Official data published in April showed that the Scottish economy contracted in the final 3-months of 2016. That means that we’re just one data release away from ‘technical recession’ – that is, two consecutive quarters of falling GDP.

In this blog, we review the most up to date official and unofficial data to get a sense of how likely it is that we will slip into recession when the figures for Q1 2017 are published in July.

On balance, we think that it is going to be a close run thing.

Recap – Q4 2016

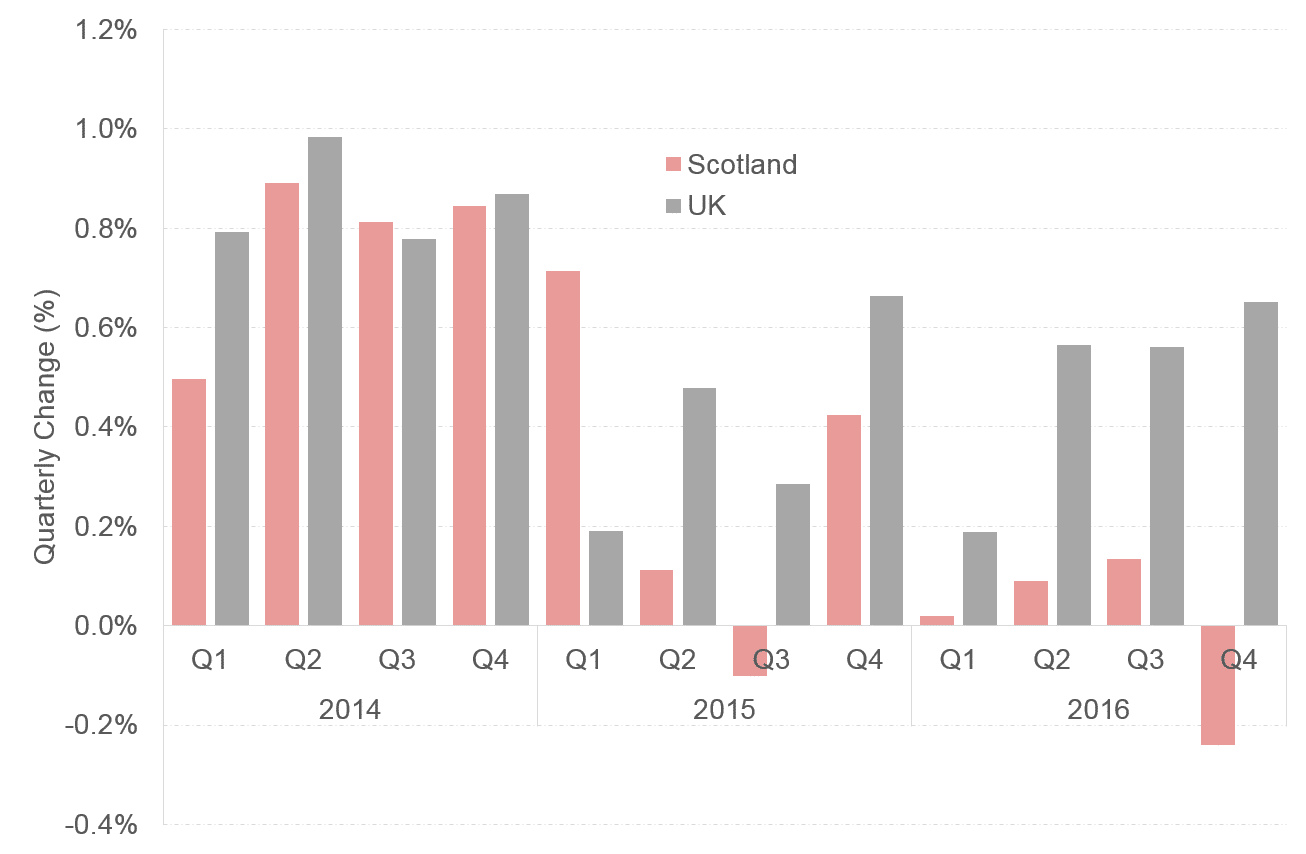

The Scottish economy contracted by 0.2% in the final quarter of 2016.

