Incoherent reforms to council tax: could have been worse, but not good enough

Scotland will follow the UK Government’s example and introduce higher taxes on higher value properties. Whereas at the UK Government level this is being done as a new surcharge flowing to central government, in Scotland it will be through two new council tax bands, with revenues staying with local government:

- Band I for properties valued between £1 million and £2 million; and

- Band J for properties valued above £2 million.

These will be based on ‘up-to-date’ valuations, but only for properties worth over £1m. The rest of us have to keep paying tax on the 1991 values of our property, and all the errors and inconsistencies that go with that.

The Scottish Government’s own commissioned analysis state that at least half of properties are in the wrong band – that is, they are in a higher or lower band (and paying too much or too little tax) than would be the case if council tax for all homes was based on up-to-date values. As the reform announced yesterday will only affect 1% of properties, that issues has not been solved.

Such a move by the Scottish Government to tweak around the edges is not surprising based on past experience but is hugely disappointing.

As the Scottish Government point out in the budget documents, a process of engagement, including a public consultation, is currently underway to look at reforms to the whole system, recognising “the importance of consensus, stability and fairness and is intended to inform decisions in the next parliament”. This reform for £1m+ homes will come in 2 years into the next parliament.

This point on consensus comes up time and time again. In a letter to the Local Government, Housing and Planning Committee in October 2025, Shona Robison said that:

“We believe that reform can only proceed if there is a consensus in favour of it. The Scottish Government does not believe that such consensus currently exists, which is why this consultation has been launched.”

The only thing that has changed since this letter was written is that the UK Government announcement of a similar scheme south of the border. The consultation is still open so no new consensus can have been drawn from that.

It could have been worse. Had new bands been introduced using 1991 property values, the distortions in the system would have been amplified. The most recent reforms in 2017 adjusted the multipliers for bands E, F, G and H using those 1991 valuations, and a similar approach proposed in 2023 was ultimately not taken forward. This may have been influenced, at least in part, by consultation feedback highlighting that reliance on 1991 values would often result in higher charges falling on the “wrong” properties.

While our standard response to successive budgets has been to describe them as a “missed opportunity” for council tax reform, this particular change also introduces a degree of incoherence. Maintaining a stated position that reform cannot proceed without consensus, while simultaneously implementing changes to one part of the system in the absence of such consensus, is impossible to reconcile.

There are other details that we need to wait for further information on, including any distributional analysis of the decision (as part of legal duties, analysis of the impact on different groups of people should have been done before the decision was made) or explanation of how much it will raise. Clarity on whether how/if additional income will be equalised across local authorities needs to be clarified– obviously most £1m+ properties will be clustered geographically, but this doesn’t mean that those geographical areas will retain all that income.

It’s not ideal that an announcement like this has been made without all that detail to go with it. In the Scottish Government’s defence, this isn’t due to take effect until 2028 so it is not part of the published assessments of the impact of the budget in 2026/27, with the only financial implication in the next financial year being some additional money to go to the Scottish Assessors for valuations. However, a policy decision has been made, and in the spirit of transparency we would have hoped to see more detail from the Scottish Government along with that announcement.

Outlook for spending is very tight

The Scottish Spending Review builds on the challenges we pointed out in our immediate Budget reaction on Tuesday, and underlines the challenges presented for whoever is in power at Holyrood after May.

The Spending review presents portfolio level spending for 2027-28 and 2028-29. The Scottish Fiscal Commission have helpfully produced a table which reverses transfers between portfolios in 2025-26, which (if not done) makes it more difficult to see how spending is changing over the SR period. [Table 2.12 in the Supplementary Fiscal Spreadsheets for those who want to check it out. As discussed in earlier blogs, it would be much better if the regular transfers were just baselined].

This shows the following for the big departments.

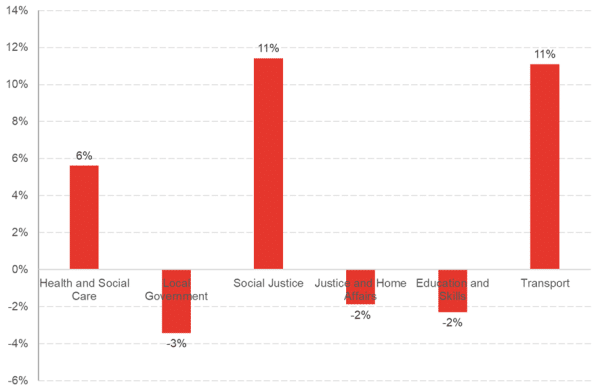

Chart: Spending Review – Change in Spending (Real terms) between 2025-26 and 2028-29

Source: Scottish Fiscal Commission

This shows that Health & Social Care (although it is really Health as the regular transfers to LG have been stripped out) is set to grow by 6% over 3 years in real terms. This is less than was assumed by the Scottish Government in the Medium-Term Financial Strategy in May, where they assumed that Health spending would have to grow 3.3% in real terms every year to keep up with demand.

