The income tax system has changed a lot over the last parliament, with the introduction of new tax bands and changes to both rates and thresholds. These changes go against the SNP’s 2021 manifesto promise to freeze both income tax rates and bands.

We’ll go through these changes, and what they mean for the taxes paid by people in Scotland compared to the rest of the UK.

Changes to rates and thresholds

At the start of the parliamentary term, Scotland operated a five-band income tax system – more bands than the three-band system in the rest of the UK.

In the 2023-24 budget, the higher rate increased from 41% to 42% and the top rate from 46% to 47%, while the top rate threshold decreased from £150,000 to £125,140. The 2024-25 budget introduced the most significant structural change: a new, sixth income tax band. The 45% advanced rate was introduced, applying to income between £75,001 and £125,140.

Thresholds for lower income bands – affecting those on lower and middle incomes – have increased in recent budgets, broadly keeping pace with inflation. However, thresholds for the higher rate and above have remained frozen.

Table 1 summarises these changes to income tax across the parliament.

Table 1: Scottish income tax rates and thresholds in 2021/22 and 2026/27

| 2021/22 | 2026/27 | |||

| Threshold | Rate | Threshold | Rate | |

| Personal Allowance | £0–£12,570 | 0% | £0–£12,570 | 0% |

| Starter Rate | £12,571–£14,667 | 19% | £12,571–£16,537 | 19% |

| Basic Rate | £14,668–£25,296 | 20% | £16,538 – £29,526 | 20% |

| Intermediate Rate | £25,297–£43,662 | 21% | £29,527 – £43,662 | 21% |

| Higher Rate | £43,663–£150,000 | 41% | £43,663 – £75,000 | 42% |

| Advanced Rate | – | – | £75,001 – £125,140 | 45% |

| Top Rate | Above £150,000* | 46% | Above £125,140* | 48% |

*A higher/advanced rate taper is applied to incomes over £100,000. For each £2 earned above £100,000, there is a £1 reduction in the £12,570 tax free personal allowance. The personal allowance is zero once adjusted net income reaches £125,140 or more.

Comparison with the rest of the UK

These changes have widened the differences between the Scottish income tax system and the one operating in the rest of the UK.

Lower earners benefit slightly in Scotland. Individuals earning below the median income pay a little less tax than they would elsewhere in the UK, largely because of Scotland’s 19% starter rate (compared with the 20% UK basic rate). This applies to incomes between £12,571 and £16,537, and results in a maximum annual saving of £40 (around 76 pence per week).

However, middle and higher earners pay more. Anyone earning above £29,526 per year pays more income tax in Scotland than they would in the rest of the UK.

The starkest difference is visible when income tax is considered alongside National Insurance contributions (NICs). NICs are set by the UK Government and apply consistently across the whole of the UK.

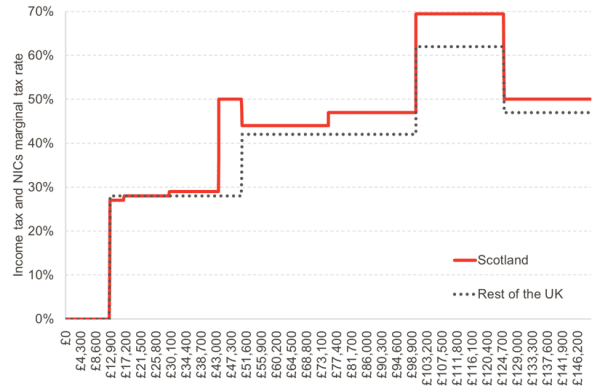

Figure 1 presents combined marginal tax rates for income tax and NICs, measuring the tax paid on each additional pound earned.

Figure 1: Income tax and NICs marginal tax rates in Scotland and the rest of the UK

Source: FAI calculations

For all employees across the UK, the NICs rate falls from 8% to 2% at £50,270 – the point where the higher rate of income tax begins in the rest of the UK. However, in Scotland, the higher rate starts earlier, at £43,663.

This means that Scottish employees earning between £43,663 and £50,270 face a combined marginal tax rate of 50% – 22 percentage points higher than the rate faced by taxpayers elsewhere in the UK earning the same income. This is the largest gap in marginal tax rates between Scotland and the rest of the UK at any income level.

When we look at the Scottish tax system at the margin –combining income tax with NICs, which is the reality of tax paid by the vast majority of Scottish taxpayers – parts of the Scottish tax system are less progressive than they might first appear. While lower earners (£12,570–£16,537) pay a lower marginal rate than in the rest of the UK, within Scotland those earning between £43,663 and £50,270 face a higher marginal rate than those earning between £50,270 and £100,000. They also face the same combined marginal rate (50%) as anyone earning £125,140 or more.

