In recent weeks, there has been considerable debate over the government’s decision to freeze the income tax threshold at which taxpayers start to pay the 40% higher rate in Scotland.

This has led the Conservatives to argue that Scotland is now the highest taxed part of the UK.

This blog discusses some of the key issues underpinning this argument and some important questions around interpretation.

The Scottish Government’s income tax decision for 2017/18

The Scottish Government has decided to use its new ‘Smith powers’ over income tax to set a different policy to that in the UK from next month.

The higher rate income tax threshold will be frozen in Scotland at £43,000 in 2017/18. In contrast, the Chancellor confirmed in his Budget in March that the same threshold elsewhere in the UK will rise to £45,000.

The OBR estimate that this will raise around £125 million for the Scottish Government in 2017/18.

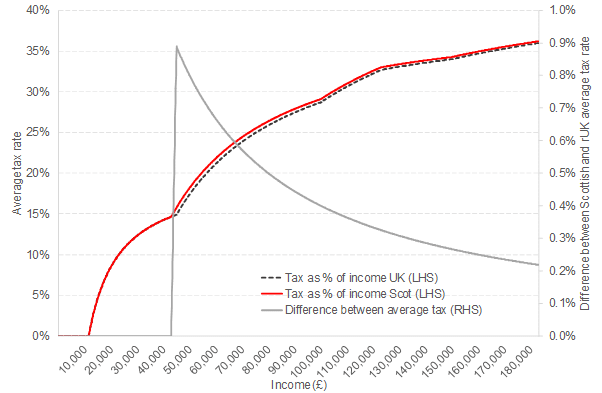

When considering the impact of tax on individuals and households, it’s important to look at both the average and marginal tax rates. These have important implications for the distributional implications of tax and the incentives faced by individuals. They are therefore useful when comparing tax rates across countries.

- The average tax rate is the amount of tax paid as a proportion of total income

- The marginal tax rate is the tax paid on the last pound of income earned.

As a result of the different policies pursued by the Scottish and UK Governments, around 374,000 tax payers in Scotland – those earning above £43,000 – will now face a higher average tax rate than equivalent taxpayers in rUK.

The higher tax liability results from the fact that the higher rate of tax (40%) applies over a wider range of income in Scotland. Most will pay £400 more in tax per year – i.e. paying a 40% rate rather than a 20% rate on income between £43,000 and £45,000. For those earning between £43,000 and £45,000 the amount will be less.

As the chart highlights, the effect is that all Scottish taxpayers earning above £43,000 will pay a marginally higher average tax rate than equivalent taxpayers in rUK – as demonstrated by the red line vis-à-vis the black dotted line.

The difference in average tax rate between Scottish and rUK taxpayers is greatest for those earning £45,000, and then declines. Needless to say, this is because a £400 tax differential is greater for someone earning £45,000 than it is for someone earning £150,000.

It’s important to put these differences in context, however.

Firstly, as the chart highlights, for most higher rate taxpayers the difference – at least in this first year – is small.

Secondly, the changes only impact on around 14.5% of income tax payers in Scotland. Over 85% of taxpayers will be unaffected and will pay the same as elsewhere in the UK.

What about the effect on marginal tax rates?

Again, for the vast majority of higher rate taxpayers, there is no difference in marginal tax rate between Scotland and rUK.

The exception is for those individuals who earn between £43,000 and £45,000, who pay a marginal tax rate twenty percentage points higher in Scotland than their counterparts in rUK*.

Income tax differentials are only part of the story….

Income tax is of course only one of the taxes now devolved.

Decisions on business rates and LBTT are also clearly important. But arguably of most relevance in terms of the taxes paid on a day-to-day basis by households is council tax.

Council tax comparisons with the rest of the UK are not straightforward. The most obvious method is simply to compare average tax rates in Band D. Band D council tax is the standard measure of council tax (all other bands are set as a proportion of the Band D).

This does however, have a number of weaknesses as it assumes for example, that the distribution of houses across bands is the same in Scotland and rUK. We will return to this in future analysis.

From April, the multipliers applied to the highest council tax bands E-H in Scotland will increase. The table sets out the average bills both before and after reform.

| Average Scottish Council Tax Bill – 2016-17 | Band A | Band B | Band C | Band D | Band E | Band F | Band G | Band H |

| Pre-reform | £766 | £894 | £1,021 | £1,149 | £1,404 | £1,660 | £1,915 | £2,298 |

| Post-reform | £766 | £894 | £1,021 | £1,149 | £1,510 | £1,867 | £2,250 | £2,815 |

Average Band D council tax bills in England in 2016/17 were higher than the Scottish average at £1,530. In Wales – where they have an additional Band I – the average Band D rate was £1,374.

These differences are sufficiently large that even with the higher multipliers in Scotland for bands E-H, the average bill in England and (mostly) Wales in these higher banded properties would have still been higher. For example, the average Band H at a ratio of 18/9 of Band D in England would have been £3,060 in 2016/17.

Of course, after 9 years, the council tax freeze has been lifted in Scotland. The majority of Scottish councils have decided to increase bills – 21 by the maximum 3%, 3 by less than 3%, with 8 deciding on no change. But whilst details on average increases in England and Wales are not yet available, reports suggest that many councils will opt for similar, if not greater, increases (with the maximum capped at 5%) to cope with pressures in social care.

Overall therefore, the gap in terms of tax paid by band is likely to remain.

So is Scotland the highest taxed part of the UK?

Firstly, the vast majority – 85% – of Scottish taxpayers will pay the same (not more) in income tax than someone earning the same amount in England or Wales.

Secondly however – and for the first time since devolution – taxpayers earning above £43,000 in Scotland will pay more in income tax than someone earning the same amount in England or Wales (up to £400 per year).

But even then, such differences are marginal.

Thirdly, on other measures of tax – such as council tax – and whilst comparisons are not straightforward, average council tax bills by band are lower in Scotland.

But the prospects for a larger gap in tax structures between Scotland and rUK could emerge. The Conservatives have plans to raise the higher rate threshold in the rest of the UK to £50,000 by ‘the end of the Parliament’; should the equivalent rate in Scotland remain at £43,000, the tax differential for those affected would rise to £1,400. The economic impact of any differences is likely to be particularly focussed at key points in the income distribution.

Of course, what this debate ignores is what taxpayers get in turn from the taxes raised. Whether someone is better or worse off ultimately is very hard to determine as it’ll depend upon a wide range of spending and policy decisions taken by the Scottish Government, some of which will be financed by different decisions taken on tax.

One potential risk from the narrow debate about whether or not 15% of the population face a slightly higher average tax rate than in the rest of the UK is for a wider narrative about Scotland’s apparent lack of competitiveness is allowed to develop. To counter this, individuals and businesses are likely to press the government on their long-term tax objectives – across all devolved taxes – and crucially, how any revenues raised will support investment in growth and the economy.

* Individuals earning between £43,000 and £45,000 will pay an income tax rate of 40% in Scotland, but 20% in rUK. Marginal tax rates are sometimes calculated to include employee National Insurance Contributions. Including employee NICs (which are 12% at income below the UK higher rate threshold), individuals earning between £43,000 and £45,000 will pay a marginal rate of 32% in rUK but 52% in Scotland. Ironically, this is a higher marginal tax rate than is faced by those earning over £45,000, as the employee NICs rate falls to 2% on income above the UK Government’s higher rate threshold (i.e. £45,000).

Authors

The Fraser of Allander Institute (FAI) is a leading economy research institute based in the Department of Economics at the University of Strathclyde, Glasgow.