Today, HMRC published the first ever figures on the scale of ‘income tax reconciliations’ for Scotland.

These ‘reconciliations’ – whilst being a largely dry technical issue – are a key part of Scotland’s new fiscal framework.

These income tax reconciliations are reflections of the fact that Scottish budgets are initially set on the basis of forecasts. Once outturn data is known there is then an adjustment – or reconciliation – according to whether or not these forecasts turned out to be higher or lower than forecast.

Note: before reading this blog you might find it helpful to refresh your understanding of the budget process and the reconciliation issue here.

So what are the numbers?

The figures cover the 2017/18 budget.

At the time, two forecasts were made –

- A forecast by the OBR for the block grant adjustment (i.e. the amount taken out of the Scottish block grant to account for the fact that income tax powers have been devolved to Holyrood), based upon the relative growth rate of income tax receipts (per head) in the rest of the UK; and,

- A forecast by the Scottish Government of the growth in income tax receipts (per head in Scotland). NB: the forecasts for 2017/18 were undertaken by the Scottish Government, but they are now undertaken by the Scottish Fiscal Commission.

In the end, both forecasts for how much income tax would be raised in Scotland and the rest of the UK have turned out to be over-optimistic.

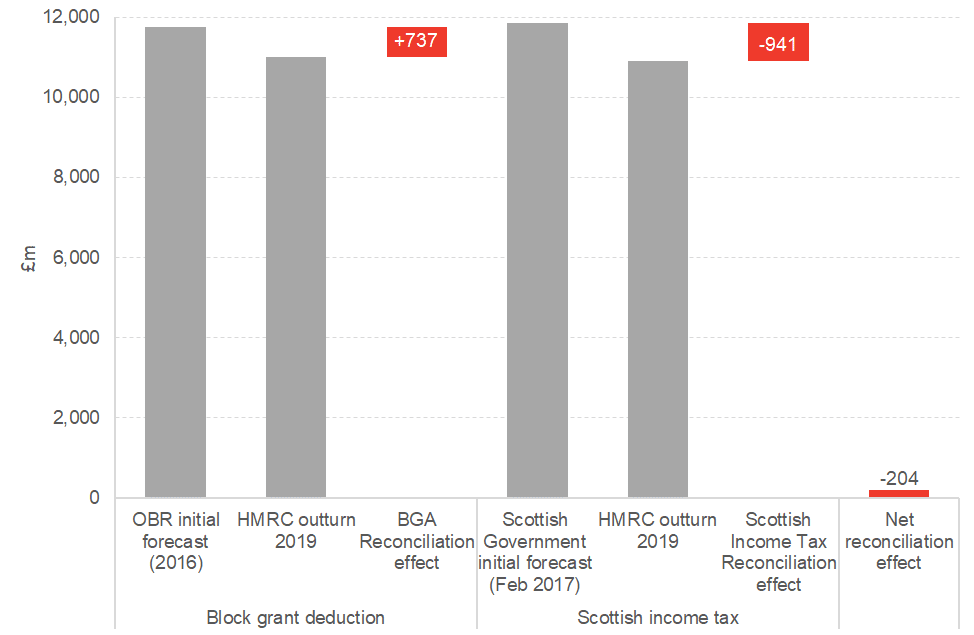

Chart: Forecasts and reconciliations

Source: UK Government

Back in 2016, the OBR forecast a block grant adjustment of £11,750m for Scotland. With outturn date now available, that figure is lower at £11,013m. As a result, the BGA for Scotland is around £740m lower than initially thought.

However, at the same time, the Scottish Government’s initial forecast of devolved income tax revenues of £11,857m has also just been confirmed to have been higher than outturn…but to the tune of around £940m (with the outturn figure being £10,916m). Some of this reflects the general drop-down in UK-wide receipts, with the rest a more specific net ‘Scottish effect’.

Two conclusions can be taken from this.

Firstly, the effect will be a ‘net reconciliation’ of £204m in funding for 2020/21 – the difference between the BGA reconciliation of £737m and the income tax reconciliation of £941m. As a result, the Scottish Government will have around £200m less in their budget next year than previously thought. This is broadly in line with what the SFC forecast back in May.

As we said previously, to call this a ‘black hole’ is an over-dramatization. But it does mean the Scottish Government will have to find resources from future budgets to pay for this reconciliation.

The government can manage this adjustment either through growing spending by less, different tax choices, using its borrowing and/or drawing upon its reserves.

Secondly, note that the outturn figure for Scottish income tax receipts is less than the outturn figure for the BGA. In other words, tax receipts per head grew more quickly in the rest of the UK in 2017-18 than in Scotland, despite the Scottish Government increasing the tax burden. In effect, the gap in the growth in the tax base in that year was sufficient to more than offset the increase in tax burden.

What next?

This is the first year of reconciliations and they will continue each year going forward.

The forecasts from the SFC in May of this year suggested that a shortfall is likely to have spilled-over into 2018-19 and 2019-20. If correct, further reconciliations will be required which will reduce the resources available to the Scottish Government still further.

In time, some of the reconciliations from ‘forecast error’ should be positive as well as negative. But it’s important to not lose sight of the underlying driver of these errors on this occasion – that is the implication from Scotland’s tax base performing less well than the equivalent tax base in the rest of the UK.

Scottish Ministers will be hoping that this performance turns around pretty soon.

Authors

The Fraser of Allander Institute (FAI) is a leading economy research institute based in the Department of Economics at the University of Strathclyde, Glasgow.