On Tuesday 26 September, we published our report on Scotland’s Budget 2017. Many thanks to those who attended our seminar.

For those unable to come along, or who do not have time to read the full report, here we summarise some conclusions from the sections that looked at the outlook for public spending over the next few years.

A follow-up blog in the coming days will discuss our analysis of longer-term trends.

1. With Scotland’s new fiscal powers, the size of the Scottish budget that Mr Mackay will have to share across the public sector on the 14th December will depend upon 3 things –

- the block grant from Westminster;

- the Scottish Government’s tax policy decisions; and,

- how the Scottish Fiscal Commission’s forecasts for devolved tax revenues compare to the equivalent taxes in the rest of the UK.

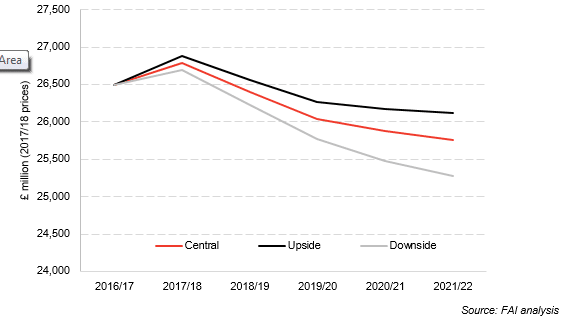

With a relatively fragile economic outlook and the UK Government’s plans to continue to tackle the fiscal deficit, the balance of probability points towards further real terms reductions in day-to-day (or resource) discretionary spending over the remainder of the parliament (and possibly beyond).

Illustrative scenarios for the real-terms outlook for the Scottish resource budget (£ million): 2017/18 prices

The exact year-on-year profile is – of course – uncertain (and will depend upon the extent to which the Scottish Government proposes to raise revenues themselves), but the outlook for public spending is clearly going to remain challenging for the foreseeable future.

2. Given Scotland’s relative economic performance vis-à-vis the UK, there is the possibility that the Scottish Government could trigger the emergency borrowing powers embedded within the Fiscal Framework. This would increase the budget by up to £600 million but this would of course have to be repaid at a future date.

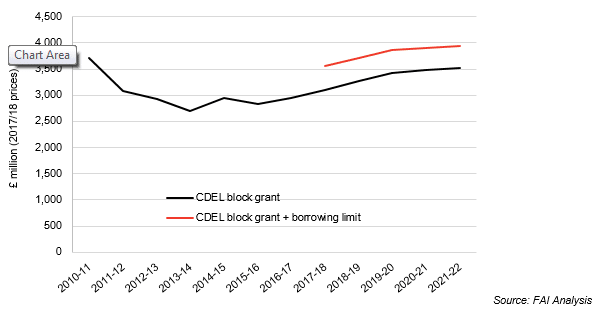

3. The outlook for capital spending is more positive – driven by the decision the Chancellor took at last year’s Autumn Statement to boost capital spending across the UK.

If the Scottish government makes full use of its borrowing powers, then by 2021 capital spending in Scotland will have moved above its 2010/11 peak (and be worth nearly £4 billion).

Real terms outlook for the Scottish capital budget (£ million): 2017/18 prices

4. Within this overall envelope, the Scottish Government has set out a number of policy priorities for the next few years, including

- a commitment to increase health resource spending by £500 million more than inflation by the end of this parliament;

- to maintain real terms spending on policing;

- to double free childcare provision; and

- to invest an additional £750 million in a school attainment fund over the course of the parliament.

These commitments – just on their own – mean that over half the Scottish budget can be viewed as ‘protected’ (around £15 billion).

5. In a time of fiscal restraint, delivering on such commitments necessarily requires the burden of any squeeze to be borne by other public services. As an illustration, delivering on just the four budgetary priorities above could mean that ‘non-protected’ areas face real terms cuts of between 9% to 14% over the parliamentary term (2016/17 to 2020/21).

Real terms budget implications for non-protected portfolios under a variety of budget scenarios (£ million): 2017/18 prices

6. On top of this can be added other commitments like free higher education tuition, college places, free personal and nursing care and funding for school education.

Lifting the 1% pay gap will also cost money. A 3% increase in pay – in line with inflation – could cost around £350 to £400 million even accounting for the higher tax revenues the government could receive from wage increases increasing income tax receipts. The government are also likely to wish to build up some reserves should tax receipts come in under forecast or if they wish to build some form of resilience buffer in the light of Brexit.

7. Moreover, whilst Scotland’s new social security powers carry significant opportunities to introduce new policies and take advantage of synergies with existing devolved levers (and thereby save money in the long-run), they too bring some risks.

For example, there is potentially a gap of around £100 million over the four years to 2021 in terms of how much the Scottish Government think it might cost to set-up the new devolved social security system and the amount of money transferred from the UK Government to help with this process. The same estimates suggest a gap of over £80 million per annum for the running cost of administering the new system.

8. So the settlement is clearly tight and with big commitments to pay for some difficult decisions are likely to be required this December. Already the government has committed to publishing options around income tax and it seems ever more likely that this year’s budget is going to be as much about taxation as it will be about public spending.

Authors

The Fraser of Allander Institute (FAI) is a leading economy research institute based in the Department of Economics at the University of Strathclyde, Glasgow.