Growth returns to the Scottish economy – with the fastest quarterly pick-up in over two years

Today’s figures report substantial (and welcome) growth of +0.8% in the Scottish economy in Q1. Not only does this mean that the economy avoids falling into the technical definition of recession – defined as two quarters of falling output – but it means that it has made up some of the ground lost last year (when it did not grow at all).

This blog summarises the key results from today’s figures.

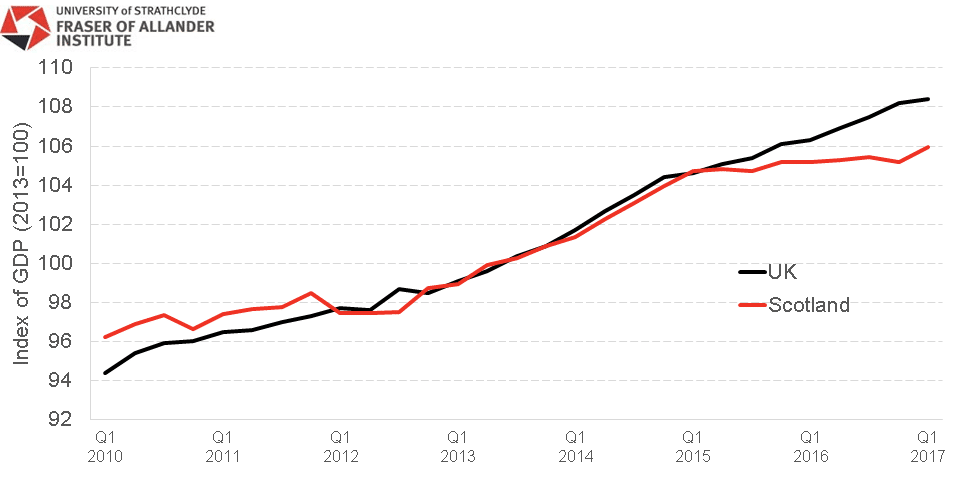

Relative to the UK

Growth of +0.8% in Scotland in Q1 is above the equivalent growth of +0.2% in the UK economy as a whole in Q1. However, as the following chart shows the UK economy has grown far faster than the Scottish economy since 2015.

Drivers of growth

The first obvious question is why – with all indicators of business activity and confidence suggesting relatively weak growth at best – do the GDP statistics produced by the Scottish Government suggest such a substantial pick-up in activity in the first three months of 2017?

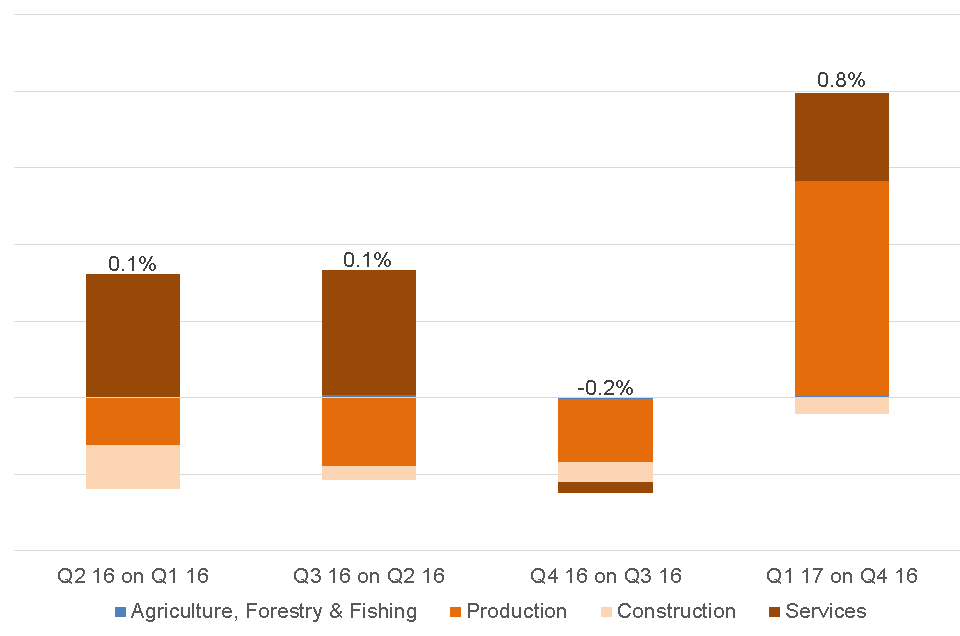

The explanation lies in the sectoral split of growth, summarised at a high level in the following chart.

For services and construction, which together make up over 80% of the economy, growth was good but relatively unspectacular. Services grew 0.3% (slightly below trend of 0.4%) whilst construction output actually fell 0.7%.

Taken together these would have led to growth overall in the economy – indeed spot on with what our Nowcast is telling us about the Scottish economy’s performance.

But what has driven the scale of the upswing was the massive growth in production of 3.1%! This is the first time production sector activity has grown since Q1 2015.

To put this in context, the only other time that the production sector has reportedly grown faster than this – since the Scottish series began in 1998 – was in Q3 2009.

