The design and structure of both income tax and council tax have been extensively debated in recent years. But the design of charging structures for water and sewerage services, which represent a lesser but nonetheless significant expense for many households, have received less attention.

The average household bill for combined water and sewerage services in Scotland was £360 in 2017/18. However, there is significant variation in the charge paid by different households. What are the principles on which the water and sewerage charges are based? And is the distribution of charges across households fair?

Water and sewerage charges are determined by the Council Tax Band a household falls within. In 2017/18 a Band D property is charged £431. Households in other bands are charged a ratio of this, with this ratio reflecting the ratios that were used to determine council tax charges (prior to the 2017/18 changes in council tax ratios). So a Band A property is charged £287, whilst a Band H property is charged £861. Single occupancy households receive a 25% discount on bills, whilst some groups receive either discounts or full exemptions (e.g. households occupied by students).

Two key principles underlie this charging structure. First, water and sewerage charges are levied on the basis of full cost recovery – all costs associated with providing water and sewerage services are recovered from customers’ charges. Second, charges are structured to be related to ‘ability to pay’, with better off households facing higher charges.

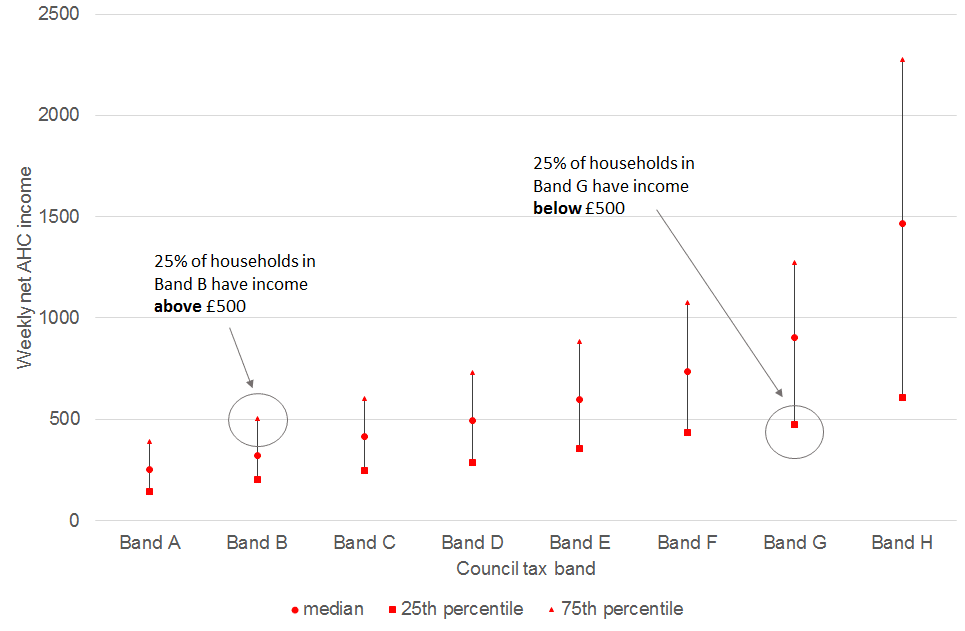

The principle of relating charges to ability to pay sounds reasonable. But by linking charges to council tax band, this principle is only partially achieved in practice. This is because, whilst household incomes increase with council tax band on average, there is much variation around this average relationship. In other words, there are households in Band A with relatively high incomes, and households in Band E and above with relatively low incomes. This observation is shown in Chart 1, which shows that – for example – whilst a quarter of Band B households have disposable income above £500 per week, a quarter of Band G households have income below £500 per week. Yet the annual water and sewerage charge is £718 for the Band G house and £335 for the Band B house.

Chart 1: Relationship between household income and council tax band, 2015/16

The fact that there is so much variation in the relationship between council tax band and household income means that the relationship between household income and its water and sewerage charge is also weak. Within a given council tax band, there are households whose water and sewerage charge is relatively high compared to income, and those for whom the charge is relatively low.

At this point it is important to add that low-income households, who are in receipt of Council Tax Reduction, receive a reduction in their water and sewerage bill. However this reduction is not as extensive as their reduction for council tax. Households receiving CTR can receive a maximum discount of 25% on their water and sewerage bill, with the amount of discount determined by the level of reduction in CTR. For example, a household that receives a 100% reduction on its council tax bill receives a 25% discount on its water and sewerage bill; a household that receives a 50% reduction on its council tax bill receives a 12.5% reduction in its water and sewerage bill; etc.

