Over a year has passed since Scotland, and the whole of the UK, entered a national lockdown. Recently the Economics Observatory published a recap of this unprecedented year.

Despite a challenging year, and a long winter, there is finally some optimism. The latest data shows positive signs of the economy gradually gearing up for (hopefully) an expected recovery in economic activity.

With over half of the adult population now vaccinated and the timeline for the easing of restrictions in place, indicators of economic activity and expectations of future output rose in February.

Recent monthly GDP data for Scotland has revealed that the Scottish economy contracted in January following the start of the winter lockdown. But, this fall has been less pronounced than the one experience during the Spring lockdown last year.

The current health and economic crisis makes for a very unusual election campaign. Here at the Fraser we have been publishing regular content surrounding the 2021 Scottish Election. You can keep up with our work here.

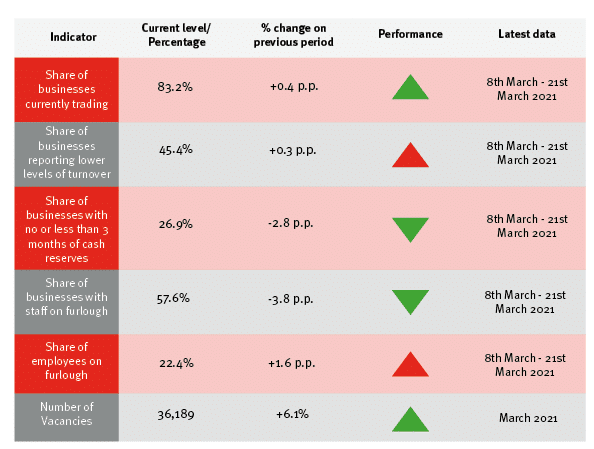

Table 1: Real time indicators dashboard

Source: Scottish Government; Adzuna

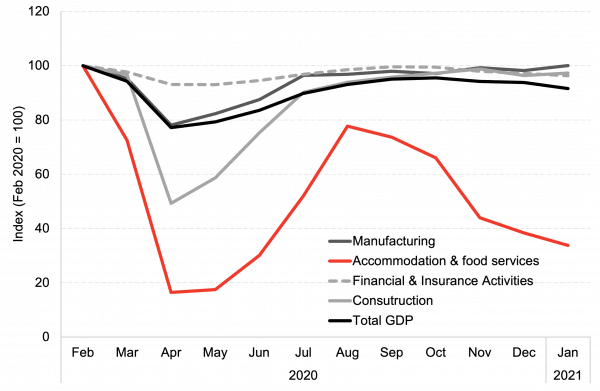

Chart 1: GDP in Scotland, February 2020 – January 2021: Scottish GDP has been more resilient during the winter lockdown compared to the first lockdown in 2020. Total GDP fell by 2.4% in January compared to the previous month. The accommodation & food services sector has been particularly hard hit and experienced a 12% contraction in January. On the other hand, despite being significantly impacted by the first lockdown, construction has proved resilient to subsequent lockdowns.

Source: Scottish Government

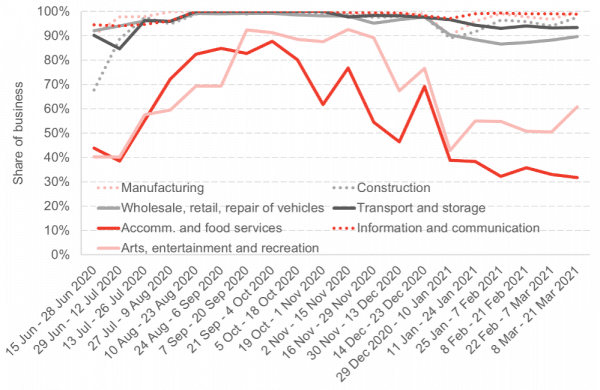

Chart 2: Estimated share of businesses that are currently trading, broken down by industry, 15th June 2020 – 21st March 2021: The share of businesses currently trading in the Scottish economy has improved since the December lockdown. The share of businesses trading in the arts sector improved around mid-march however, the share of trading businesses in the accommodation and food services sector continues to decline.

Source: Scottish Government

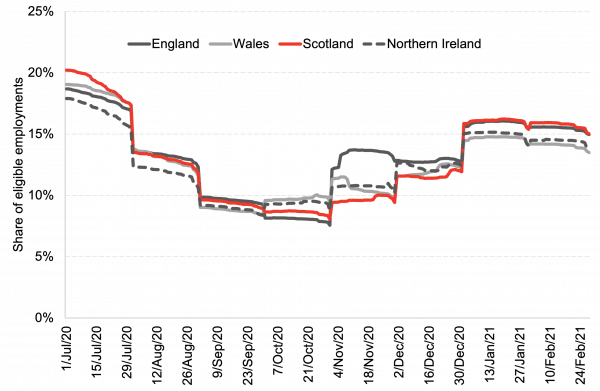

Chart 3: Share of employments on furlough, UK nations, 1st July 2020 – 28th February 2021: The share of employment on furlough has risen during the winter lockdown and was at 15% at the end of February in both Scotland and England. However, the magnitude of furloughing is currently lower compared to the first lockdown in Spring last year.

