Grant Allan, Stuart McIntyre, Graeme Roy, Fraser of Allander

This week, statisticians in St Andrew’s House will be busy finalising their best estimate of Q1 2016 Scottish GDP.

In advance of its publication, we offer our prediction of what that estimate might be, and crucially what it will tell us about the state of the Scottish economy.

Recent Performance

GDP figures are usually keenly anticipated, and the ones to be published next week – Wednesday 20th July – will be intriguing for two reasons.

Firstly by covering the period up to March, they will provide an insight into how robust the Scottish economy was prior to the EU referendum debate really taking hold. Perceptions were that much of the UK economy was on pause in the run-up to the vote. The GDP estimate to be released next week will give us an indication of how well placed Scotland was to cope with these headwinds and the uncertainty that has followed the result.

Secondly, they will also reveal the underlying strength of the Scottish economy, the impact of the ongoing challenges in the North Sea, and whether the divergence in the performance of the UK and Scottish economies in 2015 has continued into 2016.

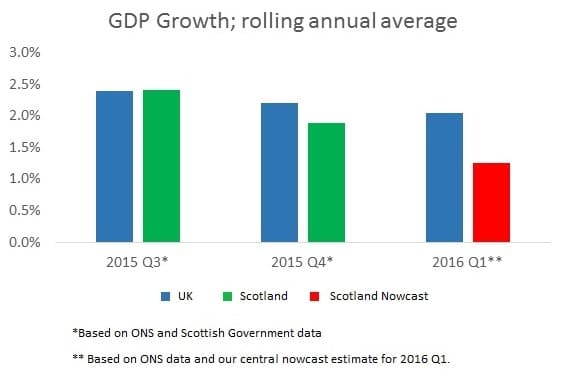

Over the 12 months to the end of December 2015, the Scottish economy grew by just 0.9% compared to 2.1% in the UK. It is also worth noting that Scotland narrowly avoided ‘technical recession’ last year – defined as two consecutive quarters of negative output – with output of just +0.1, -0.1 and +0.1 during the final 9 months of 2015. Without a substantial boost from the construction sector – primarily government infrastructure – it is highly likely that Scotland would have slipped back into recession.

Crucial here will be the continued effect of the low oil price on the North Sea, and in turn its impact on onshore activity, particularly in the North East. Oil and gas is by far Scotland’s largest industrial sector. And although next week’s GDP figures will only cover the onshore economy, they will pick-up the decline within the wider local supply chain. We have for example seen relatively sharp falls in manufacturing and the mining and quarrying sector over the past year. Household spending has also trailed off as a result of lower earnings and rising unemployment.

So the divergence between Scotland and the UK is hardly surprising. But with Holyrood soon to take on greater responsibility for raising its own revenue, it is vital that this performance improves.

What is our best estimate of next week’s figure?

In the Fraser of Allander, we’ve been developing new techniques to provide an accurate ‘nowcast’ of the Scottish economy.

One of the problems with official data is the time lag it takes to publish the latest figures.

There are good reasons why official figures are published with such a lag – for example it takes time to process the large volume of survey data that underpins the estimates. However, in a fast changing environment, such as in the aftermath of the EU referendum, there is an urgent need for much more timely data.

Waiting 3½ months simply isn’t going to work.

A nowcast is a statistical estimate which combines emerging unofficial data on different trends in the economy (e.g. consumer confidence), business survey results (including data that we at the Fraser produce) along with the most current official data (e.g. on employment) to obtain an up-to-date estimate of conditions in the economy.

The aim is to try to provide a much more immediate assessment than can ever be provided by the official data. And it lets us provide an estimate of what we think GDP will be next week.

The chart below shows our forecast for annual growth up to Q1 2016.

Based on our modelling, we think the Scottish economy will continue to avoid recession – just!

Growth will be +0.3% for the quarter compared to +0.5% in the UK. This will actually be slightly faster growth than Q4, but still weak by historical standards. Overall, this would take Scotland’s annual 4Q on 4Q growth to 1.3% vs. UK growth of 2.1%. Experience suggests that our model tends to over-estimate Scottish GDP, and therefore while we expect that growth will be positive, we wouldn’t be surprised if our estimate provides an upper bound on this growth.

Why? The North Sea will clearly continue to have an impact, but we’re also seeing ongoing weaknesses in investment and export information more generally. Consumer confidence remains fragile. Clearly any number of unforeseen things could influence the statistics next week, but our take is that whatever the exact point estimate turns out to be, the conclusion will be that the recovery remains fragile.

The outlook had been improving a little although it certainly won’t have been helped by the uncertainty surrounding Brexit. That’s why there is an urgent need for a robust policy response from policymakers from all sides.

Two Final Things to Watch For

Firstly, next week’s statistics are likely to include relatively large revisions to past data. Every year, the GDP figures go through a major ‘revision’ following publication of the UK Blue Book of National Accounts and the Scottish Supply Use Tables.

These revisions provide updated information on some of the more complex items of GDP to measure and allow the GDP estimates to more accurately capture the structural composition of the Scottish economy by re-weighting the size of sectors. Typically, any revisions usually net out so the overall impact on long-term growth trends is marginal.

However with recent quarterly Scottish GDP numbers very close to 0, small changes could have quite significant implications in interpretation if they were to show that Scotland did actually re-enter recession last year; or indeed that the slowdown hadn’t been as bad as initially thought.

Secondly, next week’s figures will include the final days of Longannet power station, one of the largest coal power stations in Europe. The shut-down will have a significant impact on Scottish GDP in the next quarter (i.e. Q2 2016), taking anything up to 0.4 percentage points off the headline number. A weaker – or even negative – number next week for Q1 compared to our prediction of +0.3% will not bode well for economic performance over the year (and in our view will substantially increase the risk of Scotland re-entering ‘technical recession’ sometime this year).

Authors

Graeme Roy

Dean of External Engagement in the College of Social Sciences at Glasgow University and previously director of the Fraser of Allander Institute.