Grant Allan, Peter McGregor and Andrew Ross

Fraser of Allander Institute, Department of Economics, University of Strathclyde

Policymakers have been understandably active in identifying economic opportunities for the UK through new and expanded trading opportunities. The recent Industrial Strategy and Export Strategy lay out the UK Government’s ambitions for increasing exports, as well as seeking out specific sectors where the UK has comparative economic advantage. The Export Strategy talks of an aspiration to raise exports to the equivalent of 35% of Gross Domestic Product.

A successful export strategy, one which does lead to increases in the scale of exports, will bring economic benefits – this is unambiguous. What is unclear however is how such outcomes might interact with government objectives in other areas, such as the Clean Growth Strategy (2018), with its focus on moving to “cleaner economic growth”, though, for example the development of new technologies.

With colleagues we have explored this trade-off at the economy-wide level for the UK. Through our work, supported by the UK Energy Research Centre, we have focused on simulating a successful policy which raises the level of all exports. Our results from this – reported last month – found that, overall, an across-the-board export stimulus raises economic activity while simultaneously increasing energy use and emissions.

In our results, increases in energy use and emissions are greater than the economic boost (in percentage terms), so that energy- and emissions-intensity of GDP rises as a result. Employment increases in all sectors, but again by less than sectors’ energy use. This important finding also confirms that, absent any offsetting policy, there exist tradeoffs between a successful export strategy’s impact on economic activity, with effects on environmental and energy indicators.

These results also suggest the importance both of quantitative modelling of economy-energy links, and also the scale of political judgement in determining the appropriate balance between objectives for energy policy.

But what if there is an opportunity to exploit differences in the impacts of sectoral-specific strategies, which our across-the-board simulation does not capture? Since our modelling framework captures individual sectors (and the links between these e.g. through intermediate purchases and sales) a disaggregated analysis is possible.

Can we, for instance, identify industries where increasing exports have positive economic consequences but without simultaneously increasing energy- or emissions-intensity?

Are there characteristics of sectors which we can use to predict whether export policy might be expected to produce more positive economic consequences without as negative changes in non-economic indicators?

These questions matter as there is likely to be considerable differences in the success of raising exports from UK industries and in their impacts. The Export Strategy identifies opportunities for UK firms to get involved in the global market in low carbon goods and services, with an estimated value of between £1.0 and £1.8 trillion by 2030.

Indeed, as the Export Strategy identifies, specific opportunities exist – for instance – for UK companies to provide exports to infrastructure projects across the globe. The “Belt and Road Initiative” for instance, is identified as an area where there are “opportunities for UK exporters, particularly in terms of: project design, implementation and governance, financial design and legal services; equipment, clean energy and other innovative technologies, and; construction and related services”.

Similar work by Carvalho and Fankhauser (2017) identifies areas of low carbon activity globally where UK firms may have comparative advantage. Their study identifies that opportunities, “extend beyond technologies specifically identified as low-carbon”, and: “The low-carbon economy will encompass all sectors: consultants, lawyers and engineers will offer expertise to drive it; banks will finance low-carbon projects; architects will design low-carbon buildings.”

We therefore have run illustrative simulations focusing on four quite different economic sectors:

- Electrical Manufacturing

- Manufacture of Motor Vehicles

- Communication

- Services

Crucially, when we introduce successful export policies in each sector (note we do this individually, introducing the export shock for each sector in turn) there is the potential for quite heterogeneous impacts across economic, energy and emissions indicators.

A £10billion increase in sectoral exports introduced to each sector in turn leads to much larger economic expansion (in both GDP and employment) for the third and fourth (both “Services”) sectors above, compared to the first two (“Manufacturing”) sectors.

This is partly explained by the existence of economic linkages between the stimulated sector and the rest of the economy in each case, and the energy requirements of sectors providing inputs to these sectors (and so on), e.g. the sector’s own energy-intensity, and the energy intensity of its supply chain.