Source: HMRC

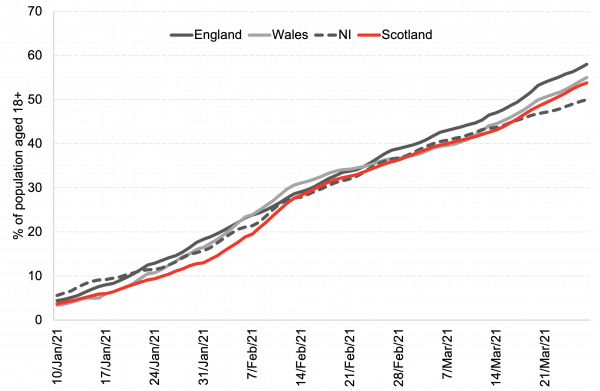

Chart 4: Share of adult population aged 18+ who have received the first dose of the vaccine against Covid-19, UK nations, 10th January 2021 – 27th March 2021: The share of adults who have received their first dose of the COVID-19 vaccine has exceeded 50% across all UK nations. All nations have been delivering vaccines at a similar pace, but the pace picked up in England throughout February and March.

Source: UK Government

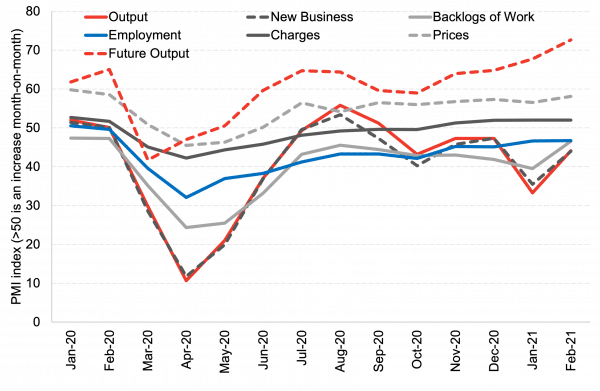

Chart 5: Purchasing Managers Index, Scotland, January 2020 – February 2021: The PMI shows that more companies have been experiencing a contraction in new business, output, employment, and backlogs of work than those who have experienced an increase. However, the number of managers reporting a decline was smaller in February compared to January. On the other hand, expectations of future output has risen to the highest level since the beginning of the pandemic.

Source: IHS Markit

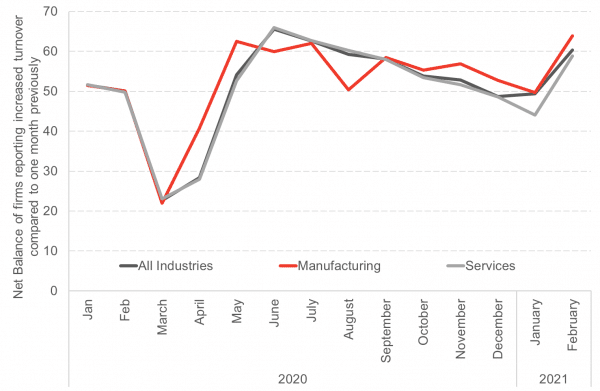

Chart 6: Monthly Business Index – Net Balance of firms reporting increased turnover compared to one month previously, Jan 2020 – Feb 2021: In February the monthly turnover index for all industries was 60.3. The index for manufacturing and services was 63.9 and 58.9 respectively; notable improvements on the month before. The direction of this turnover index does not directly correlate with monthly GDP however, it does show that economic activity picked up in February. Scottish GDP data for February will be published later this month.

Source: Scottish Government

Note on our real-term indicators analysis:

We review newly available data each fortnight and provide a regularly updated snapshot of indicators that can provide information on how the economy and household finances are changing. This allows us to monitor changes in advance of official data on the economy being released and also to capture key trends that will be missed by measures such as GDP. Each fortnight we investigate new sources from known data sources and use publicly available data.

Authors

Ben is an Economist Fellow at the Fraser of Allander Institute working across a number of projects areas. He has a Masters in Economics from the University of Edinburgh, and a degree in Economics from the University of Strathclyde.

His expertise lies in various economic modelling approaches, social care, and evaluating social impact for organisations across the private, public and third sector, particularly where evaluation requires intuitive approaches.

Adam McGeoch

Adam is an Economist Fellow at the FAI who works closely with FAI partners and specialises in business analysis. Adam's research typically involves an assessment of business strategies and policies on economic, societal and environmental impacts. Adam also leads the FAI's quarterly Scottish Business Monitor.

Find out more about Adam.

Frantisek Brocek

Frank graduated from the University of Strathclyde in 2019 with a First-class BA (Hons) degree in Economics. He is currently studying on the Scottish Graduate Programme MSc in Economics at the University of Edinburgh.

He has experience from a variety of economic policy institutions including the European Commission in Brussels, the Slovak Central Bank and the Ministry of Finance.