Source: Scottish Government

The poor figures were pretty comprehensive – both production and construction output fell, whilst the all-important services sector remained flat.

Back in July 2016, we argued that the outlook for the next couple of years was fragile and periods of negative growth were highly possible.

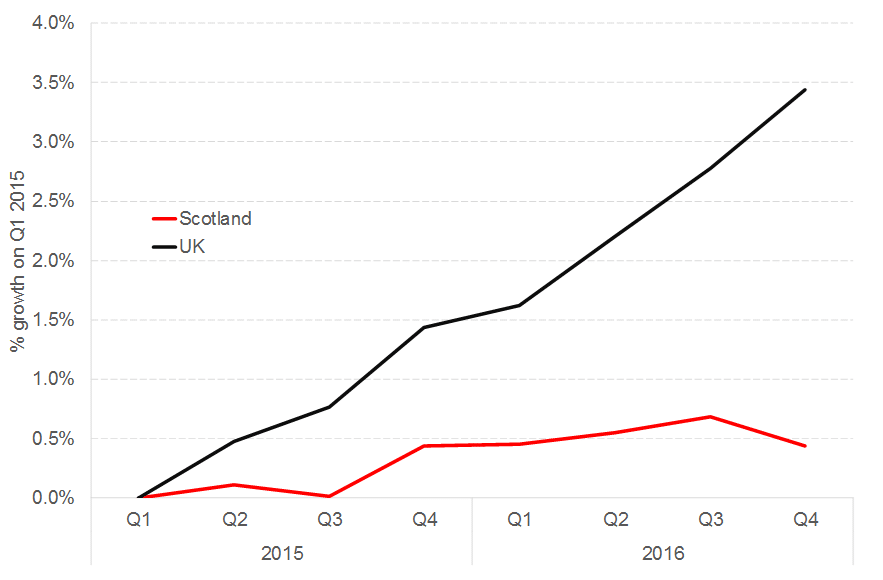

Indeed, between Q4 2015 and Q4 2016, the Scottish economy did not grow at all, compared to growth of 1.9% in the UK.

Economic growth in Scotland has lagged the UK for 2 years now.

Source: Scottish Government

A key driver for this divergence has undoubtedly been the downturn in the North Sea. Whilst North Sea output doesn’t actually enter the Scottish figures (instead it covers the onshore economy only), the supply chain that supports the oil and gas industry does.

But as we discussed last month – Strathclyde Engage Week – there is increasing evidence that this might only be part of the explanation.

For example, whilst engineering firms and makers of specialist machinery and oil and gas support services have been badly hit, every single one of Scotland’s principal manufacturing sectors – from food and drink, textiles, computer and electrical products, through to transport equipment, contracted during 2016.

Services – around 75% of our economy – grew nearly twice as fast in the UK as a whole as they did in Scotland.

It seems unlikely that this is all tied to the North Sea.

So what is the more recent data telling us?

For the official figures for Q1 2017, we will have to wait until early July.

But there’s quite a lot of information out there already that can give us clues to how the economy has performed during the first months of 2017.