There is an even higher marginal rate between £100,000 and £125,140, as a result of the gradual withdrawal of the personal allowance – this is true for the whole of the UK, although the higher Scottish rates at those incomes compound to create an effective marginal rate of 69.5% – higher than in the rest of the UK.

Are people changing their behaviour in response to higher taxes?

A key question when tax rates diverge is whether people adjust their working behaviour in response. This could include reducing hours worked, taking a pay cut in exchange for other benefits, or using salary sacrifice arrangements (such as increased pension contributions) to reduce taxable income.

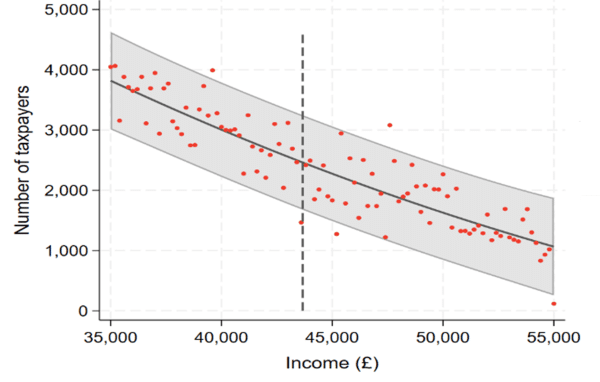

We examined the latest available Scottish taxpayer data from 2022-23 to assess if this is happening in Scotland in response to the difference in tax rates.

We looked for evidence of income “bunching” – an unusually high concentration of taxpayers just below the Scottish higher rate threshold of £43,663, where the combined marginal tax rate jumps sharply from 29% to 50%. However, we only found weak evidence of this.

Figure 2 shows the distribution of taxpayers around the higher rate threshold. While there are slightly fewer taxpayers than expected just below the threshold (statistically significant at the 5% level), there is no corresponding cluster elsewhere below that threshold relative to those above it.

Figure 2: Distribution of taxpayers around the Scottish higher rate threshold

Source: SPI data 2022/23 and FAI calculations

Note: The shaded grey area represents two standard deviations from the expected distribution of taxpayers. Data points outside this range indicate statistically significant divergence from the expected value at the 5 per cent level.

It is important to note that this analysis uses 2022-23 data – the most recent available – due to the time it takes for tax records to be published. Stronger evidence of behavioural change may emerge as more recent data becomes available. As incomes have continued to grow and the higher rate threshold has remained frozen, more taxpayers will have moved closer to the threshold in subsequent years.

Future considerations for income tax in Scotland

When the Scottish Government sets income tax rates, it must also consider the knock-on effect on Scotland’s overall funding from the UK Government.

Under the fiscal framework, when the Scottish Government raises income tax, money is deducted from the funding Scotland receives from the UK Government through the Block Grant Adjustment (BGA). The BGA is linked to income tax performance in the rest of the UK.

Differences in income distribution mean that earnings growth in England, particularly at the top of the income distribution driven by London, generates proportionally more tax revenue than in Scotland. As a result, Scotland needs higher income tax rates than those in the rest of the UK to raise an equivalent level of revenue. We estimate that aligning Scottish income tax rates and bands with those in the rest of the UK would reduce Scottish Government revenues by around £1.1 billion per year.

This blog is part of our 2026 Scotland and Wales Election Analysis. For more details on income tax and other key policy choices over the 2021-2026 Parliament, click the link to read our report Setting the scene: Scotland on the eve of the 2026 Election.

This work is supported by the Nuffield Foundation. The Nuffield Foundation is an independent charitable trust with a mission to advance social well-being. It funds and undertakes rigorous research, encourages innovation and supports the use of sound evidence to inform social and economic policy, and improve people’s lives. The Nuffield Foundation is the founder and co-funder of the Nuffield Council on Bioethics, the Ada Lovelace Institute and the Nuffield Family Justice Observatory. Find out more at: nuffieldfoundation.org.

The views expressed are those of the authors and not necessarily those of the Foundation.

Authors

Ciara is a Knowledge Exchange Fellow at the Fraser of Allander Institute. Her main area of focus is macroeconomic and fiscal analysis. She has recently completed a secondment to the Scottish Fiscal Commission, where she worked as an Economic and Fiscal Analyst in the economy team forecasting macroeconomic conditions.

João is Deputy Director and Senior Knowledge Exchange Fellow at the Fraser of Allander Institute. Previously, he was a Senior Fiscal Analyst at the Office for Budget Responsibility, where he led on analysis of long-term sustainability of the UK's public finances and on the effect of economic developments and fiscal policy on the UK's medium-term outlook.