There appear to be four key reasons for this.

- Firstly, the figures show a substantial rise of over 7% in metals manufacturing, driven in part by the re-opening of the Dalzell steel plant.

- Secondly, as our latest Oil and Gas survey highlighted, there has been a growing return to confidence in the oil and gas supply chain. The data published today appears to indicate that this has actually now translated into a welcome degree of bounce-back in actual activity within the sector.

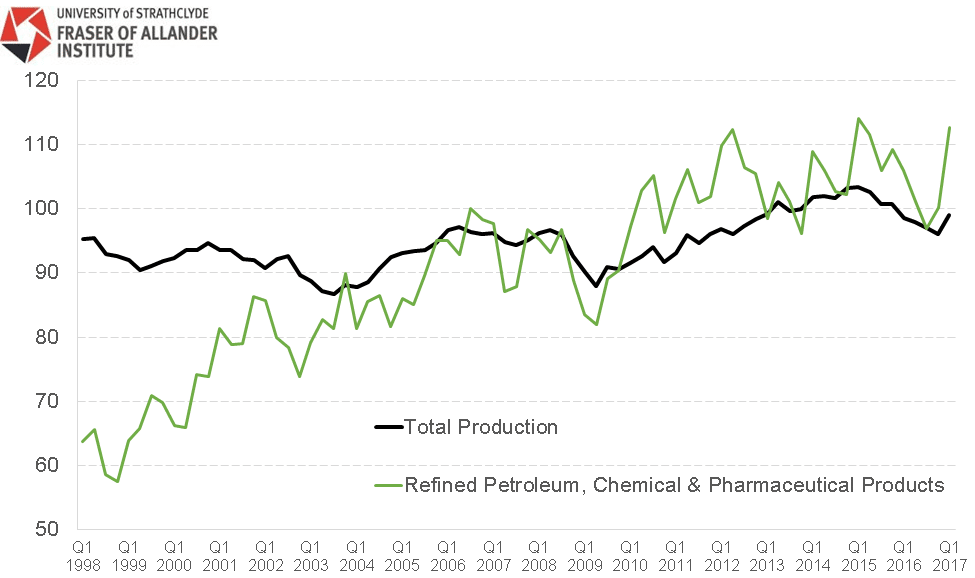

- Thirdly, the figures report massive growth of over 12% in refined petroleum output which is largely output from Grangemouth. We’d urge caution with this series as it’s especially volatile as the chart below highlights – usually around Q1- in contrast to the overall production series.

- Finally, other sectors of manufacturing have also bounced back from a weak 2016. Food and drink for example, also grew strongly by historical standards.

All these positive factors have happened to coincide with each other during this quarter, helping to pull up overall growth quite significantly. Whilst positive, it is entirely possible that a number of these factors will only have a (large) temporary impact on the quarterly results. Key will be how sustainable the pick-up is in the months ahead.

One thing to note is that unlike with previous one-off events impacting on headline GDP figures, for instance when power plants have closed, there is no explanation for these one-off events in the statistical publication accompanying today’s data; they are only picked up in the Scottish Government press release. This is unusual.

Finally, it is worth noting that these data also report substantial growth of 0.6% and 0.5% respectively in the Education sector and the Health and Social Work sector this quarter. These are large increases. This means that the data now show that the GDP contribution of the Health and Social Work is 2.1% larger, in real terms, than it was this time last year.

Longer-term performance

All this being said, as we outlined in our report last week, whether or not the quarterly figures are above or over the line is largely unimportant. What is much more important is the longer-term trend. In this regard, today’s figures are welcome progress but policymakers will be hoping for a few more quarters of growth at this pace before they are reassured.

For example, whilst production output is up over 3% this quarter, it is still down -4.2% over the past two years.

And taken with the contraction of -0.2% in the overall economy at the end of last year, and very weak growth during the earlier part of 2016, output in Scotland has still been weaker than the UK as a whole.

So on balance, these data do not change the fact that the Scottish economy still faces a fragile outlook – particularly when you factor in likely effects of possible higher inflation and any Brexit uncertainty in the months to come.

We continue to forecast that growth in the Scottish economy will continue through 2017.

And today’s figures are consistent with that outlook. So if Scotland can – over the remaining three quarters of 2017 – secure its average quarterly growth rate of 0.35% then this will bring in 4Q-on-4Q growth over 2017 of 1.2%. Identical to our June forecast.

Later on this month, we’ll get official data from the Office for National Statistics on earnings growth in Scotland which will give a further insight into how the performance in the wider economy is feeding through to living standards. These figures will be of particular interest to the Scottish Fiscal Commission as they get set to forecast tax revenues. They will also probably be interested in how measures of consumer confidence and business activity continue to perform and whether or not they give an alternative insight into how the underlying economy is performing in practice (and therefore how tax revenues might perform).

So all in all, whilst very welcome, we’d urge caution in dusting down the bunting and streamers just yet! There is much work still to be done if the Scottish economy is to fully make up recent lost ground.

Authors

The Fraser of Allander Institute (FAI) is a leading economy research institute based in the Department of Economics at the University of Strathclyde, Glasgow.