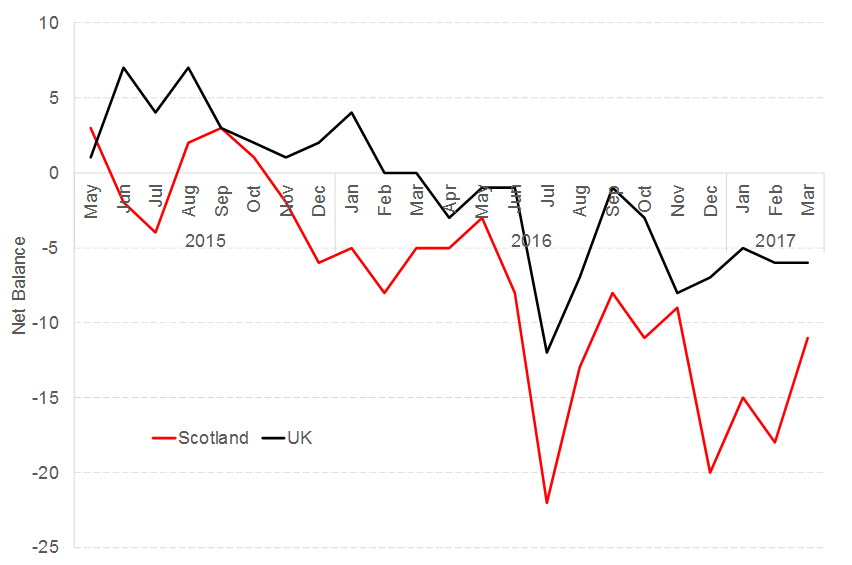

Business Surveys

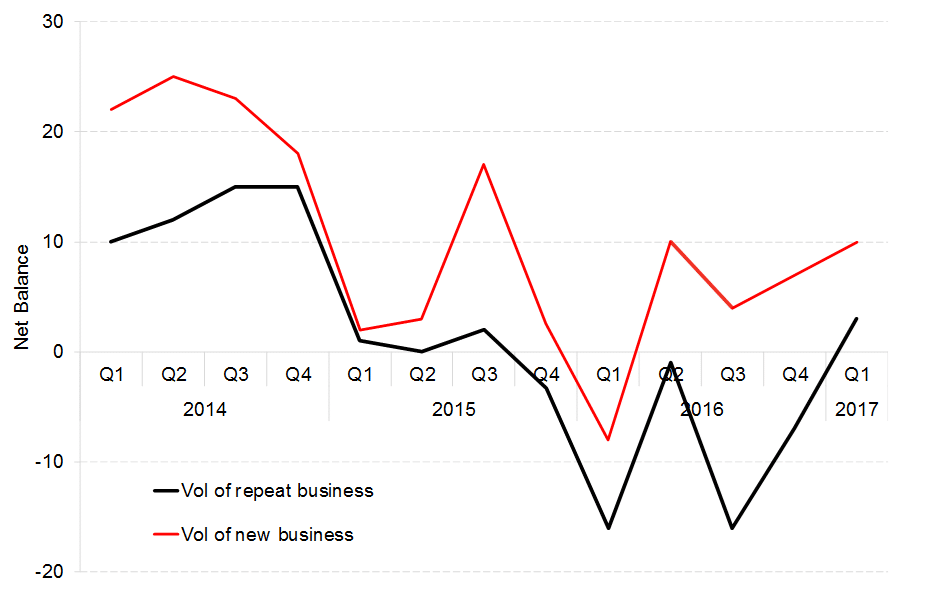

The FAI-Royal Bank of Scotland Business Monitor for Q1 2017 showed an increase in the net balance of firms reporting both repeat business and new business volumes were improving.

Indeed, Q1 2017 was the first time since mid-2015 that both measures were in positive territory. That being said, the net balance figures of below +10 are still low by historical standards.

Source: FAI/RBS Business Monitor (Q1 2017)

