Frantisek Brocek and David Eiser

Should local authorities’ revenue sources include a locally set income tax? Or, alternatively, a proportion of the income tax revenues that are raised from its own residents?

This question has been pondered repeatedly – although with varying degrees of seriousness – over the past 15 years or so.

It stems from a view that local authorities’ financial and democratic accountability, and autonomy, would be improved if councils raised a greater proportion of revenues from own sources (rather than grant from central government), and that a local income tax would provide a fairer (i.e. proportionate ability to pay) way of achieving this than trying to extend council tax in some way.

But how much revenue would local authorities raise – collectively and individually – if a given element of the income tax schedule were devolved or ‘given over’ to them?

The answer to this depends on the way that taxpayer incomes are distributed across different local authorities.

Researchers at the Institute for Fiscal Studies (IFS) have developed a model which estimates the distribution of taxpayer incomes across individual local authorities, based on published data on the distribution of employee pay, and HMRC data on taxpayer numbers and average incomes. The IFS has previously applied this model to local authorities in England, and we are grateful to them for allowing us access to the model in order to examine the issue in Scotland.

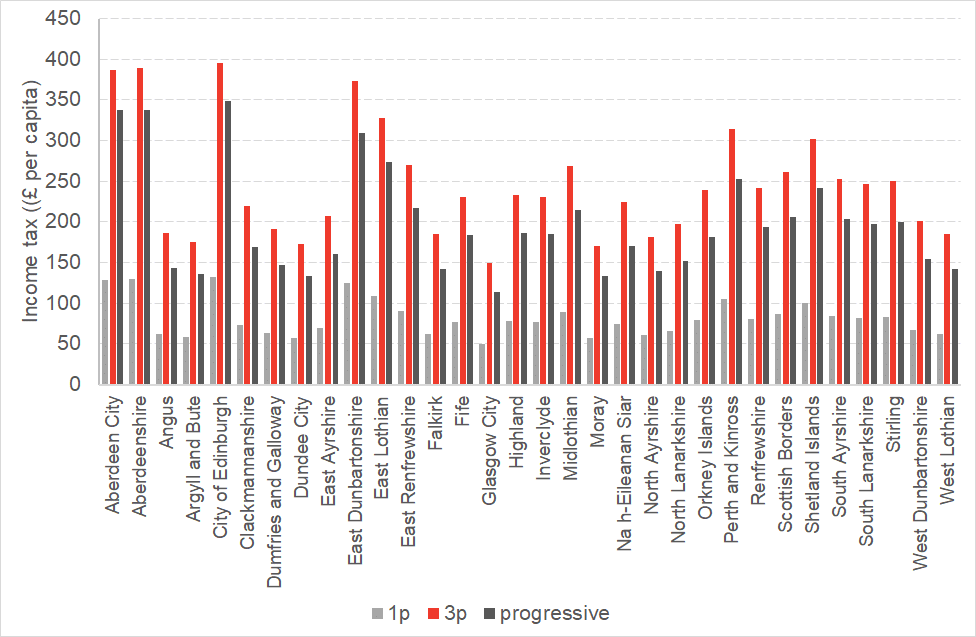

Chart 1 below shows our estimates of the per capita income tax revenues that would have been raised in each Scottish local authority in 2016/17 under three specific local income tax regimes:

- Scenario A: where local authorities retain the revenues raised from a flat 1p rate of tax on each tax band (this need not be thought of as an increase in the overall tax rate faced by Scottish taxpayers, but as a scenario where 1p of the existing tax schedule is effectively ‘given over’ to councils; the policy would raise around £450m for local authorities in total);

- Scenario B: where local authorities retain the revenues raised from a tax rate of 3p at each band of income (raising around £1.35bn in total);

- Scenario C: a more progressive local tax, where local authorities retain revenues raised from each band of income tax raised in their area (2p at the basic rate, 4p at the higher rate, and 4.5p at the additional rate; raising around £1.1bn in total).

Chart 1: Per capita revenue raised by local authorities from three income tax policies

Source: FAI calculations using data from ASHE, HMRC SPI, and ONS

Unsurprisingly there is significant variation across local authorities in terms of the revenues raised per capita. A 3p flat income tax rate would raise almost £400 per capita in Edinburgh, over twice as much as would be raised per capita in Glasgow.