Social Justice grows considerably over the 3 years, driven by social security spending, which continues the trend of this taking up an increasing proportion of the budget.

The local government settlement looks very difficult over the 3 year period, particularly as this includes social care where the Scottish Government have assumed, again, that there will be growing demands. The justice settlement also looks very difficult.

In the annexes to the spending review, the Government have set some details of workforce and other efficiency to help ensure that these spending envelopes will be deliverable with little effect on public services.

As you can see from the table below, the majority of this is assumed productivity and efficiencies in the health service. Whilst around two-thirds of the health efficiency savings come from a 3% recurring saving for NHS Boards, the rest is from “other efficiencies”. On the workforce side, it is the justice system that will have to demonstrate a large proportion of the workforce savings, and the largest chunk of savings from service reform. There is also a sizeable line for Local Government – “Other Efficiencies and Reform” for which there are no details.

Table – Efficiencies and Reform in the Spending Review

| Efficiencies and Productivity | 2026-27 | 2027-28 | 2028-29 |

| Health | 384 | 374 | 303 |

| Finance and LG | 14 | 9 | 8 |

| Social Justice | 11 | 7 | 8 |

| Education and skills | 20 | 11 | 13 |

| Justice & Home Affairs | 29 | 42 | 55 |

| Transport | 5 | 4 | 2 |

| DFM, Economy & Gaelic | 11 | 7 | 7 |

| Housing | 2 | 1 | 1 |

| Rural Affairs | 8 | 7 | 6 |

| Climate Action & Energy | 3 | 4 | 4 |

| Constitution, External Affairs & Culture | 4 | 2 | 2 |

| COPFS | 0.4 | 0.4 | 0 |

| Total assumed from efficiencies and productivity | 492 | 468 | 408 |

| of which -Workforce Savings | 2026-27 | 2027-28 | 2028-29 |

| Finance and LG | 10 | 7 | 7 |

| Social Justice | 6 | 4 | 5 |

| Education and skills | 18 | 7 | 10 |

| Justice & Home Affairs | 19 | 32 | 45 |

| Transport | 2 | 1 | 1 |

| DFM, Economy & Gaelic | 8 | 5 | 6 |

| Housing | 2 | 1 | 1 |

| Rural Affairs | 8 | 7 | 6 |

| Climate Action & Energy | 2 | 3 | 3 |

| Constitution, External Affairs & Culture | 4 | 2 | 2 |

| COPFS | 0 | 0 | 0 |

| Of which – total workforce savings | 81 | 69 | 85 |

| Service Reform | 2026-27 | 2027-28 | 2028-29 |

| Finance and LG | 1 | 2 | 2 |

| Social Justice | 0 | 0 | 1 |

| Justice & Home Affairs | 5 | 12 | 20 |

| DFM, Economy & Gaelic | 2 | 0 | 0 |

| Rural Affairs | 6 | 2 | 4 |

| Climate Action & Energy | 1 | 0 | 1 |

| Constitution, External Affairs & Culture | 4 | 2 | 2 |

| COPFS | 1 | 1 | 0 |

| Total Service Reform | 18 | 18 | 29 |

| Other Efficiencies and Reform | 2026-27 | 2027-28 | 2028-29 |

| Finance and LG | 53 | 37 | 38 |

| Total other efficiencies and reform | 53 | 37 | 38 |

| TOTAL SAVINGS FROM EFFICIENCIES & REFORM* | 563 | 523 | 476 |

Source: Spending Review 2026

* when first published this mistakenly double counted workforce savings – apologies

The extent to which these cuts in spending are achievable is difficult to assess, given the detail of some of these efficiency measures that we have. For local government, given the social care service is likely to be under the same sort of pressure as the health system, there are particular challenges to deliver services at the current level in the face of the overall settlement.

The area that looks like it has taken the biggest clobbering though is the justice system. It does not seem credible that such large cuts can be made to this area without impacts on services.

Authors

Mairi is the Director of the Fraser of Allander Institute. Previously, she was the Deputy Chief Executive of the Scottish Fiscal Commission and the Head of National Accounts at the Scottish Government and has over a decade of experience working in different areas of statistics and analysis.

Emma Congreve is Principal Knowledge Exchange Fellow and Deputy Director at the Fraser of Allander Institute. Emma's work at the Institute is focussed on policy analysis, covering a wide range of areas of social and economic policy. Emma is an experienced economist and has previously held roles as a senior economist at the Joseph Rowntree Foundation and as an economic adviser within the Scottish Government.

João is Deputy Director and Senior Knowledge Exchange Fellow at the Fraser of Allander Institute. Previously, he was a Senior Fiscal Analyst at the Office for Budget Responsibility, where he led on analysis of long-term sustainability of the UK's public finances and on the effect of economic developments and fiscal policy on the UK's medium-term outlook.