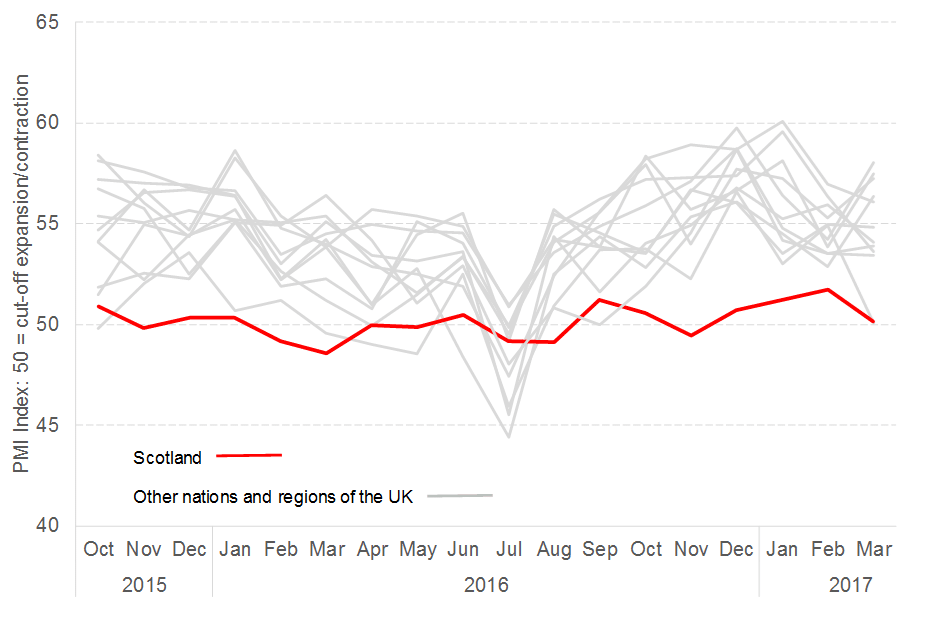

The Lloyds Bank Regional Purchasing Managers Index (PMI) for Scotland – undertaken by IHS Markit – has continued to remain perilously close to the cut-off point of 50 (where >50 marks a balance of firms reporting an expansion in their activities whilst a value of <50 marks a contraction). The Scottish figures of 51.2 in Jan, 51.7 in Feb and 50.1 in March compare against UK-wide figures of 55.2, 53.8 and 54.9 respectively.

As the chart highlights, this doesn’t seem to be just a ‘London effect’ dominating the UK figures.

Source: Lloyds Bank Regional Purchasing Managers Index (PMI) for Scotland, IHS Markit

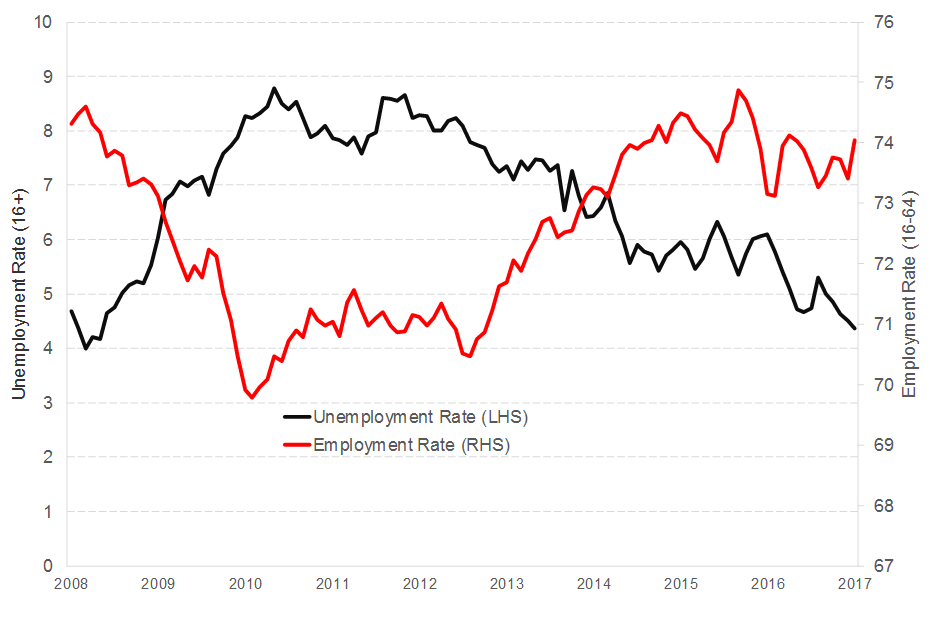

Labour Market

The Scottish labour market continues to hold up much better – at least at first glance.

Unemployment and employment are back to near the levels witnessed just before the financial crisis.

Over the first quarter of 2017, unemployment fell by 14,000 whilst employment rose by 5,000.

