Frantisek Brocek

The coronavirus outbreak – and the public health response – will have a range of impacts upon the economy, and on individuals whose livelihoods will be impacted.

One issue, particular when asking those self-employed to forgo income by self-isolating or asking others to scale back their day-to-day activities, will be how it impacts upon family budgets.

A concern that policymakers will be mindful of, and will no doubt be looking to develop a response to, will be how to support households who may be most vulnerable to any fall-off in income.

At times like these it is crucial that households have enough liquid savings to draw upon if they need to forgo regular income for some time.

We have used the Wealth and Assets Survey to see how many Scottish households have per adult liquid assets to allow them to cover 1 month, 3 months, or 6 months of their regular income.

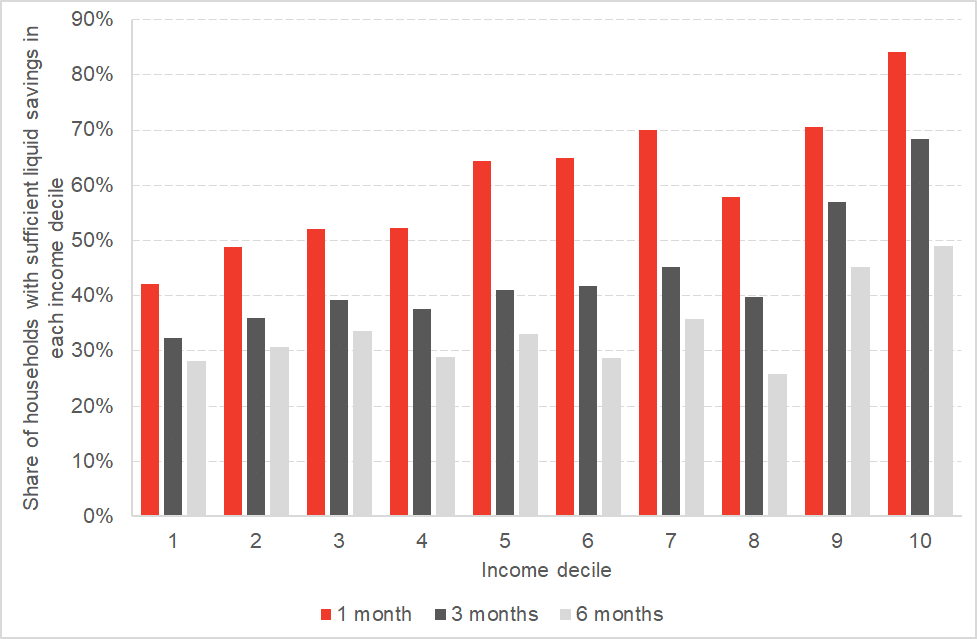

Chart 1: Share of Scottish households in each income decile with enough liquid savings to cover a period without regular income

Note: We have used the definition of liquid assets from this DWP report. Liquid savings and regular income are computed on a per adult basis for each household.

Chart 1 shows that households at the bottom of the income distribution have the lowest amount of savings. Only 42% of Scottish households in the bottom income decile would be able to cover 1 month of their regular income from savings. Circa three quarters of households in the bottom decile would not have a sufficient buffer if they had to forgo regular income for 6 months.

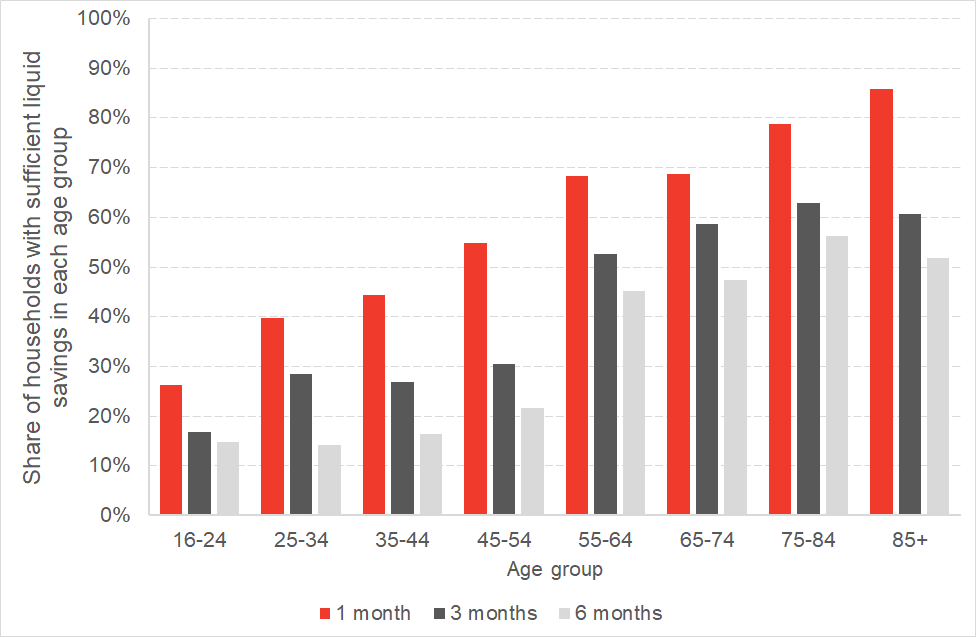

Chart 2: Share of Scottish households in each age group with enough liquid savings to cover a period without regular income

Note: Age group of the household representative.

The youngest age groups are the most vulnerable to unexpected income fluctuations. Only a quarter of 16-24-year olds have enough savings to cover 1 month of their income. On the other hand, older households who have saved for retirement typically have more liquid savings and are less reliant on income from work.

It is these groups that policymakers will be most concerned about supporting at the current time.

Clearly the welfare system is designed to provide support at such times, although key will be ensuring that it works swiftly and without delay. Last week’s announcements around sick-pay, grants and business rates are clearly designed to also provide support to small businesses who are vulnerable to temporary swings in the supply of labour and demand.

But the scale of the public health response means that we should expect to hear more in the coming days about support for households and those most impacted by any (temporary) fall off in income.

Authors

The Fraser of Allander Institute (FAI) is a leading economy research institute based in the Department of Economics at the University of Strathclyde, Glasgow.