When the Chancellor Phillip Hammond sits down after delivering his Budget on Wednesday, this will signal the start of the final three weeks of preparations before the Scottish budget is launched on December 14th.

But how will the decisions and announcements made on Wednesday effect the options and choices available to Cabinet Secretary for Finance Derek Mackay in his budget three weeks later?

To answer this, you need to remember that the resources available to the Scottish Government to fund day-to-day expenditure depend on three things:

- The block grant from Westminster – which is effectively determined by changes to English spending on functions that are ‘comparable’ to those delivered by the Scottish Government);

- The forecasts for the block grant adjustments – deductions to the block grant to account for the revenues that have been transferred from Westminster to Holyrood; and

- The forecasts for revenue raised from taxes devolved or transferred to the Scottish Government.

We will find out about the block grant and the block grant adjustments on Wednesday. But we’ll have to wait until the Scottish Fiscal Commission publishes its revenue forecasts in December before we’ll have all the pieces in the jigsaw.

What will we learn on Wednesday about the first two elements?

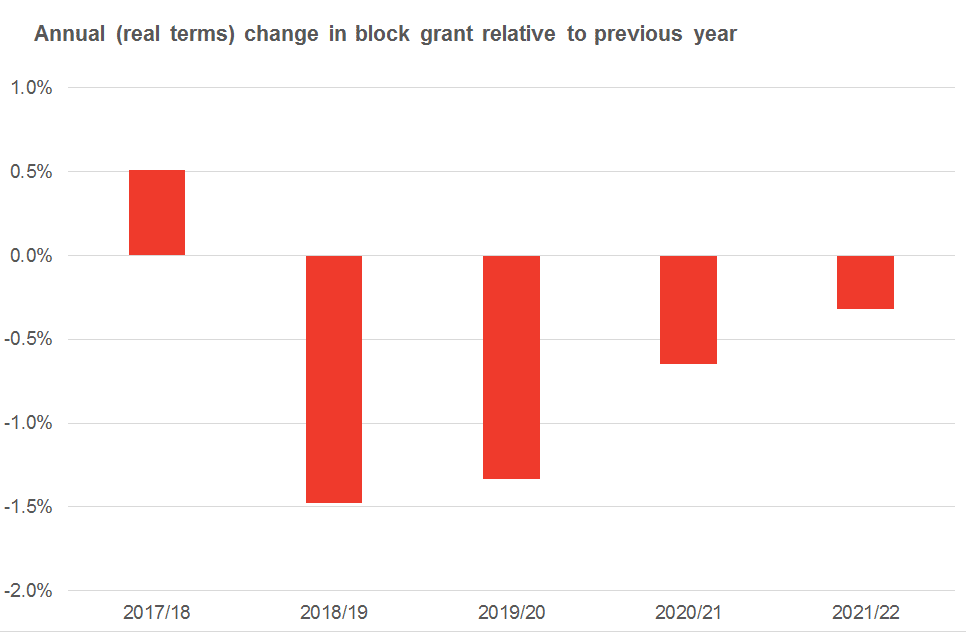

When the Chancellor set out his Budget in March, the Scottish Government’s block grant was projected to fall by 1.5% in real terms between 2017/18 and 2018/19, before falling by a further 1.3% in 2019/20. If those plans were unchanged, that would make for a very challenging couple of years for Mr. MacKay (in 2017/18, the block grant actually went up slightly).

How much is this outlook likely to change on Wednesday? We can be reasonably confident that the outlook won’t deteriorate. The Chancellor had planned in some ‘headroom’ for himself in meeting his self-imposed target to achieve a fiscal deficit of 2% of GDP by 2020/21. Even if the OBR forecasts on Wednesday that the medium term outlook has deteriorated (which they have already indicated will be the case), the outlook is unlikely to deteriorate sufficiently to justify clawing back any departmental spending commitments made just eight months ago.

But equally the Chancellor is unlikely to feel able to loosen the reigns on departmental spending significantly. He faces substantial pressure from within his own party to stay firmly on course to meet the fiscal target he set himself this time last year. With borrowing costs potentially on the rise following increases in interest rates – not to mention the as yet unknown fiscal costs of Brexit – his track record suggests that he will want to demonstrate he remains in control of the UK’s public finances.

