As the Scottish Budget for 2017/18 has passed through Parliament, the operation of the Non-Domestic Rates pool has risen to prominence. It has provided the Cabinet Secretary for Finance with flexibility to support local government spending and ease the burden of the revaluation to business rates.

So how does the NDRI pool work and what could be the implications over the medium term in the light of the additional cash taken from it to get the budget passed this year?

Its recent claim to fame…..

The NDRI pool has largely been an unnoticed part of the Scottish Budget process, but it has popped up to play an important role on two occasions in the last couple of months!

The first of these, came at Stage 1 of the Budget Bill’s passage through parliament. Here the Government announced a £220 million increase in spending relative to the plans laid out in the Draft Budget in December.

Of this £220m, £30m was funded by revenue-raising tax policy changes. The majority was from Budget Exchange. However, there was also a transfer of £60m from the NDRI pool.

Sources of the additional £220m announced at Stage 1

| Source | Amount |

| Budget Exchange (i.e. underspends from previous years) | £125m |

| NDRI Pool | £60m |

| Revenue-raising from income tax (cash-terms freeze in Higher Rate threshold) | £29m |

| Reduction in forecast borrowing costs | £6m |

| Total | £220m |

The second intervention came a couple of weeks later in response to the pressure to respond to a concern amongst some in the business community over the effect on NDR bills of revaluations for 2017/18.

This issue had been brewing for a number of months. Business rates are calculated by multiplying the poundage (i.e. the tax rate) by the ‘rateable’ value of a property. This value is determined by independent assessors. Assessing the value of every property in Scotland is costly, so revaluations usually only take place every 5 years or so.

As with all such things, there are winners and losers. The losers tend to make the most noise – and often understandably so given that their current business models can often be substantially changed with little warning.

The Scottish Government listened to these concerns and announced a package of measures to help some of the worst affected. Where did this money come from? It seems, once again, the NDRI pool – or more specifically “addressing the forecast in the NDR pool balance, and the adjusted forecasts can be accommodated within that”.

How the pool works….

As we mentioned in our original blog, the operation of the non-domestic rates pool is complex.

Essentially, each year the Scottish Government makes a forecast for non-domestic rates and guarantees the revenues implied by that forecast (and the block grant) to local authorities as part of the local government settlement. This acts like a withdrawal from the pool.

The government then receives the revenue as the year progresses. This acts as a payment into the pool.

Over time this is expected to balance out. Forecasts should be neither consistently over optimistic or over pessimistic.

The NDRI pool balance…..

So far, all well and good.

But what is interesting is that the recent evidence on the cash balance in the pool suggests that rather than it being in surplus, the pool has actually been in deficit.

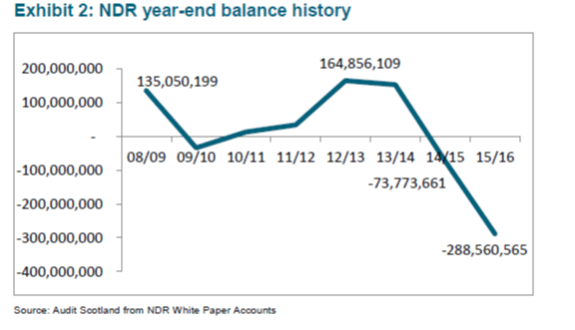

In October, Audit Scotland reported on their audit of NDRI accounts for 2015/16 (the most recent year figures are available) the current position on the NDRI pool.

They highlighted that total non-domestic rates collected during the year were £2,628 million, and total sums distributed were £2,843 million. This led to a deficit of £215 million in that year.

They also highlighted that the cumulative negative balance – i.e. including carry over from earlier years – was a deficit of £289 million which would be carried forward to 2016/17. See chart below:

How can this deficit be reconciled with further releasing of funds from the pool to support these budget measures?

Crucially what matters is not just the pool in one year, but the profile of the pool going forward and – if in deficit – how the government plans to manage it back to balance.

As Mr Mackay outlined in his statement to Parliament on the 21st February, the Scottish Government are “continuing to update the profile of the Scottish Government contribution required to bring the non-domestic rates pool into balance. This process has allowed us to meet the estimated cost of the additional support package announced today.”

Whilst we have no data as yet, one would expect that the balance in 2016/17 must have been relatively healthy which coupled with the profile for 2017/18 onwards will support this return to balance. Of course, the government bears the risk if that this does not happen.

A number of things flow from this.

Firstly, with a deficit of around £289 million in 2015/16, the contributions from the Scottish Government must, with all probability, be quite a significant financial commitment. All things considered, the 2015/16 starting position – coupled with the new £60 million and £45 million support packages – means that any room for manoeuvre is likely to be especially tight in the coming years.

Secondly, with the Fiscal Commission soon to be forecasting business rates income from now on, how these new forecasts will reconcile with the government’s current expectations for future income will have a bearing on the resources at its disposal in the future.

Thirdly, the managing of these balances and the ability to adjust profiles is an important source of flexibility for the Scottish Government. But it also highlights some of the challenges and risks associated with relying upon uncertain tax revenues to support spending commitments – something that will only increase once new tax powers are devolved.

Finally, the entire process is understandably complex. But it is also arguably not very transparent, particularly compared to other parts of the Budget process.

Now that the NDRI pool has come to prominence so explicitly, and similar to the use of underspends to boost the budget this year, opposition policymakers are likely to press the government much more in the future over whether the Draft Budget is indeed the complete picture of resource available. Some may ask whether or not more resources can be found from other sources – such as re-profiling the NDRI pool – to meet additional commitments during any negotiations.

Authors

The Fraser of Allander Institute (FAI) is a leading economy research institute based in the Department of Economics at the University of Strathclyde, Glasgow.