since 2012

Scottish Government statisticians believe that the sharp increase in the series was driven by ”large transport and industrial infrastructure developments such as the Forth Replacement Crossing, Borders railway, M8 missing link and the Shetland Gas Plant.” The downturn has come as these projects have ended.

The underlying data from the ONS on output in the construction sector backs this up, with a spike in infrastructure spending in 2014 and 2015. There has also – in recent times – been a decline in private commercial construction.

But this still seems somewhat odd. Whilst it is the case that there have been number of major public infrastructure projects in Scotland in recent times, the overall capital budget of the Scottish Government has been rising so the public sector is still investing in infrastructure (perhaps not just very large and visible projects).

We suspect therefore that some of the changes we have seen in construction in recent times reflects the way in which activity is measured.

Once the series returns to trend, we should start to series more ‘normal’ patterns of growth.

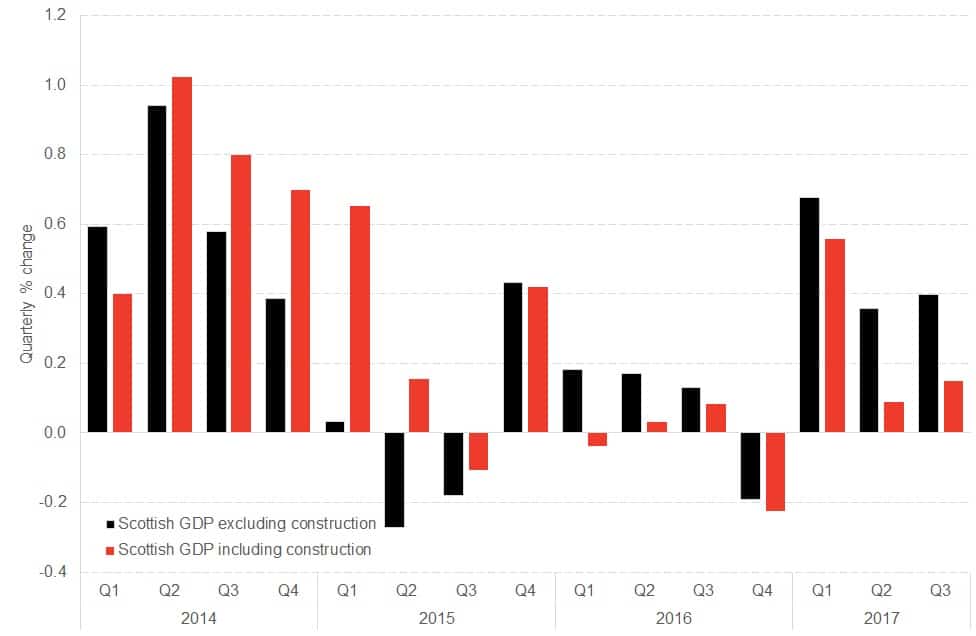

In the meantime, the volatility in the construction series is having a significant impact on aggregate Scottish GDP.

To illustrate this, in Chart 6 we strip out from the aggregate Scottish GDP figure the impact of construction.

Chart 6 Scottish GDP since sharp rise in construction in 2014 – aggregate GDP with and without construction sector series

The chart shows that the time path of Scottish GDP looks quite different when the impact of construction is removed from the series. Firstly, growth in 2014 and 2015 would have been much lower than reported. For example, in Q1 2015 reported growth was 0.7% but virtually all of that came from construction.

Secondly, and perhaps of most interest, is that the recent performance of the Scottish economy has not been as bad as the aggregate figure suggests once the impact of construction has been removed. In particular, 2017 growth would have been closer to trend.

Clearly construction is an important sector in the economy and this is not to downplay its role or the challenges that it faces. However, given the somewhat surprising pattern of growth in the statistical series in recent years, it suggests once again that some caution is needed when interpreting key trends (and the sources of underlying growth/weakness in the Scottish economy).

So how do today’s numbers stack up against forecasts?

Firstly, our nowcasts projected slightly stronger growth between 0.3% to 0.4% for Q3 2017. But as pointed out above, removing construction from the series suggests that our nowcasts – which track overall growth in the economy rather than specific sectors – were pretty accurate.

Secondly, the Scottish Fiscal Commission published a quarterly estimate for Scottish GDP back in December. Back then, they forecast growth of +0.14% – remarkably close to today’s figure of +0.15%!! Not bad for their first forecast evaluation!!

Today’s figures are part of an increasingly consistent pattern – from unofficial sources like our nowcasts and business surveys and from official sources – that whilst the Scottish economy continues to grow, it does so at a fragile pace.

Next week we will get labour market data and we await to see if the relative weak growth will have any impact on the near record levels of employment that have been a feature of the Scottish economy in recent times.

Authors

The Fraser of Allander Institute (FAI) is a leading economy research institute based in the Department of Economics at the University of Strathclyde, Glasgow.