Today’s Spring Statement was expressly not a ‘budget’; it contained no new spending or tax policy announcements. Instead, it was an opportunity for the Chancellor to update parliament on the latest UK economic and fiscal forecasts.

It is only three and a half months since the Autumn Statement in November. The big statements then were about the major downward revisions to the forecasts for UK economic growth.

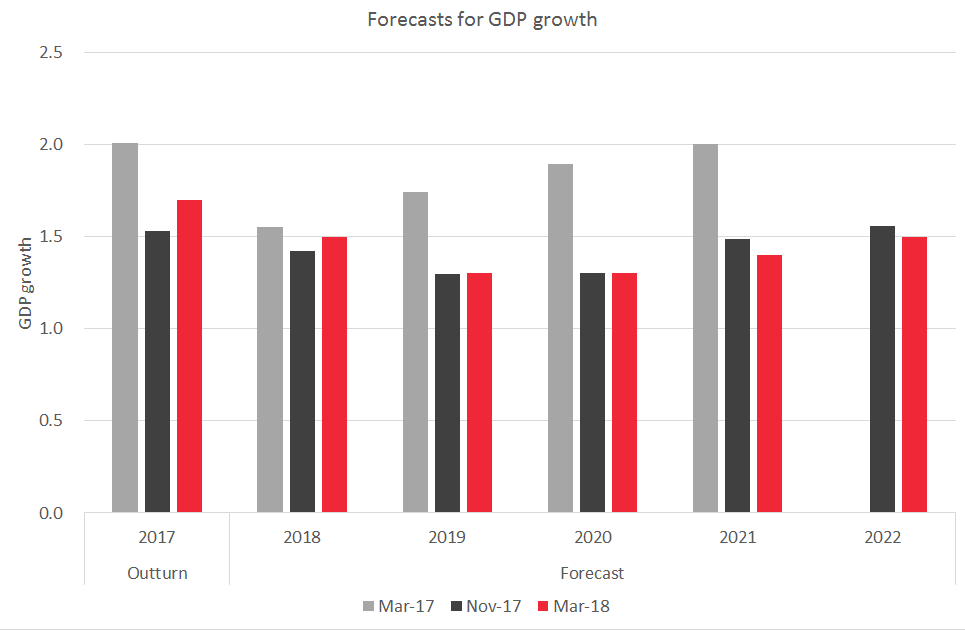

Today there was a smidgeon of relatively better news on the economy. GDP growth in 2017 turned out to be slightly higher than the OBR had expected, and it has also revised up its forecasts for 2018. But these upward revisions in the early years of the forecast are mirrored by slight declines in later years (the OBR has effectively reassessed its view of where we are in the ‘economic cycle’).

Moreover, the upward revisions are nowhere near sufficient to offset the downward adjustments in November (see Chart). UK growth of 1.5% in 2018 is still forecast to lag EU and US growth (forecast at 2.3 and 2.9% respectively by the OECD).

What about the public finances?

Tax receipts have performed slightly better than the OBR was expecting in November, reducing the forecast for the deficit (very slightly) this year. Public sector net borrowing (the deficit) is now forecast to be £45bn, or 2.2% of GDP in 17/18.

But the OBR thinks this improvement in the deficit reflects cyclical factors. The forecast for the underlying ‘structural’ deficit, on which the Chancellor’s target is based, is basically unchanged since November. The structural deficit is forecast to fall below 2% in 2018/19, two years ahead of target (see Chart).

In fact the Chancellor is now able to say that there will be a surplus on current spending in 2018/19. This means that the government’s tax income is sufficient to pay for day-to-day spending on public services. This is the first time that this has happened since 2003.

Normally a deficit of close to 2%, combined with a surplus on current spending, would be taken as a sign of healthy public finances. But the shadow cast over all of this is the public debt. Public sector net debt is forecast to peak in 2017/18 at over 86%, and then to begin to decline slowly.

The Chancellor argues that a debt to GDP ratio of this size represents a risk to the public finances, in that the costs of financing this debt (currently around £41bn per year) could become challenging if interest rates increase or if another shock were to hit the economy.

How real these risks are – and how serious the implications – will continue to be debated. And even if the need to continue to reduce the deficit is accepted, the extent to which further reductions should be balanced across spending cuts as opposed to tax increases will prove another area of contention. The UK Government’s day-to-day spending on public services per capita is forecast to decline in real terms in 2018/19 and 2019/20.

The Chancellor had faced increased calls even from within his own party to use the Spring Statement to announce targeted increases in public spending, financed through some tax increases. He has resisted those calls for now, but hinted that he would use his Budget in Autumn to reconsider spending commitments, whilst the UK Government will have a full Spending Review in 2019.

What does all this mean for Scotland?

Not a great deal in the immediate term. With no policy changes at UK level, the forecast for the Scottish resource block grant remains to decline by 0.8% in 2018/19 and 1.2% in 2019/20. The Scottish Government’s response for 2018/19 has been to use its new income tax powers to offset the immediate cuts to its grant, so that its budget this year will actually increase slightly, based on the Scottish Fiscal Commission’s latest forecasts.

The key question now from a Scottish perspective is the extent to which devolved tax revenues perform on the upside or downside.

In May this year, we expect the Scottish Government to set out its medium term tax and spending plans. And in September, we will have an update from the SFC as to how the Scottish devolved revenues are performing. Fiscal events seem to becoming more frequent, rather than less!

Authors

The Fraser of Allander Institute (FAI) is a leading economy research institute based in the Department of Economics at the University of Strathclyde, Glasgow.