As we flagged in our blog last week, today sees the publication of the latest Government Expenditure and Revenue (GERS) report.

This blog summarises some of the key headline results.

Some background

GERS estimates the contribution of public sector revenue raised in Scotland toward the public sector goods and services provided for the benefit of Scotland. The estimates typically cause significant controversy, and our blog highlighted some of the usual areas of debate.

These arguments are not going to go away, but the GERS figures present the most reasonable approximation to help us understand the nature and extent of public spending and revenue in Scotland in the latest financial year.

What is the headline figure?

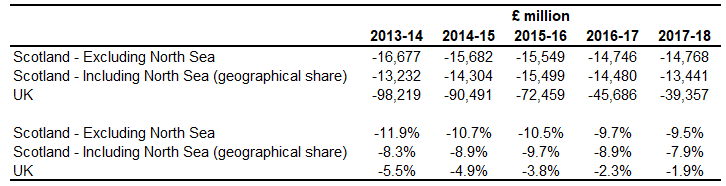

The GERS report shows a net fiscal balance (including a geographical share of North Sea oil) in Scotland of -£13.4bn or -7.9% of Scottish GDP for 2017-18. This compares with a UK balance of -£39.4bn or -1.9% of UK GDP.

This is an improvement on the figures for 2016-17 where Scotland’s fiscal balance was

-8.9%.The main reason for the improvement in the net fiscal balance is a slight recovery in oil revenues – £1.3 billion in 2017-18 compared to £266 million in 2016-17 and the low of £50 million in 2015-16.

Despite this, it is highly unlikely that North Sea revenues will return to levels seen in 2010-11 and 2011-12 in the future, even if the oil price recovers to $100 per barrel, given that the basin is entering its mature stage. The OBR predict that North Sea revenues will remain low for the foreseeable future at around £1 billion.

Table: Net fiscal balance – Scotland and UK 2013-14 to 2017-18

What does this all mean for the Scottish Budget?

Most of the debate today will concentrate on the headline numbers and what this all means for the independence debate.

But from an economic statistics perspective, the more interesting angle is what the figures are telling us about the devolved budget.

In particular, there are a number of interesting revisions in the data published today, which have led to a weakening in Scotland’s fiscal position compared to what was thought to be the case last year – i.e. 2016-17. These include revisions to income tax and VAT due to updated data which is used to estimate the Scottish share of these taxes.

Income tax in 2016-17 was revised down by £451 million due to new Survey of Personal Incomes data.

For the Scottish budget, the relevant figures are non-savings non-dividend (NSND) liabilities which are different to income tax figures presented in Table 1.1 in GERS. Interestingly, the outturn data published by HMRC this summer (see our blog) may suggest that the Survey of Personal income based estimates are over-estimating NSND liabilities in Scotland. However, the data are very new and still being examined, and so have not been incorporated into the headline GERS estimates (see Box 1.1 of GERS).

If this is indeed the case, this suggests that further downward revisions to previous years’ income tax take, and therefore fiscal position, may be coming in future editions of GERS. See Table 4.1 in GERS which illustrates the step-change in the liability figures.

VAT in 2016-17 was revised down by £316 million due to the incorporation of new Living Costs and Food Survey data. This is not an unusual revision for VAT in GERS, and in comparison to a

£13-14 billion fiscal balance figure this is not huge.

However, it highlights the volatility of the series, and as the first year of VAT assignment approaches, it brings into focus the practical issues that could be faced with assigning VAT to the Scottish Budget.

Remember that it is relative growth (compared to the rest of the UK) per person in receipts that matter for the overall impact on the Scottish Budget. There had been expectation from some that if there were revisions to either historical estimates or forecasts, these would generally be in the same direction and therefore have no net effect on the Budget.

However, it can be seen today that for both these taxes, the revisions to the UK are in the opposite direction, which means the effect on the Scottish Budget of the estimates and forecasts of these taxes in future years could be large and hard to predict.

Oil revenues

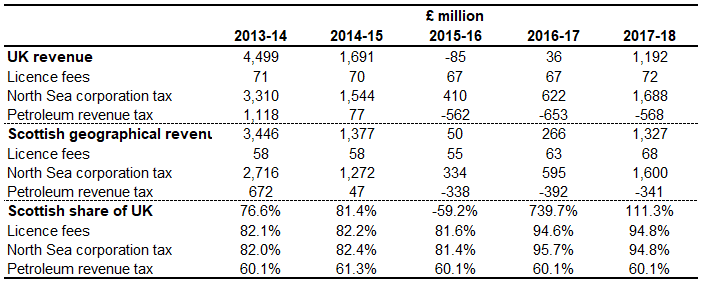

Another interesting point is the treatment of oil revenues in GERS. The method for apportioning these revenues to Scotland hasn’t changed this year, but the improvement in the revenue in this edition of GERS has made the issue more obvious.

You will see from the headline revenue tables (Table 1.1) that Scotland has 1.3 billion or 111% of UK North Sea revenues in 2017-18. This obviously looks a little strange, but the answer can be found in Chapter 2 of GERS.

Table: Geographical share of North Sea revenue – Scotland 2013-14 to 2017-18

Most of North Sea revenue in recent years was made up of two taxes, Petroleum Revenue Tax and North Sea Corporation Tax. Significant changes have been made to the fiscal regime in the March 2015 and 2016 Budgets, which led to a significant cut in Corporation Tax, and PRT being cut to 0%.

So, PRT receipts are now negative and have been since 2015-16. Although companies no longer pay PRT, they can still claim refunds on PRT paid in previous years against current trading losses and decommissioning spending. As a result, PRT receipts will only be negative in the future under the current tax regime.

Because of the fields that are subject to PRT, the Scottish share of this is lower. Therefore a smaller amount is netted off the Scottish figure due to PRT refunds, leading to a larger total than the UK.

Final thoughts

It is important to remember that GERS takes the current constitutional settlement as given. If the very purpose of independence is to take different choices about the type of economy and society that we live in, then a set of accounts based upon the current constitutional settlement and policy priorities will tell us little about the long-term finances of an independent Scotland.

But GERS does provide a pretty accurate picture of where Scotland is in 2018. So in doing so, today’s numbers set the starting point for a discussion about the immediate choices and challenges that need to be addressed by those advocating new fiscal arrangements.

Authors

The Fraser of Allander Institute (FAI) is a leading economy research institute based in the Department of Economics at the University of Strathclyde, Glasgow.