In principle the Chancellor could raise additional revenues from tax increases, and no doubt he will find some scope for doing so. But parliamentary arithmetic means that scope for bold tax rises is limited.

So we probably won’t see the Chancellor respond in full to the argument from Simon Stevens, head of NHS England, that the NHS needs an additional £4bn a year (which would generate around £350m consequentials for the Scottish budget). Nor are we likely to see a fully-resourced commitment to increase public sector pay to match inflation.

But we will see some additional consequentials, although whether these will be sufficient to turn those real terms cuts into increases remains to be seen. Key areas to look out for include support for local government to avoid sharp increases in business rates.

For the Scottish block grant to remain unchanged in real terms in 2018/19 requires around £420m of additional consequentials to be announced on Wednesday relative to what had been set out in March.

What about the block grant adjustments? These are estimates of the revenues that the UK Government has foregone as a result of transferring revenue streams to Scotland.

There is a block grant adjustment for each of the taxes that has been transferred as part of the Scotland Acts 2012 and 2016. The BGAs are deducted from the block grant, so the bigger the BGA, the bigger the deduction, and the ‘worse off’ the Scottish budget is.

Two things thus determine the size of the BGAs:

- The growth of the relevant ‘tax base’ in rUK (so for income tax, the tax base is ‘taxable income’, and the rate at which this grows depends on things like employment rates and wages);

- rUK tax policy (higher tax rates imply higher revenues and vice versa)

What does this mean practically?

If, as expected, the OBR revises down its forecasts for rUK income tax revenues in 2018/19 and 2019/20 as a result of slower growth in the tax base, this means the income tax BGA will be smaller in those years.

A smaller BGA means less deducted from the Scottish block grant and a larger budget, yes?

Well all else equal, yes that’s the principle.

But bear in mind that any downwards revision to the OBR’s forecasts for rUK income tax revenues will probably just be the precursor to the Scottish Fiscal Commission revising down its forecasts for Scottish income tax revenues by a similar margin when it publishes its forecasts in three weeks.

In this sense, knowing the BGA forecast without knowing the Scottish revenue forecast only gives us part of the picture. But it at least gives us a sense of how high Scottish revenues need to be in order for the Scottish budget to be ‘no worse off’ than it would have been without income tax devolution.

Of more interest is what might happen to tax policy. Increasing the Higher Rate threshold in rUK more substantially than previously set out would reduce the BGA. As a result, the budgetary effect of the Scottish Government freezing the Higher Rate again, should it choose to do so, would increase.

What about Land and Buildings Transactions Tax (LBTT)? There have been some rumours circulating that the Chancellor might reduce rates of Stamp Duty Land Tax, or even provide a Stamp Duty ‘holiday’ to first time buyers. These policies would not apply in Scotland, but they would reduce the BGA for LBTT, potentially providing a small budget boost to the Scottish Government*. This however assumes that the Scottish Government will be able to resist calls to match any tax cuts that the Chancellor has made. Matching tax cuts in Scotland would negate the effects of a smaller BGA.

Finally, note that the outlook for capital spending is more straightforward. Additional spending announced by the Chancellor on Wednesday on comparable functions such as housing or roads will generate consequentials for the Scottish budget; but don’t expect these additional consequentials to be substantial.

So whilst the UK Budget on Wednesday will have implications for everyone in Scotland in its own right, it also shapes the constraints and choices for the subsequent Scottish budget in a variety of ways. On Wednesday we learn the context; on December 14th we’ll see how that context has shaped the details.

FAI will host its traditional post-Budget briefing event on at the University of Strathclyde’s Technology and Innovation Centre from 9am to 11am on the 24th November. Sign-up here.

* This might sound odd – how does a tax cut in rUK provide a budget boost to the Scottish Government? The principle here is that Scottish taxpayers shouldn’t pay to fund a tax cut in rUK. All else equal, a tax cut in rUK will reduce spending by the UK Government, which in turn will reduce the Scottish block grant. The fall in the BGA thus insulates Scottish taxpayers from any fall in public spending that might be engendered by the rUK tax cut.

Authors

The Fraser of Allander Institute (FAI) is a leading economy research institute based in the Department of Economics at the University of Strathclyde, Glasgow.