The price of a barrel of oil has been rising steadily in recent months.

Whilst prices have slipped back a little – in the light of OPEC’s apparent plan to relax their recent self-imposed constraints on supply – oil prices continue to hover close to their highest level in three years.

The recent increase has helped to provide a boost for contractors and operators in the North Sea.

You may have missed it over the last few days following the publication of a couple of other economic reports, but late last month we published the latest set of results in our joint survey with Aberdeen and Grampian Chamber of Commerce – sponsored by KPMG – which showed further signs of returning optimism in the sector.

In this blog, we discuss some of the key results and their potential implications for the wider Scottish economy and the growth outlook for 2018.

Oil prices and activity in the North Sea

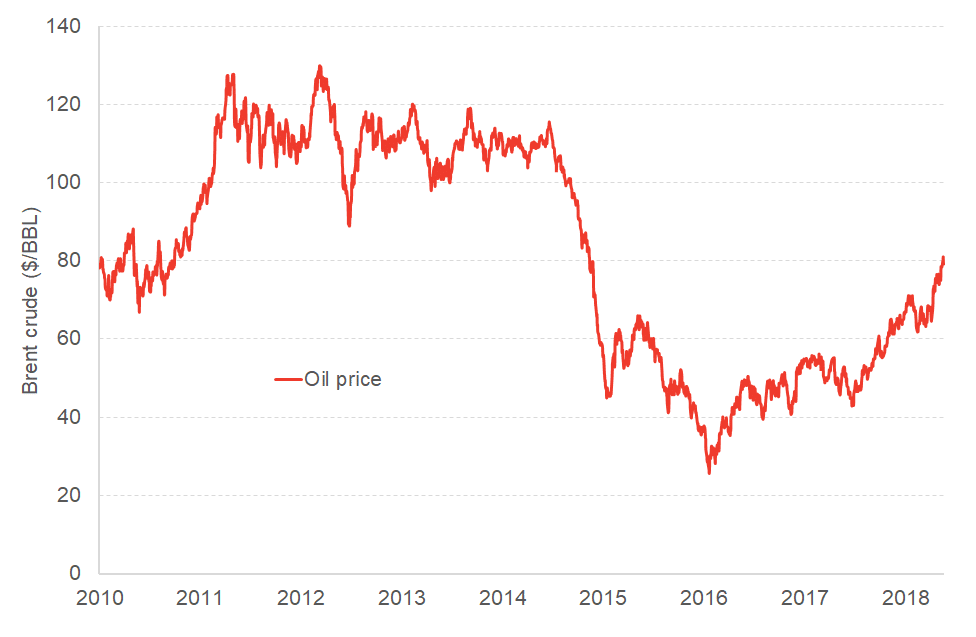

As has been well documented, oil prices fell from between $110 and $120 during 2011-2014 to around $25 a barrel in early 2016.

Brent crude spot prices – 2010 to 2018 Source: Thomson-Reuters Datastream

Source: Thomson-Reuters Datastream

Since then – and particularly late 2017 – prices have been rising back to close to $80 (up around 50% over the year).

All this comes at a time when production in the Scottish part of the North Sea has been on a slightly upward trend.

Oil and gas production in Scottish sector of UKCS

Source: Scottish Government

Oil and gas production in the UKCS peaked in 1999 and has been falling relatively steadily since. But over the last couple of years, driven in part by record investment levels, production has been back on the rise. Most forecasts are for production to remain on the upside for the next couple of years.

Trends in wider North Sea activity

Arguably the most important element for the day-to-day Scottish economy is not the amount of production in the North Sea. Instead, it’s i) the amount of income that this activity is generating for the people working in the sector and, ii) demand levels in the associated supply chain.

The sharp fall in the oil price led to a major cost-cutting exercise in the North Sea. Oil and Gas UK estimate that average unit operating costs have fallen from around $29.6 per barrel of oil equivalent in 2014 to just $15.2 in 2017.

In 2016, capital investment – including in exploration and appraisal – was just over half that in 2014.

These dramatic cost-cutting and efficiency measures – coupled with reforms to the fiscal and regulatory environment – has led to a sector that is leaner and more competitive.

But it has also undoubtedly had a spill-over effect into the Scottish economy, with lower wages and significant job losses.

Estimated UK jobs supported by oil and gas (includes direct and multiplier impacts)

| 2013 | 2014 | 2015 | 2016 | 2017 | |

| Direct | 36,600 | 41,300 | 37,300 | 29,500 | 28,300 |

| Indirect | 198,100 | 206,100 | 163,100 | 150,600 | 141,900 |

| Induced | 206,200 | 216,500 | 173,400 | 135,300 | 132,000 |

| Total | 440,900 | 463,900 | 373,800 | 315,400 | 302,200 |

Source: Oil and Gas UK Economic Report 2017

As the table highlights, around 160,000 jobs are estimated to have been lost since the downturn. Whilst these figures are for the UK as a whole, a substantial number will have been in Scotland.

The sharp decline in the oil prices has also had a major impact on the onshore supply chain.

Oil and Gas UK estimate that the oil and gas services sector has seen revenues fall by more than £10 billion from 2014 to 2016.

Impact on the Scottish economy

It is no surprise that with such dramatic changes in activity in the North Sea, the Scottish economy has been impacted.

