Next week sees the publication of the latest Government Expenditure and Revenue (GERS) report.

As in previous years, the publication will be followed by claim and counter claim about the strength of Scotland’s public finances and economy.

If you are lucky enough to be on holiday – or perhaps choose to hide behind the sofa until the debate passes – in the next couple of blogs, we outline what you can expect to see and hear.

This first blog covers some questions about how the stats are produced. The companion blog talks about the numbers themselves.

What is GERS?

GERS estimates the contribution of public sector revenue raised in Scotland toward the public sector goods and services provided for the benefit of the people of Scotland.

The latest year will cover 2016-17. It therefore takes the existing constitutional settlement as given and the various constraints and protections that this brings.

By receiving the National Statistics kite-mark, this means that the statistics – and how they are presented – have been independently judged to be methodologically sound and produced free of political interference.

How is it compiled?

GERS is produced by independent civil servant statisticians. It is for them to decide on methodology and how GERS is produced.

It is published by the Scottish Government.

All methodologies are public and available for scrutiny.

All changes are peer reviewed by an external group of experts.

A BRIEF ASIDE

Work with us

We regularly work with governments, businesses and the third sector, providing commissioned research and economic advisory services.

Find out more about how you can work with us as an economic consulting firm.

Is GERS based on real data?

On the spending side, the figures are actual data and not estimates.

Taking 2015-16 as an example –

- £40.5bn of spending (around 60% of total spending for Scotland) is from devolved services (i.e. Scottish and local government spending) and incorporated directly.

- For the £17.8bn of UK welfare spending in Scotland in 2015-16, detailed benefits information is used to identify where claimants actually live and how much they receive etc.

- For the remaining £10bn or so of UK Government (non-devolved) spend in Scotland – e.g. defence and debt interest etc. – the ‘UK spend’ data are known, what happens next is simply an apportionment of this to Scotland. Usually this is a per capita figure, so it has no impact on Scotland’s ‘relative’ position.

For revenues, an increasing proportion of the data used is now collected in Scotland. This includes council tax, business rates, the profits made by Scottish Water, landfill tax, land and building transactions tax and local authority user charges and fees.

In the next few years, with the identification of Scottish taxpayers for the first time in 2016-17, income tax will be added to this along with air passenger duty and aggregates levy.

But for other revenues – particularly those collected by HMRC – estimation is needed.

For example, for whisky duty – an excise duty on the consumption of whisky in the UK (not production) – we don’t know how much is actually ‘paid’ by consumers in Scotland and how much is ‘paid’ by consumers elsewhere in the UK. What we do have estimates of however, is how much whisky is consumed in Scotland each year from various surveys. GERS uses this information to apportion whisky duties to Scotland. So if Scottish families are estimated to consume 10% of total UK whisky consumption in a given year, then GERS allocates Scottish revenues 10% of UK whisky duties.

Are the results unreliable because they are based – in part – on estimation?

It’s wrong to dismiss GERS because they rely, in part, on estimation.

Firstly, estimates are not unusual in economic statistics. Scottish GDP figures are based entirely on estimation, as are productivity, trade, unemployment, oil and national accounts statistics.

Secondly, as we will discuss in a follow-up blog, the main factor which drives Scotland’s relative difference with the UK is higher levels of spending – not revenue. Remember the spending figures are based upon actual figures.

Thirdly, the key issue is whether or not the estimates used are robust. The statisticians are transparent about what they use so you can check for yourself.

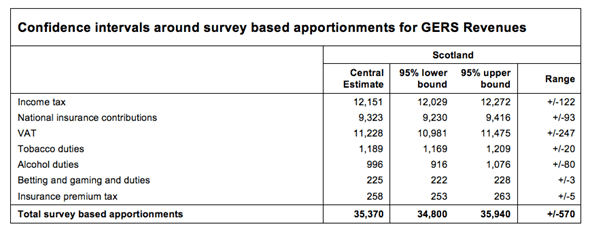

Different methods will give different results but only at the margin.

For example, GERS publishes 95% confidence intervals for many of the ‘big’ taxes that rely on estimation. The key figures for 2015-16 are shown below.

To put this in context, £570m is equivalent to just 0.4% of GDP.

I still don’t believe you – the results will be wrong for sure

Ok, so how ‘wrong’ must they be for the key headline results to change significantly?

We’ll discuss the latest numbers in some detail in the subsequent blog, but for now some back of the envelope calculations provide useful context.

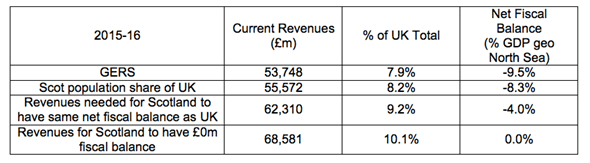

The following table shows the latest GERS revenue estimates and net balance figure for Scotland.

GERS estimates Scotland raising 7.9% of UK revenues – just below a per capita share – in 2015-16.

If Scotland did raise a per capita share of UK revenues (8.2%), Scotland’s estimated net fiscal balance would only fall from -9.5% to -8.3%.

To have the same net fiscal balance of -4.0% as the UK, in 2015-16 Scotland would have had to raise 9.2% of total UK revenues in 2015-16 – around £8.6 billion higher than the latest estimates (to put this in context £8.6 billion is around the sum of Scottish corporation tax revenues, fuel duties, alcohol duties, tobacco duties, inheritance tax, vehicle excise duty and landfill tax put together).

So alternative figures and estimates can be arrived at – and for some individual taxes like corporation tax the estimates are more uncertain – but any changes are small and don’t alter the big picture.

What about expenditure? Again, different assumptions about the elements that are apportioned will have an impact, but again only at the margin.

Take the two biggest examples, defence and debt interest repayments. If Scotland was to be allocated no such spending, the 2015-16 net balance figure would fall to -5.7% of GDP (inc. a geographic share of North Sea revenue).

What about HMRC Regional Trade Statistics – will they have an impact?

In recent days, there has been a debate about the significance of HMRC’s Regional Trade Statistics and their treatment of oil production in Scottish goods exports.

Export statistics are worthy of a follow-up blog later.

But for the purposes of GERS, it’s important to know that the HMRC methodology will have no impact on the results published next week.

Firstly, they refer to exports not profits or taxes.

Secondly, the Scottish Government has already – for years – incorporated oil figures into their economic data (including GERS). Indeed, GERS first included a detailed treatment of Scottish oil revenues back in 2007.

Later on we will ask what next week’s GERS will probably say about Scotland’s spending and revenues, and what the figures might mean for debates around constitutional reform.

Authors

The Fraser of Allander Institute (FAI) is a leading economy research institute based in the Department of Economics at the University of Strathclyde, Glasgow.