As we highlighted here, much of the improvement in the unemployment rate in recent months had been driven, not by people finding work but, by people leaving the labour market entirely. This trend has eased, albeit with inactivity rates in Scotland now higher than the UK as a whole.

Source: Labour Force Survey, ONS

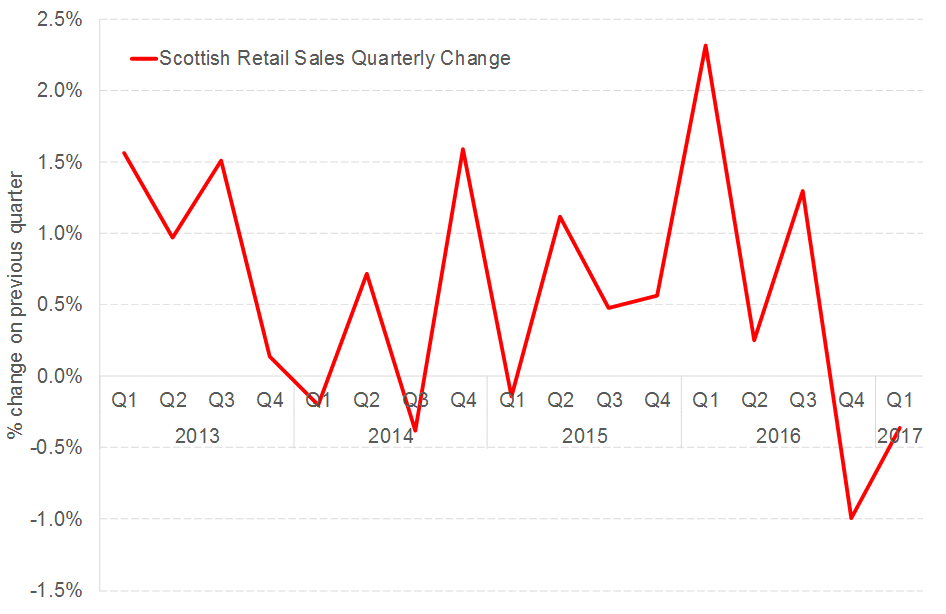

Retail and consumer confidence

But consumer confidence remains weak – not just in Scotland, but across the UK as higher inflation begins to bite.

Source: GfK Consumer Confidence Index

It’s therefore unsurprising that the official retail sales figures for Scotland – one early component of the official Scottish GDP series – declined again in the first three months of 2017 pushing that sector into recession (for the first time since 2012).

Source: Scottish Retail Sales Index, Scottish Government

UK GDP

The performance of the wider UK economy has an important bearing on Scottish growth. Around £11.5bn of Scottish exports are sold to rUK each quarter.

All things remaining equal, a healthy UK economy is good news for the Scottish economy.

The UK had grown relatively strongly through most of 2016, confounding most predictions. But the growth was driven almost entirely by rapid increases in consumer spending. This couldn’t last – particularly with rising inflation.

UK growth in the first three months of 2017 was just 0.2%. This suggests that a source of buoyancy over the last year, may provide less of a boost this time around.

Conclusions

On balance, it’s difficult to conclude anything other than the Scottish economy remains in a fragile position.

Whether or not it will be confirmed in July that we have entered recession is in the balance.

Given the way in which economies operate (and the statistical data is compiled), some form of bounce back is likely at some point. In the short-term, whilst not impossible, the balance of evidence suggest that this is unlikely.

But whatever the next set of GDP data tell us, what is key is the trend over the long-term.

Talk back in 2008 was for the potential of a lost decade of growth. Since 2006, output per head in Scotland has increased by just over 1% (that’s not an average growth rate, that’s the total increase).

With the new fiscal powers coming on stream this year, getting the economy growing again – and on a sustainable basis – will be vital not just for jobs and prosperity, but also our public services.

Authors

The Fraser of Allander Institute (FAI) is a leading economy research institute based in the Department of Economics at the University of Strathclyde, Glasgow.