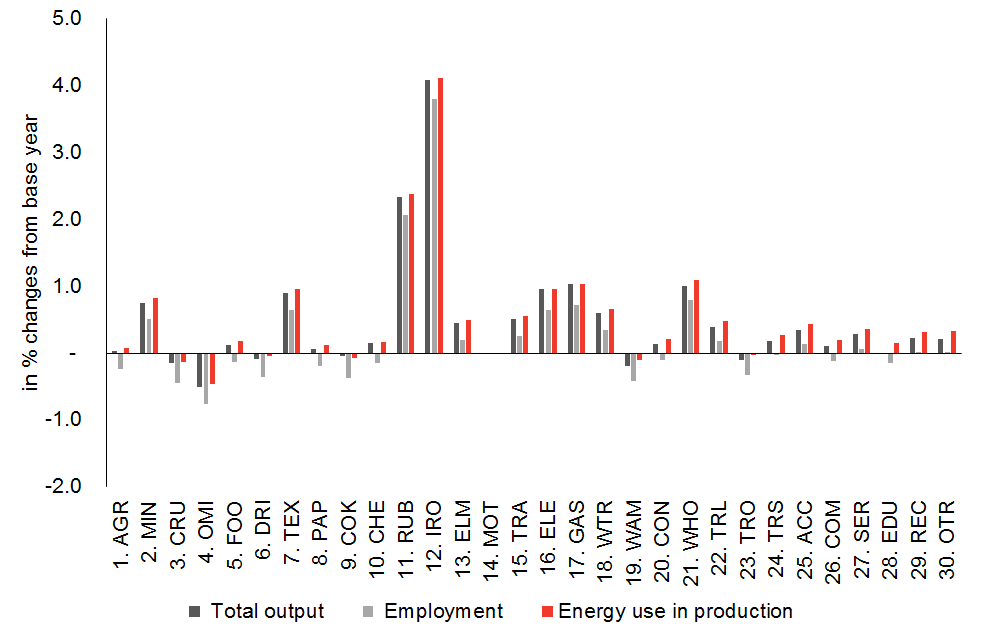

Export-led expansions in the manufacture of motor vehicles, for instance, lead to increases (in economic activity as well as energy use) not only in that sector but in “Iron, Steel and Metal”, “Rubber, Cement and Glass”, for instance, which are also energy-intensive sectors.

Figure 1: Long-run impact on output, employment and energy use by individual sectors of a £10bn increase in internal exports in the Manufacture of Motor Vehicles sector, % changes from base year

Note: results for the Manufacture of Motor Vehicles sector are omitted to make more clear the sectoral interdependencies

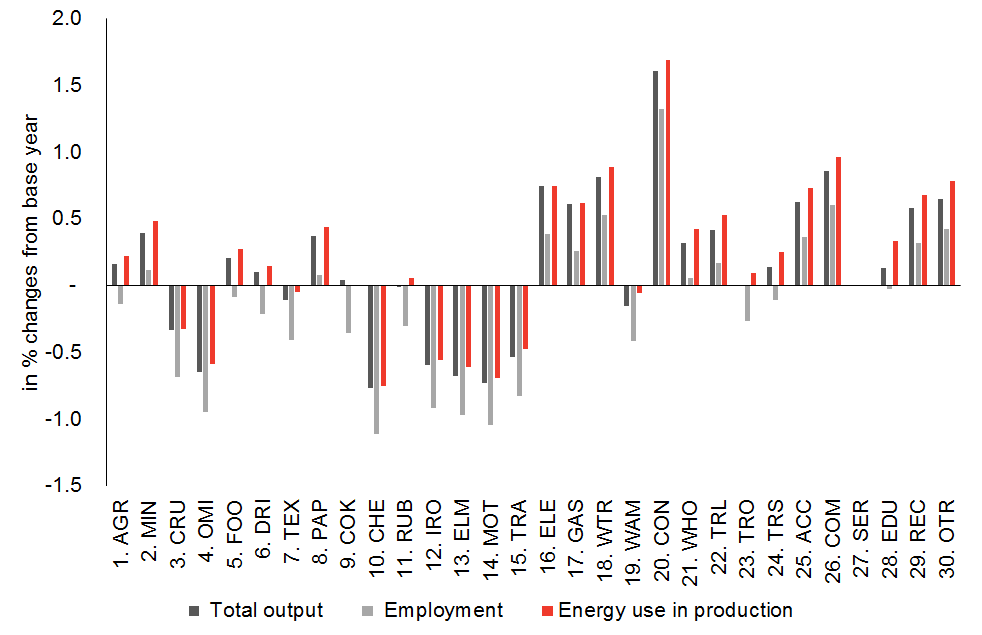

On the other hand, the same scale of increase in exports by the “Services” sector leads to larger positive impacts on GDP and employment, and knock-on consequences across other services sectors, as well as the “Construction” sector, which is itself a key sector in the UK’s Industrial Strategy. We observe reductions in economic activity in some manufacturing activities, particularly those with strong energy demands, which leads to a lower increase in energy consumption at the same time as a larger economic boost.

Figure 2: Long-run impact on output, employment and energy use by individual sectors of a £10bn increase in internal exports in the Services sector, % changes from base year

Note: results for the Services sector are omitted to make more clear the sectoral interdependencies

While these are early and illustrative results, they provide some interesting conclusions.

First, an across the board stimulus to growth through exports – in the absence of mitigating steps – is not typically “green” in nature, stimulating both energy and emissions, as well as increasing both energy- and emissions-intensity of UK economic activity.

Second, it may be possible to target export policies which would stimulate “greener” growth, through addressing sectors with – among other things – lower energy and emissions per unit of output, or smaller links to energy-using sectors.

Third, economic policy which does not acknowledge such “spillover” effects on energy and emissions risks negative impacts on energy policy goals. A knowledge of the likely scale of such spillover effects could be used to develop a more holistic, coordinated approach to policy formation and implementation. For example, pursuit of the Clean Growth strategy could mitigate/offset increases in emissions that would otherwise result from an export promotion policy. This would minimise the prospect of conflicts between UK industrial and green growth strategies.

This research was undertaken by the Fraser of Allander Institute & the Centre for Energy Policy at the University of Strathclyde as part of the research programme of the UK Energy Research Centre (UKERC), supported by the UK Research Councils under EPSRC award EP/L024756/1.

UKERC carries out world-class, interdisciplinary research into sustainable future energy systems. It is a focal point of UK energy research and a gateway between the UK and the international energy research communities. Our whole systems research informs UK policy development and research strategy. UKERC is funded by The Research Councils UK Energy Programme.

For information please visit: www.ukerc.ac.uk

Follow UKERC on Twitter @UKERCHQ

Authors

The Fraser of Allander Institute (FAI) is a leading economy research institute based in the Department of Economics at the University of Strathclyde, Glasgow.