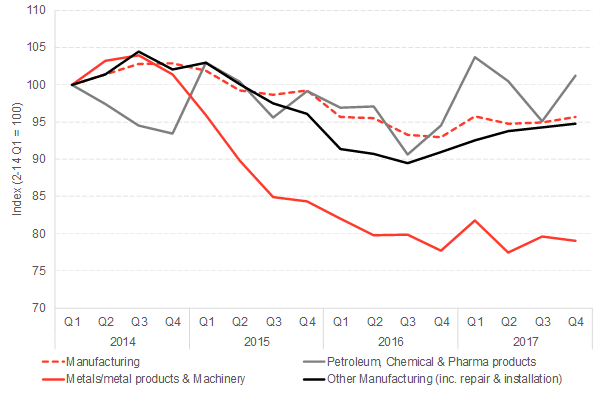

Many of the sectors closely tied to oil and gas saw output full significantly.

Output in manufacturing, metals, petroleum & chemicals and other manufacturing (including repair and maintenance)

Source: Scottish Government

The Scottish Government’s Chief Economist estimated this time last year that the downturn in the oil and gas sector contributed to around 2/3 of the slowdown in the Scottish economy between 2014 and 2016.

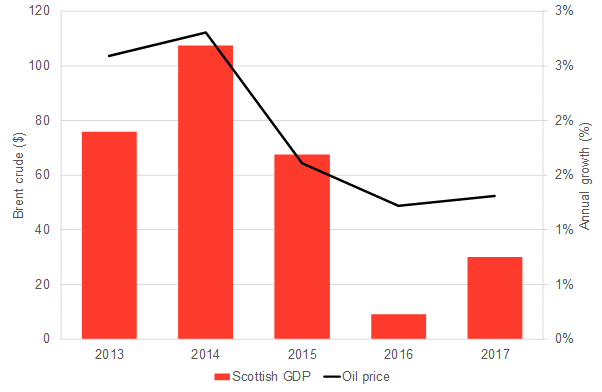

Indeed, the correlation between the oil price and growth in recent times appears strong.

Oil prices and Scottish economic growth

Source: Scottish Government & Thomson Reuters

Source: Scottish Government & Thomson Reuters

But as we discussed in our March Commentary – and will touch on once again in our upcoming commentary next month – the relatively slow growth in the Scottish economy during 2017 appears to stem not from sectors tied to oil and gas but from other parts of the economy (and in particular, construction).

So if activity in the oil and gas industry continues to pick-up then this should help boost growth in 2018.

So what is our latest survey telling us about current activity levels?

Our latest survey

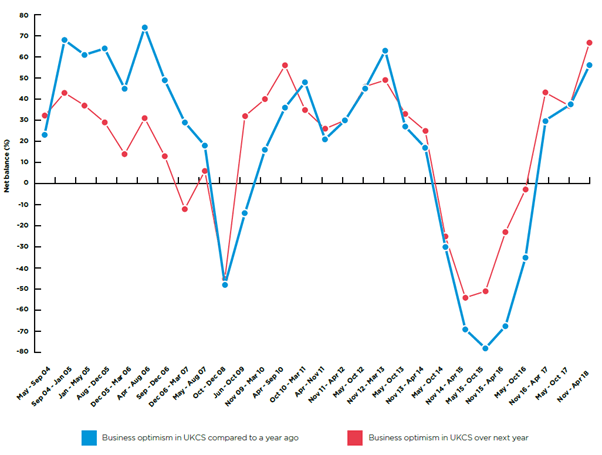

During the six months to April 2018, almost two-thirds of contractors reported being more confident about the current business situation compared to a year ago.

The net balance of 56% is greater than at any other time since spring 2013.

Business confidence amongst contractors in the UK Continental Shelf

Source: FAI/AGCC/KPMG

With 41% of businesses now working at or above optimum levels, 75% of firms forecasting a rise in profits this year and around 70% of firms existing to see a further rise in business optimism in the months to come, the latest information suggests that activity in the North Sea may surprise on the upside this year.

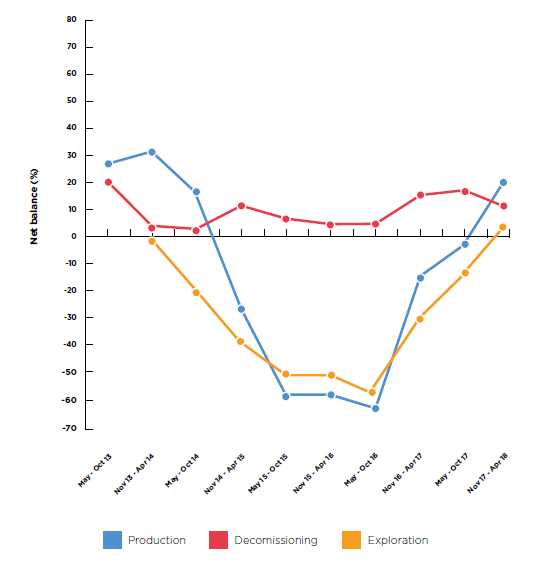

But it’s not all positive. Whilst exploration levels returned to positive territory for the first time since before the downturn, employment continues to fall amongst operators (albeit at a slower pace than in recent surveys).

Net balance of firms key activities

Source: FAI/AGCC/KPMG

Source: FAI/AGCC/KPMG

Taken all together, whilst the sector continues to face significant challenges over the medium to longer term, the immediate outlook for Scotland’s oil and gas sector is more optimistic than it has been for a number of years now.

With that in mind, if this optimism translates into actual activity and higher pay for workers, then the sector should help boost economic growth in Scotland as a whole during 2018.

With UK growth just 0.1% in Q1 of 2018, it would not be unsurprising if – boosted by oil and gas – Scotland’s growth figures for the same period turn out to be stronger. But we’ll have to wait to see what the official statistics are saying when the latest set of data are released at the end of next month.

We will discuss all of this in much more detail when we publish our latest Fraser Economic Commentary – in partnership with Deloitte – on the 20th June.

Authors

The Fraser of Allander Institute (FAI) is a leading economy research institute based in the Department of Economics at the University of Strathclyde, Glasgow.