Yesterday, the Chancellor of the Exchequer announced changes to income tax in the UK Budget, setting a new higher rate threshold (HRT) of £50,000 for taxpayers in the rest of the UK and a personal allowance of £12,500 for all taxpayers.

What does this mean for taxpayers in Scotland?

The real terms increase to the personal allowance will apply in Scotland. Compared to a scenario where the personal allowance had increased in line with inflation, the policy provides a tax cut of around £70 per year for most of Scotland’s 2.5 million income taxpayers in 2019/20.

The increase in the higher rate threshold – the threshold above which the higher 40% tax rate is charged – represents a tax cut to higher rate taxpayers in rUK*.

But the increase in the HRT will not apply in Scotland. Instead, it will be up to the Scottish Government to decide how to respond in its December budget.

In deciding where to set the HRT in Scotland, the Scottish Government will have to balance competing financial and political considerations.

As a minority government, the Scottish Government has to secure the support of another political party to get the budget bill through parliament. In each of the last two years, this support has come from the Scottish Greens. The Greens’ quid pro quo for supporting the budget has been a cash freeze in the HRT in Scotland in 2017/18, and a 1% increase in 2018/19 – in each case ensuring that the HRT is set below the level originally proposed by the Scottish Government. As a result, the HRT in Scotland in 2018/19 is some £3,000 below the equivalent threshold in rUK.

These lower than inflationary increases in the HRT have benefited the Scottish budget. The Scottish budget in 2018/19 is better off by over £300m as a result of setting the HRT at £43,430 relative to the £46,350 HRT in rUK.

But the gap between the HRT in Scotland and rUK opens up the Scottish Government to the charge that Scotland’s 300,000 higher rate taxpayers face a higher tax bill than their counterparts in rUK.

So how might these considerations influence the Scottish Government’s tax decisions in 2019/20?

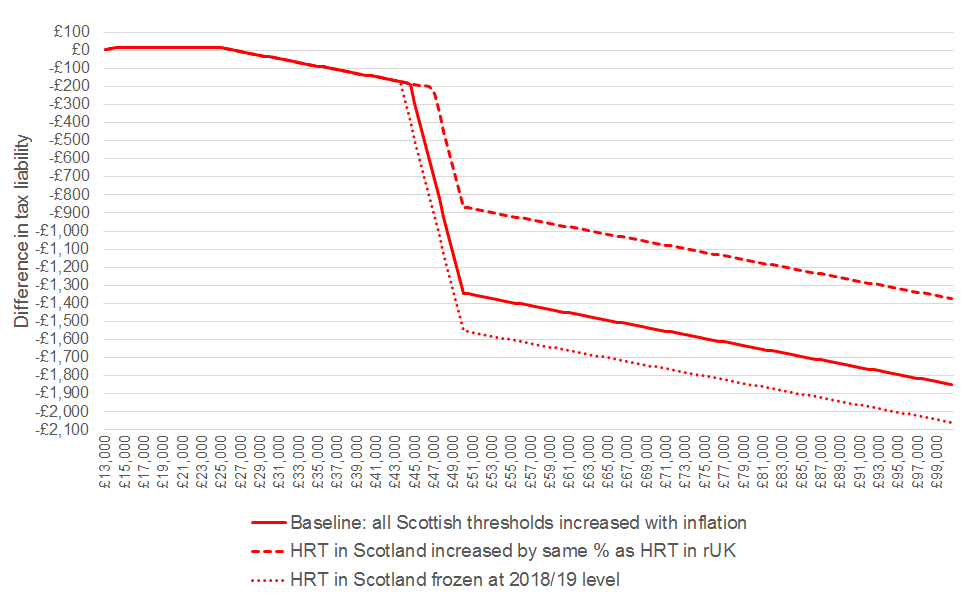

Chart 1. Difference in tax liability between rUK and Scotland taxpayers in 2019/20 under three potential Scottish policy scenarios

The Scottish Government might propose initially to increase the threshold for each rate of tax in Scotland in line with inflation. This would result in the set of tax thresholds shown in Table 1. We call this the ‘baseline’ Scottish Government policy.

The effect of this uprating policy would be that the gap between the Scottish and rUK HRT would increase further. This would generate extra revenue for the Scottish budget. But it would further increase the tax liabilities of Scottish higher rate taxpayers compared to their rUK counterparts (see Chart). A Scottish taxpayer earning £45,000 would pay an additional £290 in tax, whilst a Scottish taxpayer earning £50,000 would pay over £1,300 more in tax compared with an rUK counterpart.

Table 1. Income tax thresholds 2018-19 / 2019-20

If it was sensitive to criticism about the additional liabilities of higher rate taxpayers, the Scottish Government could decide to increase the Scottish HRT by more than inflation. It could for example decide to increase the Scottish HRT by an equivalent proportionate amount as the HRT has increased in rUK.

This policy would take the HRT to £46,850. For a Scottish taxpayer earning £50,000, the difference in liabilities between Scotland and rUK would fall substantially (but still be almost £900).

However, it remains to be seen whether the Scottish Greens would support a budget that proposed a tax cut to higher rate taxpayers – regardless of what had happened in rUK. Indeed it is not impossible that the Greens might argue for a further cash freeze in the HRT. If so, the difference in tax liabilities between Scottish and rUK taxpayers would increase further still.

At our budget event next week we will consider the distributional and revenue implications of these tax policy options in further detail.

*(An rUK taxpayer earning £50,000 will see their total tax liability fall by £250, made up of a £500 fall in income tax liability and a £250 increase in National Insurance liability).

Authors

The Fraser of Allander Institute (FAI) is a leading economy research institute based in the Department of Economics at the University of Strathclyde, Glasgow.