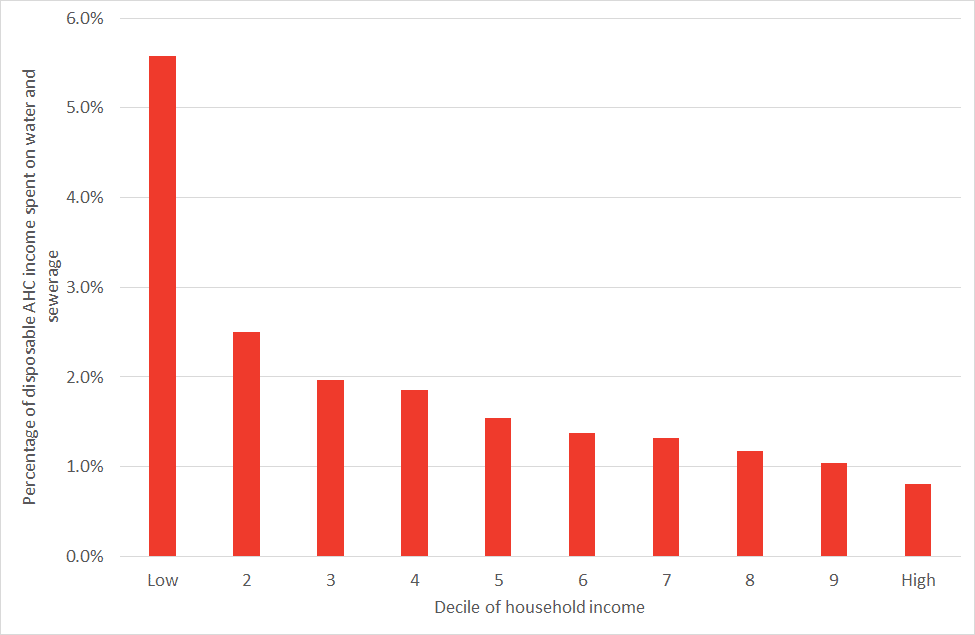

We can put these elements together and consider how water and sewerage charges vary as a percentage of income across the income distribution (Chart 2). Households in the lowest income decile spend more than 5% of their income on water and sewerage, with this percentage falling successively for each subsequent decile of the household income distribution.

Chart 2: Household spending on water and sewerage as a percentage of disposable income

For a system ostensibly based on ‘ability to pay’, the charging structure looks fairly regressive. Needless to say however, the charging structure would look even more regressive if, rather than charges increasing with Council Tax Band, there was a flat charge across bands. On the other hand, the system could be made more progressive if support for those in receipt of CTR was extended.

Is there a better way to distribute charges across households? In reality there are no easy answers. But the starting point for any discussion needs to consider what the principle for charging should be.

Is water and sewerage seen as a public service that those on higher incomes should contribute disproportionately towards? If so, it might be most appropriate to fund water and sewerage through a progressive income tax, combined with a relatively low flat charge.

Is water and sewerage seen as a utility, for which people should pay in proportion to use? If so, there is a case for introducing metering (as is the case in England), combined with enhanced support for those on the lowest incomes.

Basing the charge on property value could be justified if property value is seen as a proxy for water use. However, the relationship between property value and water use is likely to be very weak.

The current charging system is a hybrid system that reflects various aspects of these principles.

- Charges are positively but weakly related to income (partly because the correlation between council tax band and income is weak and partly because the reductions for low-income households are inadequate). And despite charges increasing with income on average, poorer households pay more as a proportion of income than better off households.

- Charges are only peripherally related to water use (in the sense that single people receive a 25% discount, and that there is a positive but weak correlation between council tax band and occupancy).

- Charges are only partially related to property value (although this in theory could be rectified if the government were willing to undertake a revaluation exercise for council tax purposes).

The primary advantage of the current system is its administrative simplicity – charges are easily calculated based on information already held by councils (and councils collect payment on behalf of Scottish Water). But alternatives need not be necessarily more burdensome.

Whilst the rationale for the current charging system is somewhat ambiguous, it also represents a classic political compromise between competing arguments and principles. The outlook for comprehensive change in the near future seems therefore unlikely. But there is a strong case for enhancing the financial support available to the lowest income households.

Authors

The Fraser of Allander Institute (FAI) is a leading economy research institute based in the Department of Economics at the University of Strathclyde, Glasgow.