The scale of this differential is surprising, but it reflects lower employment and lower earnings, particularly in the upper part of the earnings distribution, in Glasgow compared to Edinburgh. Remember that what is important in terms of local authority income tax revenues are the incomes of those resident in the area, not of those who work in the area but commute in from outside.

The differential increases further under the progressive policy (as the difference in incomes at the top of the distribution is more marked than the distribution in the middle and lower parts of the distribution).

Is this variation a barrier to having a local income tax? Of course, council tax revenues are unequally distributed too. But they are much less unequally distributed. The Coefficient of Variation of council tax revenues per capita is 0.12, whereas it is 0.27 for the 3p flat income tax policy.

(Of course, you could argue quite legitimately that council tax revenues per capita are subject to less variation simply because there has been no revaluation since 1991 – which is likely to diminish differences between local authorities – and that the council tax is far less progressive with respect to property value than an income tax is – even a flat income tax – with respect to income!)

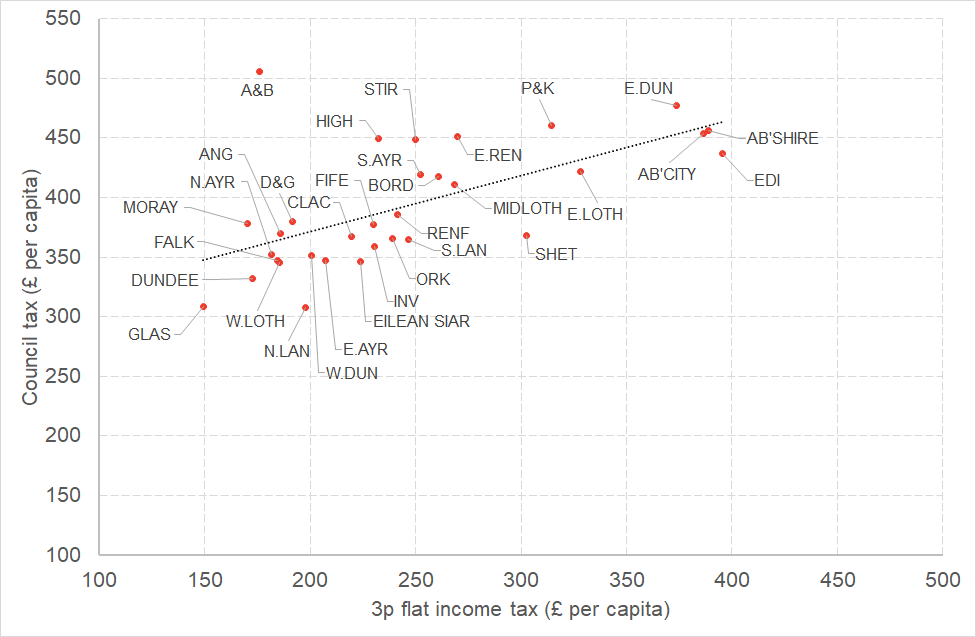

One factor that might strengthen the case for establishing a local income tax would be if income tax revenues per capita were distributed across local authorities very differently from the way that council tax revenues per capita are. If the distribution was different it might lessen the need for equalisation between local authorities in aggregate.

Chart 2 shows that, whilst there is quite a bit of variation around the relationship, there is nonetheless a reasonably strong correlation between council tax revenues per capita and income tax revenues per capita for many councils – although there are notable outliers in both directions.

Chart 2: Correlation between council tax and income tax revenues per capita

Source: FAI calculations using data from ASHE, HMRC SPI, ONS, and POBE

Would devolving or assigning a share of Scottish income tax revenues to local authorities make sense?

The Commission on Local Tax Reform (2015) argued that it might – by broadening local authorities’ tax bases, making them more reliant on a fair tax – although it did also highlight the significant administrative complexities that would be involved.

In contrast the Burt Review (2006) argued that there were ‘objections both in principle and in practice’ to a local income tax, although a number of the Commission’s recommendations seem to stem from an assumption that a local income tax would be additional to the existing income tax schedule.

Arguments for and against a local income tax will no doubt continue to emerge in the coming years, as they have done over the past decades. But whether these debates will ultimately help make the case for – or merely represent a distraction from – the more pressing case for reforming domestic property taxation remains unclear.

Authors

The Fraser of Allander Institute (FAI) is a leading economy research institute based in the Department of Economics at the University of Strathclyde, Glasgow.